This year’s Money20/20 agenda = stacked. 💥

Industry leaders from across FTA member companies will take the stage to share their perspectives on innovation, inclusion, and the policies shaping the future of finance.

See you in Vegas next week! 👀

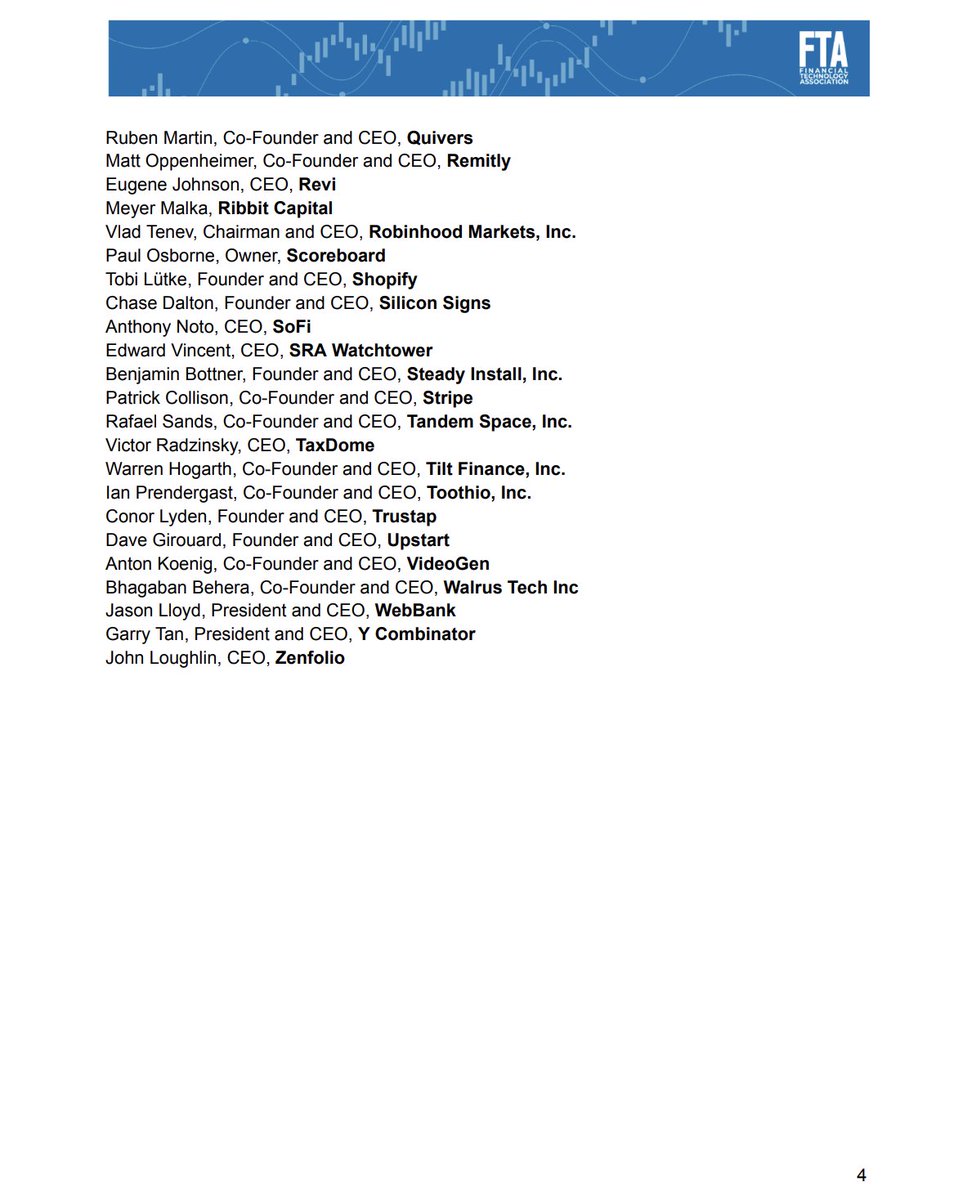

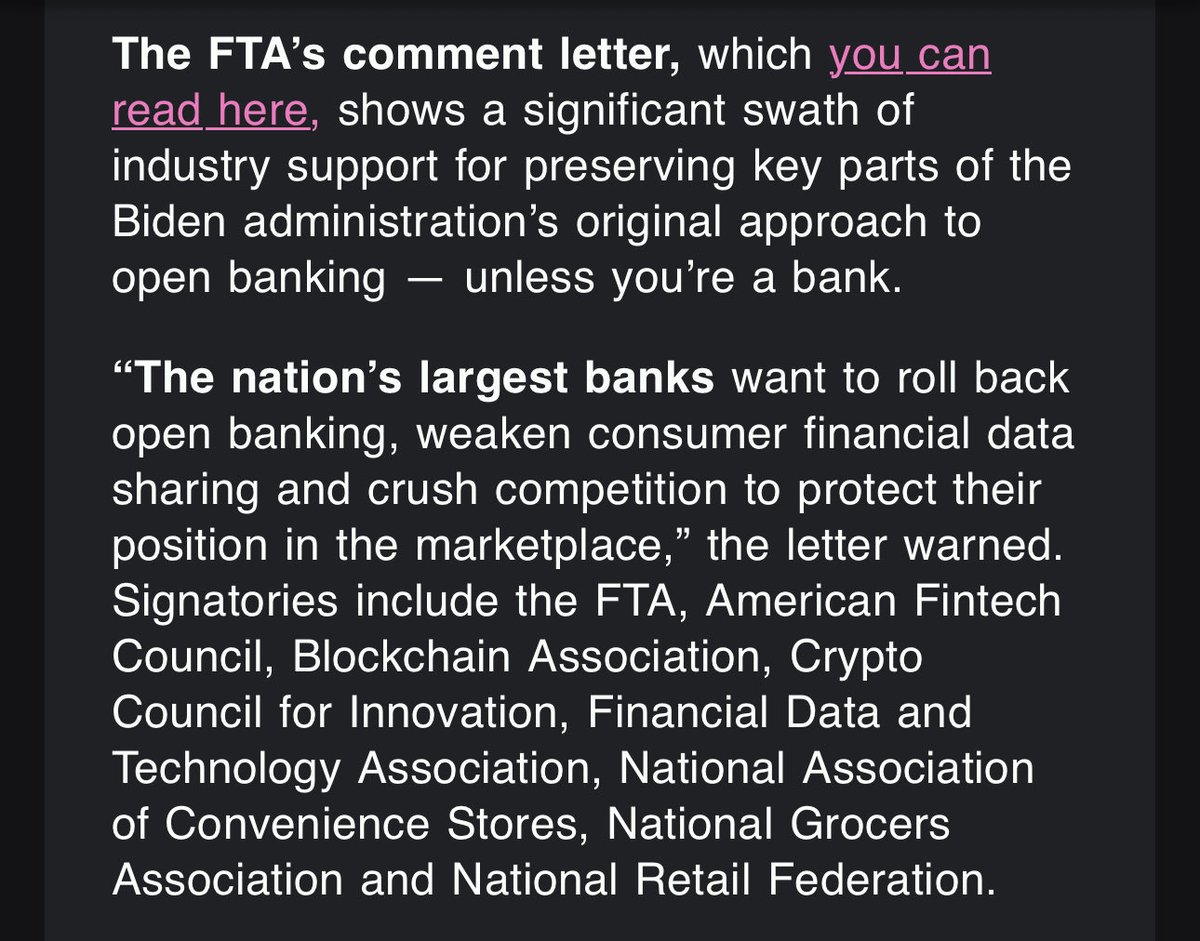

It’s rare that we write a story based off a single trade comment letter. But this coalition really is a who’s who of groups that aren’t banks but care about bank stuff (in a very specific way banks do not like)

Great panel today from @fintechassoc on why the CFPB and Trump administration should protect open banking from falling prey to large bank games and fees.

ICYMI, keep an eye out for their recording. Fantastic insights from @arampell@ciaomack@garrytan and more.

Important for everyone to understand

👇 👇👇

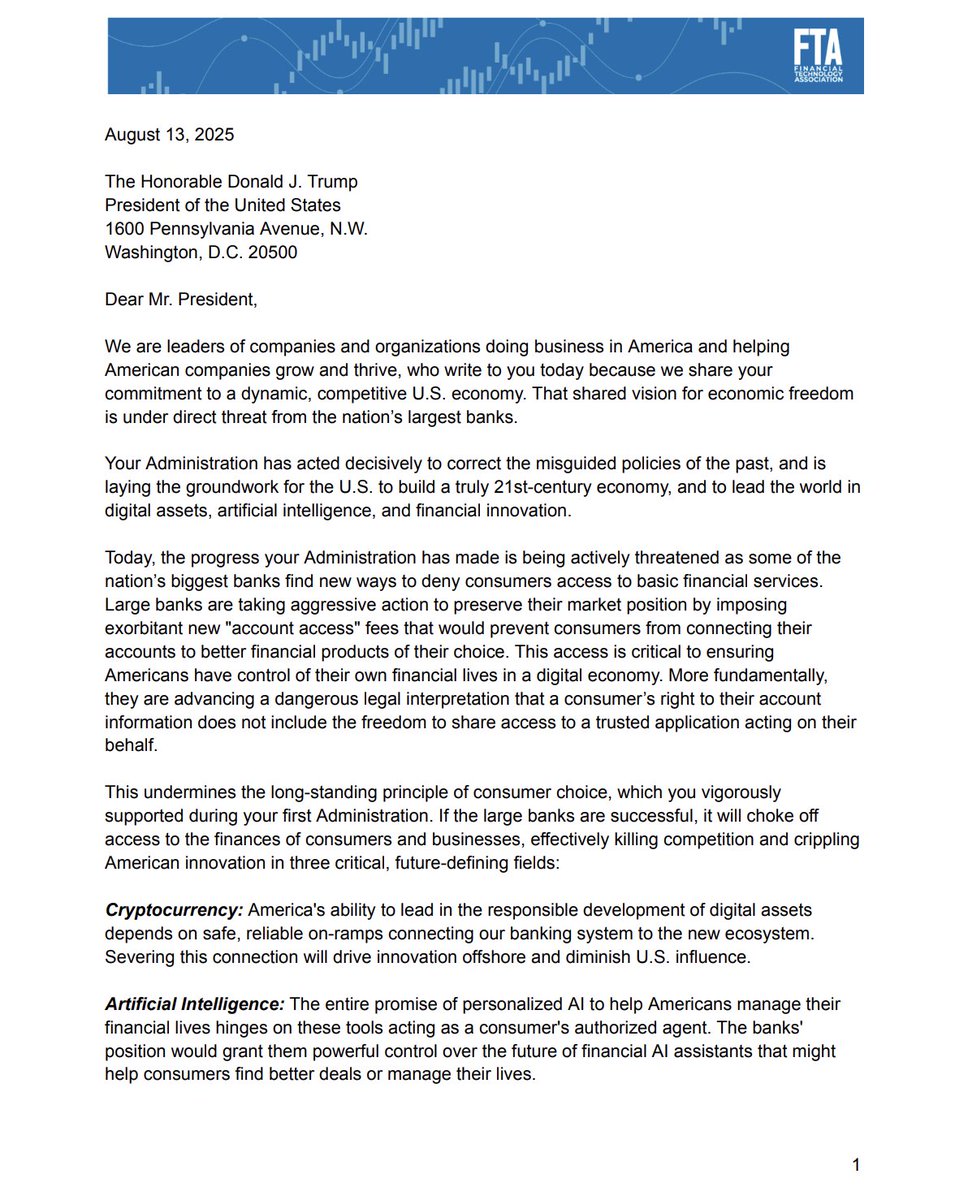

Your money. Your data. Your choice. Big banks want to shut that down. Good thing President Trump has the power to override them by strengthening the 1033 rule. Open banking is a necessity for entrepreneurs to thrive and to keep competition alive and innovation strong.

https://t.co/BUwxFG02HJ

As a consumer, I am really thankful for the CEOs who signed this letter. The Trump Administration has the opportunity to make sure America keeps looking forward on financial technology, instead of letting a handful of oligopolistic banks drag us into the past.

Banks should not be able to trap your funds and data with them and make it difficult for you to access your data or move your capital to wherever you see fit. That is your human right and foundational to the proper functioning of the system of capitalism that our country was founded on. This is the spirit of Open Banking and that's why I have signed this letter urging President Trump to support Open Banking. Onward! 🇺🇸🚀

.@tyler and @cameron signed their names to this letter urging @POTUS to support open banking and oppose anticompetitive fees on consumer data access. Account access and data belong to the customer.

Chase is implementing grabby fees to prevent customers from sharing their own account data with other apps. We (and 80 other companies listed below) think that's bad.

We are proud to sign this letter to help support innovation and competition in consumer finance. Together, we can build a better financial system for all Americans.

Why I Signed the Letter Against Data Access Fees

A few weeks ago I wrote about JPMorgan’s attempt to charge fintechs for customer data access. I said then that once data becomes a revenue stream, the goal is to fragment it, lock it in, and sell it at margin. https://t.co/vKHObuxvyE

That is precisely what is happening.

I signed this Financial Freedom letter because the stakes are higher than people realize. Charging high fees for access to consumer financial data is not just bad policy. It is technically backwards, economically short-sighted, and strategically dangerous. It breaks the infrastructure we are trying to build.

This is not just about fintech. It is about who controls the future of programmable money, open finance, and digital ownership. And whether the next generation of innovation gets built in the United States or somewhere else entirely.

Here is what is really going on.

APIs were supposed to fix this

For the last decade, the industry has pushed for a move away from screen scraping and toward secure, permissioned APIs. That shift has made financial data access more reliable, more privacy preserving, and more technically sound. It created the foundation for almost every product people use today in budgeting, investing, lending, and crypto.

But now some banks are trying to turn those APIs into toll roads. The same infrastructure that was meant to be a public good is being privatized. They are taking what was supposed to be a safety upgrade and turning it into a gate.

This is not about cost recovery. It is about control. They know that if they can make access expensive enough, they can decide who gets to build and who does not.

Monopolies do not announce themselves

They evolve one restriction at a time.

JPMorgan is now charging some fintechs millions of dollars just to access data that their own customers have explicitly authorized them to use. That is not a security improvement. That is a moat.

The pricing is not tied to usage. It is tied to leverage. And if that becomes the norm, the only products that survive will be the ones that can afford to pay for access. That is not a world where the best ideas win. That is a world where the incumbents always do.

The right to access your own financial data should not be for sale

Section 1033 of the Dodd Frank Act is clear. Consumers have the right to access and share their financial data. That right is not supposed to depend on whether a developer can afford to pay a monthly API invoice.

We do not let phone companies charge extra to forward your text messages to another app. We do not let internet providers throttle specific websites based on who pays them the most. We should not let banks decide which tools you are allowed to use with your own financial history.

Data ownership without access is not ownership at all.

This is how you slow a sector without ever passing a single law.

Open finance only works if the rails are actually open

There is a reason telecoms are interoperable. There is a reason email is open protocol. There is a reason you can use a Visa card at any store and plug any USB device into a laptop. These systems thrive because they are permissionless at the interface layer.

That is what APIs are supposed to be. Interfaces. Not bottlenecks.

When access is restricted or priced in a way that favors only the largest players, you kill the optionality that makes ecosystems work. You force developers to route around the problem. And you start breaking things in ways that will not show up until it is too late.

We are already seeing this happen. Some fintechs are considering going back to screen scraping. Others are contemplating passing the cost to consumers. Still others will shut down entirely.

None of this is good.

The United States cannot afford to get this wrong

While this is happening, Europe is expanding its PSD3 framework. The UK is rolling out Open Banking Plus. Brazil, India, and Singapore are building real time interoperable financial rails that treat access as a utility.

The United States is at risk of turning the most dynamic financial technology sector in the world into a walled garden run by a few institutions. That is not how you stay competitive. That is how you fall behind.

If we want to lead in programmable money, real world assets, stablecoins, and self custodial finance, then we need to defend the basic principle that consumer data access should be easy, safe, and free.

We cannot outsource our financial infrastructure to the few players who have the most to lose.

Why this matters now

The platforms that win over the next decade will be the ones that treat access as a feature, not a tax. The builders who succeed will be the ones who can operate without asking permission every time they want to improve the user experience. And the countries that lead will be the ones that make it easy to connect and build without interference.

I signed this letter because we should not let a handful of banks dictate who gets to innovate. We should not tax developers for using better technology. We should not sell consumer data rights back to the people who already own them.

The future of finance should not depend on who can afford to pay for it.

Bits about Money is back with an explanation of Open Banking, which has recently come under legal fire from banking trade associations and one large bank in particular.

https://t.co/8Bjj1loDZ6

1/ Today, we sent a letter from over 80 CEOs across industries urging @POTUS to support open banking and oppose anticompetitive fees on consumer data access set to take effect next month.

#OpenBanking#FinancialFreedom

On this day 75 years ago, Babe Didrikson Zaharias won the Titleholders Championship

This was the first major of the LPGA era and the first of Babe's eight wins in 1950 #LPGA75

MORE ⬇️ https://t.co/VDNoQiAphp

@FrankLuntz Payday loans are high interest loans. Klarna’s BNPL product is zero interest with an option to pay now - no installments. Hardly the same thing