Energy hasn't performed well last year despite bullish sentiments around China reopening, under investment in the sector etc.

Have the fundamentals changed or this just for short term before the next up move begins.

https://t.co/vomUNIKL6L

What is Liquidity? Most often we tend to associate this to M2. But, liquidity is more broader than just this. Michael from CrossBorder capital explains the definition of liquidity, how this movement has led asset market turning points.

https://t.co/mDfH6bT10X

This week's update by Louis from Gavekal is an interesting one, as it talks deeply about reasons why one needs to stay humble in these markets.

https://t.co/CCUmt8gl6I

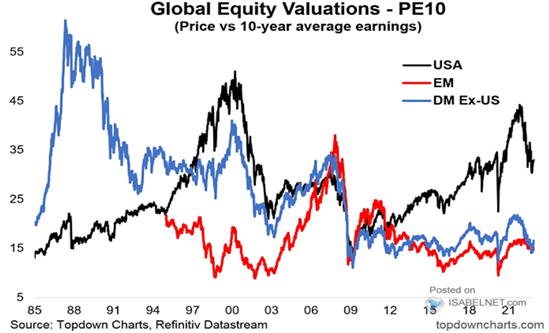

China is reopening, $ is rolling over & the Fed is pretty much done tightening. EMs are hugely under owned asset class & may see a long journey upwards from here.

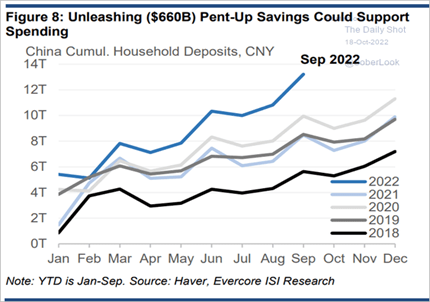

China 2nd biggest economy is re-opening after being on lockdown for 3 years. Over past 3 years, China’s household savings has increased by 50% to 15.5 trn. Excess savings along with record low mortgage rates will main drivers of pent up consumption demand driven inflation in 2023

One way to play this theme is to own assets in countries beneficiary of Chinese demand boom like EMs & Japan. Brazil, India, Mexico etc. were outperforming in 2022 when they were facing macro headwinds, now these headwinds are turning into tailwinds.

While we could have seen peak hawkishness; but, we haven’t yet seen peak inflation & China’s reopening could further push peak inflation. If we draw reference from 70s, inflation rises due to base effects leading to wages spurt; which then slows down until you get another spurt

But, as covid hits China you could see shortage of workers in next few months. So next quarter is going to be all about increase in demand on one hand & production dislocations on other. We have seen this playbook in West when they begin re-opening.

Would a Japanese insurer buy a UST yielding -1% after hedging for FX risk when 10y JGB’s yield 0.25%?

What happens when foreign investors start dumping their UST holdings in an illiquid bond market?

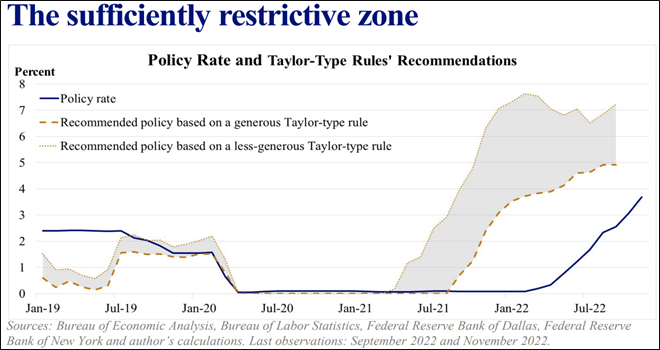

Still thinking of 7% policy rate?

Fed St. Louis, President James Bullard, released an update which says ���Even under most generous assumptions, policy rate is not yet in a zone that may be considered sufficiently restrictive”. He mentioned that hikes so far have had a limited impact on inflation.

Will Fed be able to move swiftly on the upside?

Forex hedged 10y UST yields are the most NEGATIVE they have been in over a decade, with FX hedged UST yields for Japanese investors at -1% & for EU investors at -1.44%, despite 10y UST yields at the HIGHEST levels in over a decade.

As discussed in our past updates, with US Debt/GDP at ~130% and Fiscal deficit ~10%; US faces a huge dilemma as at 4.5% rate interest costs could be ~29% of total federal tax receipt.

Markets were quick to interpret this as indication of a more hawkish stance going ahead with 3 mo /10 year treasury yield curve inversion falling back to 2019 lows.

He was referring to the ‘Taylor rule’ which is widely accepted in monetary policy discussions in past 30 years. As per this, the range for policy rate laid out is between 5–7% in generous to less generous scenario. Presently, we are at 3.75-4% on the policy rate.

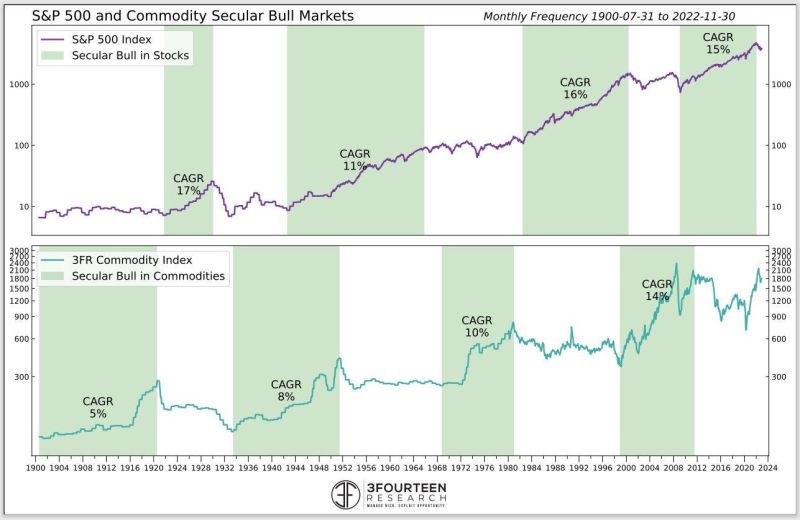

If we are in early trends of entering into commodity bull market then odds of global recession could be very high.

Equities enter bear markets during commodity bulls & there’s a high probability that markets will be flat for 10 years like 1966-1982(Source: Warranpies)

There's going to be globally a increase in inflation when China reopens. Doesn't that pretty much eliminate the possibility of the Fed pivoting? Would Fed pivot into increasing inflation and risking almost a hyperinflationary runaway situation.

XI vs Powell pivot

US CAD could not be any bigger than it is right now, US consumer is pushing $100 bn/month to ROW; 50 - 60 of which goes to China. But, world's second largest economy & exporter is on a lockdown; which, means this surplus that China's makes stuck in system

Along with Inventory built up, the 2022 deposit surge in China should support consumption next year, which thus far has lagged amidst lockdown uncertainty. Rising Chinese consumption could increase foreign tourism, demand for goods which further could aid inflation.

Maybe this is the reason that China isn't reopening. Leadership is worried about inflation & first wants to make sure that they've built necessary inventory. So until China has restocked off on coal imported from Indonesia & oil from Russia, reopening doesn’t seem to be on cards

China probably right now is under consuming by about a million and a half barrels per day. So if they come back in and consume an additional million and a half barrels, you have to wonder where that is going to come from?