🚨 HEAR ME OUT NOW!!!!

A Major Financial Shock Is Lining Up for 2026 and the Warning Signs Are Already Here.

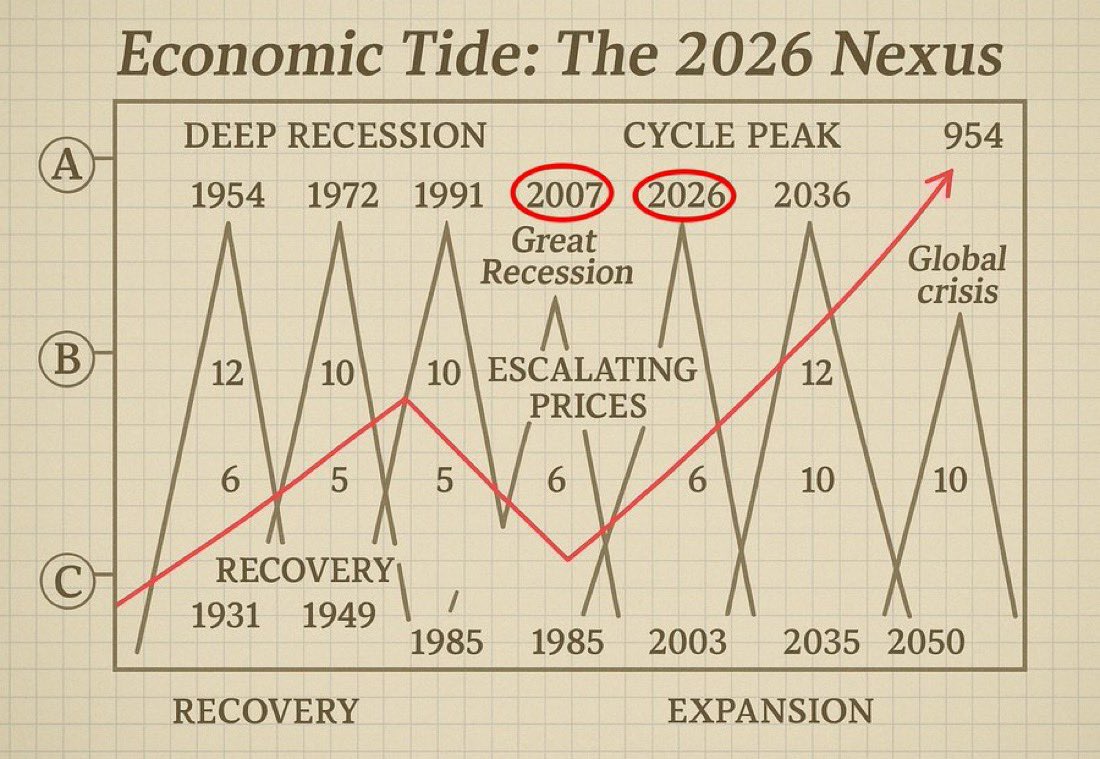

Something big is coming for 2026. And no, it’s not another banking meltdown or a typical recession cycle. This time, the pressure is sitting right at the core of the global system: sovereign bonds.

The first red flag? The MOVE index. Bond volatility is waking up.

Right now, three silent fault lines around the world are straining at the same time:

1️⃣ U.S. Treasury funding

2️⃣ Japan’s yen and carry-trade system

3️⃣ China’s overleveraged credit machine

Any one of these snapping would be enough to shake the world. All three converging in 2026? Everything falls apart.

Let’s start with the one building the fastest: a U.S. Treasury funding shock.

In 2026, the U.S. has to issue record levels of debt. At the same time, deficits are ballooning, interest costs are climbing, foreign demand is fading, dealers are stretched thin, and auctions are showing stress.

In other words: the perfect recipe for a failed or severely strained long-end Treasury auction.

And this isn’t speculation. It’s already visible in the data: weaker auctions, bigger tails, fading indirect bids, rising volatility at the long end.

If this feels familiar, it should. This is exactly how the UK’s gilt crisis kicked off in 2022. Only now, the scale is global.

Why does this matter so much? Because everything takes its cue from Treasuries: mortgages, corporate credit, global FX, emerging-market borrowing, repo markets, derivatives, collateral.

If the long end shakes, the entire system shakes.

Now layer Japan on top of this.

Japan is the world’s biggest foreign buyer of Treasuries, and the backbone of global carry trades. If USD/JPY rockets to 160–180, the BOJ has to step in, carry trades start to unwind, Japanese pensions sell foreign bonds… and Treasury volatility shoots even higher.

Japan doesn’t just get hit, it amplifies the shock.

And then there’s China.

Behind the curtain sits a $9–11 trillion local-government debt bubble. One major LGFV or SOE failure → yuan devalues → emerging markets panic → commodities jump → the dollar spikes → U.S. yields jump again.

China becomes the second amplifier in the chain.

So what actually sets off the 2026 event?

➡️ A weak U.S. 10-year or 30-year auction.

One bad auction could be the moment yields spike, dealers step back, the dollar surges, global funding tightens, and risk assets are forced to reprice all at once.

Here’s what happens next.

Phase 1:

Long-end yields explode higher.

The dollar rips upward.

Liquidity disappears.

Japan intervenes.

The offshore yuan drops.

Credit spreads widen.

Bitcoin and tech sell off hard.

Silver trails gold.

Equities fall 20–30%.

This is a funding shock, not a solvency crisis and it moves fast.

Then comes the inevitable central-bank response: liquidity injections, swap lines, Treasury buybacks, maybe even temporary curve control.

It stabilizes the system… but it floods it with liquidity.

And that liquidity sets off Phase 2.

Phase 2 is where the opportunity shows up: real yields collapse, gold breaks out, silver leads, Bitcoin recovers, commodities surge, and the dollar finally peaks.

That’s the start of the 2026–2028 inflation wave.

Why does everything point to 2026?

Because multiple global stress cycles are all hitting their peak at once.

And the early-warning signal is already blinking: the MOVE index is climbing.

When MOVE + USD/JPY + the yuan + 10-year yields all start pushing in the same direction…

…you’re looking at a 1–3 month countdown clock.

Final thought: The world can absorb a recession.

What it can’t absorb is a disorderly Treasury market.

2026 is when that pressure finally breaks.

First with a funding shock, then with the biggest hard-asset bull run of the decade.

15 sectors defining the next decade of investing

The megatrend map.

1. AI

$NVDA · $PLTR · $APP

The infrastructure king, the data layer, and the monetization engine. Three different ways to own AI.

2. Chips

$AMD · $AVGO · $MU

Compute, custom silicon, and memory. The full semiconductor stack.

3. Space

$RKLB · $ASTS · $PL

Launch infrastructure, satellite broadband, and geospatial intelligence. Pre-SpaceX IPO re-rating still unfolding.

4. ₿ Crypto

$COIN · $MSTR · $GLXY

Exchange infrastructure, BTC treasury play, and mining leverage. Three different risk profiles.

5. Energy

$VST · $NEE · $FSLR

AI power demand is the new oil shock. These three sit at the intersection of grid scale and renewables.

6. Drones

$AVAV · $KTOS · $ONDS

Autonomous defense and dual-use tech. Defense budgets are only going one direction.

7. Nuclear

$OKLO · $SMR · $LEU

The only baseload clean energy that hyperscalers can actually contract. Still early, still underpriced.

8. Robotics

$ISRG · $SYM · $PATH

Surgical precision, warehouse automation, and enterprise AI workflows. Labor replacement at scale.

9. Quantum

$IONQ · $RGTI · $QBTS

Highest risk on the list. Longest time horizon. Size accordingly — the upside is generational if it works.

10. Batteries

$QS · $LAC · $BE

Solid-state technology, lithium supply chain, and grid-scale storage. The energy transition needs all three.

11. Healthcare

$HIMS · $UNH · $LLY $MRNA

Diversified pharma cash flow, next-gen biologics, and mRNA platform optionality beyond COVID.

12. Photonics

$AAOI · $COHR · $LITE

The most underowned layer of AI infrastructure. Data centers need optical interconnects — demand is accelerating.

13. Rare Earths

$MP · $USAR · $FCX

Supply chain sovereignty is the new geopolitics. The West needs domestic rare earth and copper supply. Now.

14. Manufacturing

$ETN · $CAT · $GE

The physical backbone of AI buildout — power distribution, heavy equipment, and aerospace. Old economy, new tailwind.

15. Critical Minerals

$FCX · $UAMY · $CRML

Copper, lithium, and battery metals. Every AI data center, EV, and grid upgrade runs on these. The commodity cycle is structural.

This isn’t a buy list. It’s a framework.

Find your highest-conviction themes. Size appropriately. Think in years.

Not financial advice.

BREAKING: Bitcoin officially falls below $60,000 as selling pressure accelerates.

Total levered crypto liquidations are now up to $1.5 billion over the last 24 hours.

US petroleum stockpiles are draining at a rapid pace:

Total US crude and petroleum product inventories fell -10.6 million barrels last week, to 1.57 billion barrels, the lowest since 2004, according to the EIA.

This was driven by commercial and government crude stocks, which fell -15.9 million barrels, the 2nd-largest weekly drop on record.

The drawdown comes as exports to Asia and Europe are surging, with global markets scrambling to replace lost Middle Eastern supplies.

Before the Iran War, US crude and petroleum product exports were ~3.0 million barrels per day. They are now up to 13.6 million barrels per day, the 2nd-highest reading on record.

Meanwhile, the Strategic Petroleum Reserve fell another -7.9 million barrels last week, now down -58 million barrels since the start of the war, to 357 million barrels, the lowest since January 2024.

The US is acting as the lender of last resort for global oil markets.

🚨 EVERYTHING THAT COULD GO WRONG FOR MARKETS WENT WRONG TODAY.

S&P 500 down -1.65%, wiping out $1.14 trillion.

Nasdaq down -2.60%, wiping out $1.11 trillion.

Gold down -3.38%, wiping out $1 trillion.

Silver down -6.9%, wiping out $280 billion.

Bitcoin down -6.31%, wiping out $80 billion.

In total $2.5 TRILLION wiped out in a single session. These were not isolated moves. Everything started breaking at the same time.

It started with the jobs report this morning.

The US economy added 172,000 jobs in May. Wall Street expected 88,000. That is almost double.

On any normal day, strong jobs is good news. But inflation is already at 3.8% and oil is sitting at $90. A labor market this strong tells the Fed it cannot cut interest rates and may actually need to raise them.

The probability of a rate hike this year went from 40% to 57% in a single day. That spooked every investor holding tech and growth stocks because higher rates mean those stocks are worth less today.

Then the AI trade started cracking.

Yesterday Broadcom reported record earnings: revenue up 48%, AI chip sales up 143% and the stock still crashed 12.6%. The reason was simple.

Broadcom did not raise its AI revenue targets for the year. Investors had expected it to. That single miss made people ask a question they had been avoiding for months: are we paying too much for AI stocks?

That question got louder today when a research firm called SemiAnalysis revealed that Nvidia's next-generation AI chips will need significantly less memory than everyone assumed, roughly half of what the market was pricing in.

Memory chips are what companies like SK Hynix and Samsung make. SK Hynix fell nearly 10% today. Samsung fell over 6%.

South Korea's entire stock market crashed 5.5% in a single session. Japan's semiconductor stocks did the same.

And then Anthropic added fuel to the fire by publishing a report warning that AI is getting close to the point where it can improve itself without human help and calling for a global pause in AI development.

Coming on the same day as the memory demand news and Broadcom's miss, it fed a single growing fear across the market: what if the AI boom is moving faster than the business models can keep up with?

Underneath all of this, there is a liquidity problem nobody is talking about.

SpaceX goes public next week at a $1.75 trillion valuation. Anthropic just filed to go public. OpenAI is next.

These three companies together are worth $4 to $5 trillion. Fund managers need cash to buy into these listings.

But cash levels are already at their lowest since early 2024. The only way to raise cash is to sell what they already own. That selling is happening right now.

The new Fed Chair Kevin Warsh will also hold his very first policy meeting in 11 days. He was appointed by Trump with the expectation of cutting rates.

He is now walking into a situation where inflation is high, oil is high, and the job market is running hot. Investors do not know what he will do.

When nobody knows what the most powerful central banker in the world will decide in less than two weeks, the safest move is to reduce risk today.

Everything that could go wrong, went wrong at the same time. A hot jobs report, a collapsing ceasefire, a crack in the AI trade, a trillion dollar liquidity drain, and a Fed meeting with no clear outcome.

🇨🇳 Censorship in China is backfiring now that young Chinese are secretly learning about the Tiananmen Square massacre.

Even with AI scrubbing every trace of June 4, 1989 from the internet, China’s Gen Z is finding the truth anyway... and often in the weirdest ways!

Olympic skater Alysa Liu’s dad was a Tiananmen protester who fled.

When she won gold, Chinese netizens exploded: some called him a traitor, others got curious.

One 20-year-old Wuhan student dropped a hint on RedNote and her comment got nuked in hours.

Teens are stumbling on it through random livestreams and digging behind the firewall.

They come out stunned: “I had no idea the protests were that huge” or “my whole worldview just collapsed.”

The regime’s total blackout is actually creating curiosity bombs.

Young Chinese are horrified when they learn students were shot and tanks rolled over people, and some now want out.

Truth will always find cracks.

Even the Great Firewall can’t stop it forever.

Source: Washington Post

This market has given more returns in 8 weeks that usually $QQQ gives in 8 years.

This scares shit out of me but i believe its not dot com type of bubble or hype. This is industry shifting. AI is generating revenue, companies are growing and we are definitely seeing growth overall.

Market gave us more money in past 8 weeks than most of us ever expected in such a short time.

Loving this momentum

My 2 cents

Every bubble breeds accounting fraud, this one is no different:

- Circular financing booked as revenue

- Creating private shell entities to hoard unsold products

- Hiding the true cost of depreciation

- Meta & Google buying fugazi ads on their own platforms to fluff up revenue

Investing in the stocks from these 9 groups could potentially make you wealthy by 2030.

Semiconductor:

1. $INTC

2. $AMBQ

3. $NVTS

4. $AMD

5. $ARM

6. $WOLF

Critical Minerals:

1. $USAR

2. $UUUU

3. $CRML

4. $MP

5. $UAMY

Space:

1. $RKLB

2. $FLY

3. $SATL

4. $PL

Energy:

1. $AMPX

2. $EOSE

3. $TE

Memory/Storage:

1. $SNDK

2. $MRAM

3. $SIMO

4. $WDC

5. $MU

6. $DRAM

Optical/Photonics:

1. $AAOI

2. $AXTI

3. $LWLG

4. $LITE

5. $COHR

Quantum:

1. $IONQ

2. $QBTS

Nuclear:

1. $OKLO

Defense:

1. $OSS

2. $PLTR

3. $ONDS

The best way to beat the general market for a long term is to pick the best ones from each sectors!

5 ETFs Dominating AI, Power, Space & Robotics

$DRAM — Invests in memory chip companies. Bets on the companies storing and moving AI data faster than ever.

$NLR — Invests in nuclear energy. Bets on uranium miners and reactors powering the AI electricity boom.

$NASA — Invests in space companies. Bets on satellites, rockets, and the businesses building the space economy.

$HUMN — Invests in robotics and AI. Bets on companies building the physical robots that will replace human labor.

$EUV — Invests in semiconductor equipment. Bets on the machines that print the world’s most advanced chips.

$SMH — Invests in semiconductors broadly. Bets on the companies designing and manufacturing the chips powering everything.

$GRID — Invests in electricity infrastructure. Bets on the companies upgrading power grids to handle surging energy demand.

Just in case people are wondering about my track record with European equities:

$RPI: $280 -> $800 (agentic AI hardware demand thesis).

$LPK: ~$6, thesis at $13 -> $24.2 (glass cores substrates close monopoly)

$SOI: $44 -> $181 (silicon photonics, monopoly over substrates)

$SIVE: $4 -> $71 (CPO, critical chokepoints over lasers).

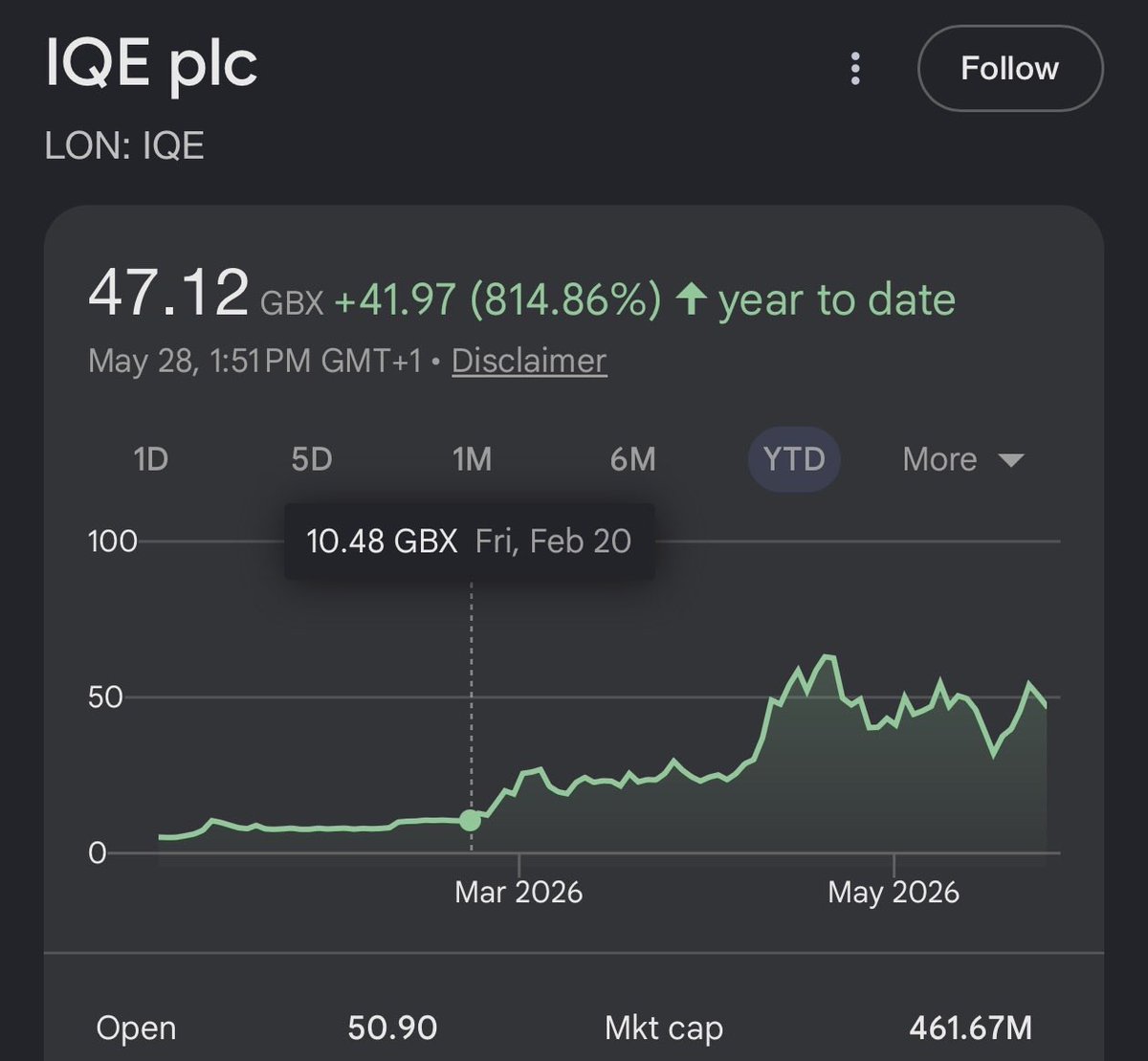

$IQE: $12 -> $47 (latent epiwafer capacity, information discovery around downstream photonics companies).

$ALRIB: $5 -> $15 (duopoly, synthesis around quantum buyers with photonics growth verticals).

And now $XFAB at $9.

I’m not always right.

But every single one of my European longs thesis have been validated so far by either earnings, investments (eg. $MTSI in IQE) or market returns.

AI capex expected to be $7.6 Trillion from 2026-2031 according to Goldman Sachs.

All of this capital flows upstream into mission-critical segments like:

- Memory with $MU & $SNDK

- Photonics with $SIVE & $LITE

- Substrates with $GLW & $AXTI

- Foundries with $INTC & $TSEM

- Neoclouds with $NBIS

And loads more.

We're literally at the start of the structural AI inflection point.

Where the value chain winners will benefit from surging demand + profitability.

All fuelled by hyperscalers like $GOOGL, $META + $AMZN tooling up for the AI arms race.

Rosenblatt InP lasers checks:

According to our checks, NVIDIA, which is the driving force behind scale up CPO, asked the supply chain to increase InP laser capacity by ~20x from 2025-2030. The vendors appear to have taken a more conservative stance, agreeing to an ~12x increase ( $AAOI / $LITE etc)

Chevron is letting customers know in California that it’s not Donald Trump causing the insane gas prices in the state, it’s California Democrats

Chevron just added these new signs to their pumps educating customers, “Sacramento policies did this. Now you pay more”

“California politicians are choosing foreign oil and fuels over local jobs and lower costs”

This is what we need. Huge companies willing to educate the public and tell the truth

It’s Gavin Newsom and Democrat policies causing $6.30+ average cost per gallon in California