AI INFRASTRUCTURE BUILDOUT (Cheat Sheet)

Top 3 names in each Sector:

AI Memory / Data Storage

$MU Micron

$SNDK Sandisk

$WDC Western Digital

→ AI can’t train or run without fast, scalable data storage.

AI Networking / Interconnects

$AVGO Broadcom

$MRVL Marvell

$ALAB Astera Labs

→ Chips are useless if they can’t talk to each other fast enough.

AI Compute & Data Centers

$CIFR Cipher

$IREN Iris Energy

$WULF TeraWulf

→ AI lives in physical data centers, not “the cloud.”

Power, Cooling & Electrical Infrastructure

$VRT Vertiv

$ETN Eaton

$PWR Quanta Services

→ Existing grids weren’t built for AI power and heat loads.

Semiconductor Manufacturing & Equipment

$ASML ASML

$LRCX Lam

$KLAC KLA

→ No advanced tools means no advanced chips.

Power Grid Bottleneck (Copper)

$FCX Freeport

$SCCO Southern Copper

$TECK Teck

→ Every grid, data center, and defense system bottlenecks here.

Nuclear / Energy Security

$CCJ Cameco

$LEU Centrus

$OKLO Oklo

→ AI and electrification need reliable, baseload power.

Autonomy / Physical AI

$TSLA Tesla

$RR Richtech Robotics

$SYM Symbotic

→ AI is moving off screens and into the real world.

Drones & Autonomous Defense

$AVAV AeroVironment

$KTOS Kratos

$ONDS Ondas

→ Modern warfare is shifting toward unmanned systems.

Space & Defense Infrastructure

$RKLB Rocket Lab

$ASTS AST SpaceMobile

$RDW Redwire

→ Satellites are now core infrastructure, not exploration.

ONDS-reversed from 20 day Ema

IREN-reversed from 20 day Ema

SERV-reversed from 50 day Ema

NBIS-reversed from 50 day SMA

Could go on and on…

Key intraday MA Reversals for many, many more stocks today

LFG! 🚀🚀

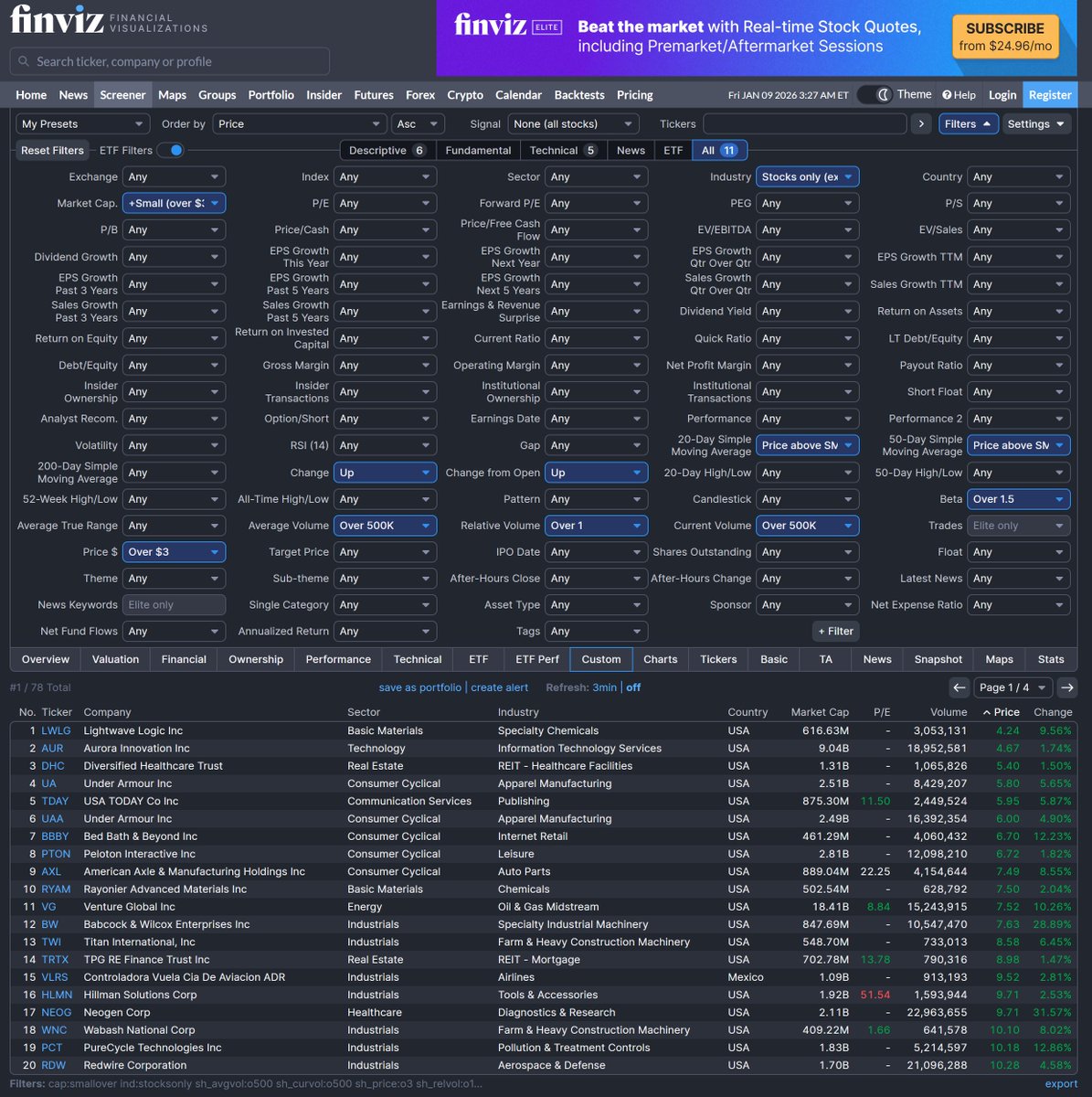

*** FREE *** Finviz Screener By @RealJGBanks

For anyone unfamiliar with Finviz and how to setup this screener, this is how your screen should look if you apply the filters as outlined.

There should be 79 names at present.

This is a direct link to the screener (sorted by market cap):

https://t.co/H8g1qafltP

⚠️Note: The scan will work only in market hours and after close as it includes Relative Volume, Change and Change From Open criteria. Once premarket starts, the scan will likely return few (if any) results.

Link to original post included.

Hope it helps 🤝

Personally as a suggestion to newer traders, may want to add Price >= SMA200 too.

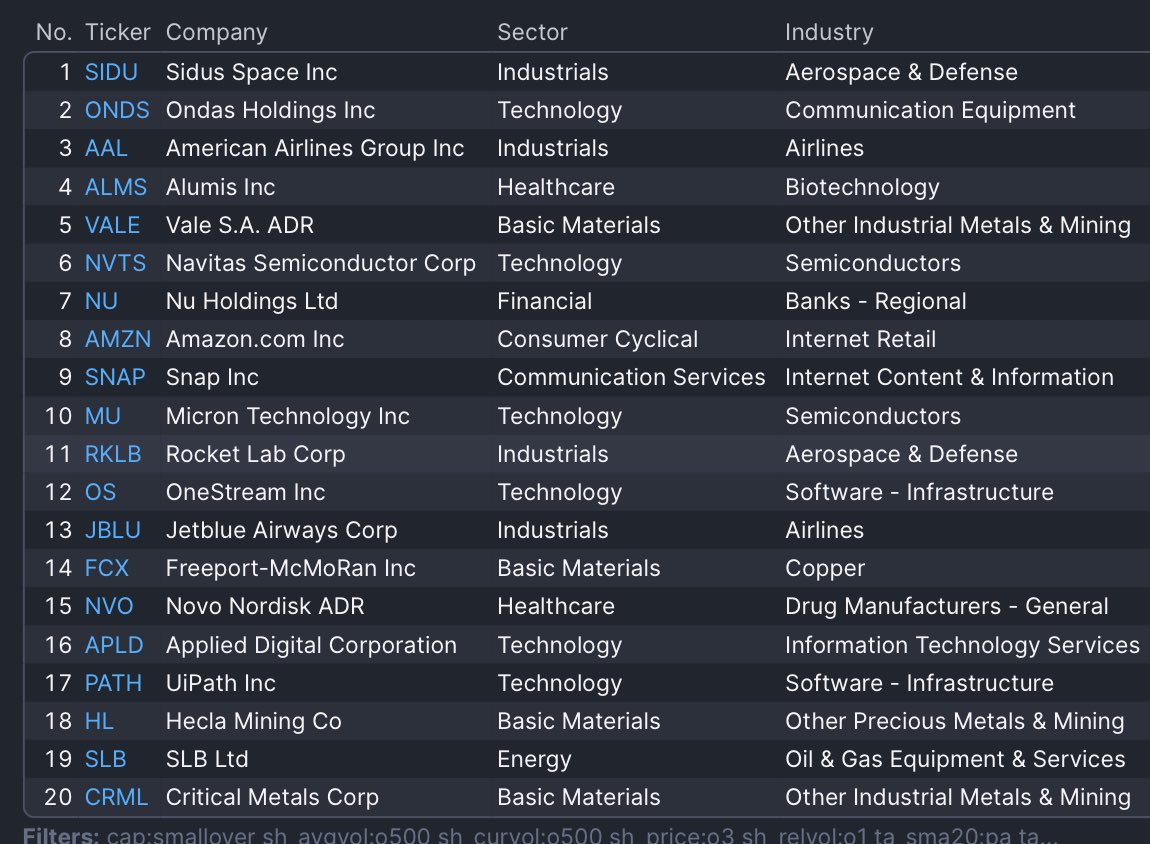

I know for a FACT this is one of the best scanners

It consistently shows the cleanest setups

It finds the hot names like

$ONDS $MU $RKLB $PATH $SIDU $AMZN

Dropping the Link to this scanner for FREE

RT + LIKE +COMMENT “BANKS” TO RECIEVE IT ❤️

Dear AI Bears: Thank You For The False Narrative And The Cheaper Prices (Part 3)

I’ll start by thanking the AI bears for grasping at any detail no matter how small, distorted, or taken out of context when building their case against the AI revolution. On Wednesday, Oracle ($ORCL) reported Q2 earnings for the 2026 fiscal year and gave the bears something new to cling to. Oracle has decided to go all-in on AI and cloud, but it is doing so by tapping the debt markets rather than primarily funding this buildout through operating cash flow. In Q2, total revenue came in at $16.1 billion, and we continued to watch a legacy technology titan transform itself.

Cloud IaaS and SaaS accounted for $7.98 billion of total revenue, up 34% YoY. Meanwhile, the on-prem and software licensing business declined 3% YoY to $5.88 billion, highlighting the continued shift from legacy software to the cloud. Cloud Infrastructure (IaaS) generated $4.1 billion in revenue, up 68% YoY, while Cloud Applications (SaaS) grew 11% YoY to $3.9 billion. Oracle is staking its future on cloud and AI but the issue has become the funding approach. Bears have repeatedly cited the scale of hyperscaler CapEx, and Oracle just increased long-term debt from $82.24 billion to $99.98 billion. Citi published a research report indicating Oracle may need to raise $20–$30 billion in debt annually over the next three years based on the company’s expansion plans.

The bears finally got what they wanted. They can point to Oracle and argue:

· Negative net liquidity

· Reliance on debt markets

· Operating cash flow that cannot currently support CapEx objectives

This has contributed to commentary like the following on major finance shows such as Power Lunch:

“I think Michael Burry kind of suddenly made us realize that there really are a lot of uncertainties with regards to the future growth rate of these Magnificent Seven companies that are now competing in this AI race and in addition we know that there’s a lot of question marks about whether all this capital spending is going to pay off with a decent return. So suddenly there is a lot of uncertainty about the projections for strong growth in these seven companies.”

I’m happy to have a serious, intellectual discussion on this topic, because I believe the AI bears are wrong and ultimately fighting a losing battle. Technology does not remain stagnant, it advances. The Magnificent Seven are arguably the strongest collection of businesses ever created, led by some of the most capable management teams in corporate history. We are not watching one company making an isolated bet on a radical idea that may or may not work. These companies are actively building products and services around AI because AI has already been established as the next frontier of computing. Can we really take the bear case seriously when the executive teams at $NVDA $MSFT $META $AMZN $GOOGL $AAPL $TSLA have built trillion and multi-trillion-dollar businesses are signaling that we are still early in the AI cycle and that this is the future? I would rather listen to Andy Jassy, Sundar Pichai, Elon Musk, Mark Zuckerberg, Jensen Huang, and Satya Nadella than a cohort of bears on the sidelines who do not work in technology and have no involvement in the direction these companies are taking.

Statements like “there are question marks about whether all this capital spending is going to pay off with a decent return” are frustrating because they often sound like conclusions drawn from market caps and P/E ratios rather than from earnings calls, quarterly filings, and the operating results that have been unfolding for years. The statement is simply not supported by what we have been watching in real time. We have also seen what happens when CapEx is not treated as a priority.

Here are the facts:

In fiscal 2021, $AAPL allocated $11.09 billion to CapEx. Apple then allocated $10.71 billion in fiscal 2022, $19.96 billion in 2023, $9.45 billion in 2024, and $12.72 billion in 2025 for a total of $54.92 billion over the past five years. Since fiscal 2021, Apple increased annualized CapEx by $1.63 billion (14.7%). Over the same period, Apple generated $365.82 billion in revenue in fiscal 2021, which grew by $50.34 billion (13.76%) over the next four years to $416.16 billion. Apple’s cash from operations increased 7.16% ($7.44 billion) over the same period from $104.04 billion to $111.48 billion.

Now look at what happens when $MSFT, $GOOGL, $META, and $AMZN take CapEx seriously.

In fiscal 2021, Microsoft allocated $20.62 billion to CapEx, which grew 213% ($43.93 billion) to $64.55 billion in fiscal 2025. Over this five-year period, Microsoft allocated $181.64 billion toward CapEx. The impact on financial performance was substantial. In fiscal 2021, Microsoft generated $168.09 billion in revenue, which increased 67.61% ($113.64 billion) to $281.72 billion. Cash from operations increased 77.43% ($59.42 billion) over this period from $76.74 billion to $136.16 billion.

Microsoft was not an outlier. Google, Amazon, and Meta had similar outcomes.

In fiscal 2021, $GOOGL allocated $20.62 billion to CapEx, which increased 216.04% ($53.23 billion) to $77.87 billion in the TTM. Over the past five years, Google has allocated $218.78 billion to CapEx. Google’s revenue increased by $127.84 billion (49.62%) from $257.64 billion in 2021 to $385.47 billion in the TTM. Google’s cash from operations increased 65.22% ($59.77 billion) over the same period from $91.65 billion to $151.42 billion.

Meta is a similar story. Meta’s CapEx increased 235.65% ($44.04 billion) over the same period, rising from $18.69 billion in 2021 to $62.73 billion in the TTM. This supported revenue growth of 60.65% ($71.53 billion), from $117.93 billion to $189.46 billion. Meta’s cash from operations expanded 86.49% ($49.89 billion) from $57.68 billion to $107.57 billion from 2021 to the TTM.

For anyone to say there are “question marks” about whether this level of capital spending will produce a decent return is to ignore what has been happening quarter by quarter. Apple’s CapEx intensity increased modestly versus peers, while cloud and platform peers dramatically increased infrastructure investment and saw corresponding growth in revenue and operating cash flow.

I believe the bears finally got what they wanted with Oracle’s earnings because Oracle has become a convenient scapegoat for the broader AI bear case. Oracle has $19.77 billion in cash and short-term investments and $0 in long-term investments. Long-term debt now stands at $99.98 billion, putting net liquidity at -$80.22 billion. Oracle also generated $22.3 billion in operating cash flow over the TTM while allocating $35.48 billion toward CapEx, resulting in FCF of -$13.18 billion (operating cash flow minus CapEx, as reported). Bears finally have a metric they can latch onto but Oracle is one company, and its balance sheet structure does not define the rest of the AI ecosystem.

Bears should also keep in mind that debt funding is not automatically a problem; mismatch is. If Oracle’s RPO converts to revenue and margins hold, the funding mix could prove highly profitable. It is premature to treat Oracle as the definitive “poster child” for the AI bear thesis.

Now compare Oracle’s position to the hyperscalers.

Google has $98.5 billion in cash and short-term investments and another $63.8 billion in long-term investments. With $21.6 billion in long-term debt, Google’s net liquidity position is $140.69 billion. Google could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Google generated $151.42 billion in operating cash flow, exceeding the $77.87 billion allocated to CapEx, producing $73.55 billion in FCF.

Microsoft has $102.01 billion in cash and short-term investments and another $10.28 billion in long-term investments. With $35.38 billion in long-term debt, Microsoft’s net liquidity position is $147.04 billion. Microsoft could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Microsoft generated $147.04 billion in operating cash flow, exceeding the $69.02 billion allocated to CapEx, producing $78.02 billion in FCF.

Meta has $44.45 billion in cash and short-term investments and another $25.07 billion in long-term investments. With $28.83 billion in long-term debt, Meta’s net liquidity position is $40.69 billion. Meta could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Meta generated $107.57 billion in operating cash flow, exceeding the $62.73 billion allocated to CapEx, producing $44.84 billion in FCF.

Amazon has $94.2 billion in cash and short-term investments and another $20 billion in long-term investments. With $57.94 billion in long-term debt, Amazon’s net liquidity position is $56.26 billion. Amazon could eliminate 100% of long-term debt tomorrow without impairing its short-term liquidity. In the TTM, Amazon generated $130.69 billion in operating cash flow, exceeding the $120.13 billion allocated to CapEx, producing $10.56 billion in FCF.

While Oracle has negative net liquidity and negative FCF, the combination of Google, Microsoft, Amazon, and Meta tells the opposite story. Together, they hold $339.15 billion in cash and short-term investments and another $119.16 billion in long-term investments. After accounting for $143.76 billion in long-term debt, they still have a net liquidity position of $314.55 billion while generating $536.73 billion in operating cash flow and producing $206.97 billion in FCF. Bears can point to Oracle all they want, but Oracle’s situation does not impact Amazon, Meta, Microsoft, or Google and it does not change the trajectory of the AI revolution.

I also believe many bears have not been reading the earnings calls. If they had, they would see the AI narrative remains firmly intact. Don’t worry I’ll do the work for them:

MSFT

• MSFT guided to increase total AI capacity by 80%+ this year and to roughly double total datacenter footprint over the next two years

• MSFT highlighted a new flagship AI datacenter expected to scale to 2 gigawatts and go online next year

• Reported deploying the first large-scale cluster of NVIDIA GB300s and improving token throughput for GPT-4.1 and GPT-5 by 30%+ per GPU

• Azure AI Foundry scale of ~80,000 customers

• Commercial RPO increased 50%+ to nearly $400B, with a 2-year weighted average duration

GOOGL

• Reiterated a full-stack AI approach and highlighted scaling both NVIDIA GPUs and Google’s TPUs

• Announced shipping A4X Max instances powered by NVIDIA GB300 to Google Cloud customers

• Gemini processing 7B tokens per minute via direct API use

• Gemini app 650M MAUs with queries up 3x QoQ

• Rolled out AI Mode globally across 40 languages, scaling to 75M+ daily active users with Search

• 70%+ of existing Google Cloud customers use AI products as they emphasized larger deal momentum

• GenAI model product revenue growth 200%+ YoY

• Launched Gemini Enterprise 2M+ subscribers across 700 companies

• Google Cloud backlog grew 46% QoQ to $155B

AMZN

• AWS grew 20% YoY to $33.0B in Q3 (re-acceleration)

• Project Rainier launched a large AI compute cluster with 500,000 Trainium2 chips to build & deploy Anthropic’s Claude models

• Announced Amazon EC2 P6e-GB200 UltraServers using NVIDIA Grace Blackwell Superchips for training/deploying very large models

• Backlog/RPO (AWS) to $200B with additional deal activity after quarter-end

META

• AI recommendations drove engagement with 5% more time spent on Facebook and 10% on Threads in Q3 attributed to recommendation improvements; strong video momentum; and Reels scale commentary

• More than 1B monthly actives already use Meta AI, with usage rising as model quality improves

• Meta described capital deployment priorities as centered on AI products/models/business solutions and outlined steps to increase capacity

• Meta highlighted the scale of business messaging and the goal of using Business AIs to help businesses automate/sell/support at low cost

ORCL

• RPO at $523B, up $68B sequentially and up 438% YoY

• RPO to be recognized in the next 12 months grew 40% year over year

• 211 live and planned regions worldwide

• More than halfway through building 72 multicloud datacenters embedded inside AWS, Google Cloud, and Microsoft Azure

• The multicloud database business is up 817% in Q2

• All top-five AI models are available in Oracle Cloud, including OpenAI, xAI, Google, and Meta models

• Cloud revenue at $8B (up 33%) now accounts for half of Oracle’s total revenue

• Cloud Infrastructure revenue at $4.1B, up 66%, with GPU-related revenue up 177%

• Cloud database services up 30%; Autonomous Database up 43%; multicloud consumption up 817%

At the end of the day, the AI bear case increasingly depends on taking a company-specific funding decision and projecting it onto an entire technology cycle that is being funded very differently by the companies actually leading it. Oracle may have chosen a more aggressive balance sheet path to accelerate capacity which creates real execution and timing risk but it does not invalidate the broader thesis. The hyperscalers and platform leaders are not hoping AI works as they are actively monetizing it today. We are witnessing the hyperscalers expand backlog and remaining performance obligations, and converting infrastructure investment into revenue growth and operating cash flow in real time. If someone wants to debate valuation, competitive dynamics, or the pace of demand, I’m all for it but the lazy narrative that “CapEx won’t earn a decent return” ignores what we have already witnessed since 2021. The companies investing the most aggressively are the same companies expanding revenue, widening cash generation, and strengthening strategic moats.

Oracle is not proof that AI is a bubble. At most, Oracle is proof that funding choices matter and that execution matters. Meanwhile, the builders are telling you, quarter after quarter, that demand is still ramping, capacity is still constrained, and the opportunity set is still early. So yes, thank you AI bears for the cheaper prices and the recycled fear narrative. I’ll keep reading the filings, listening to the calls, and following the cash because when this cycle is judged in hindsight, it won’t be decided by who posted the best skepticism on TV. It will be decided by who built the infrastructure, captured the workloads, and compounded cash flows over the next decade.

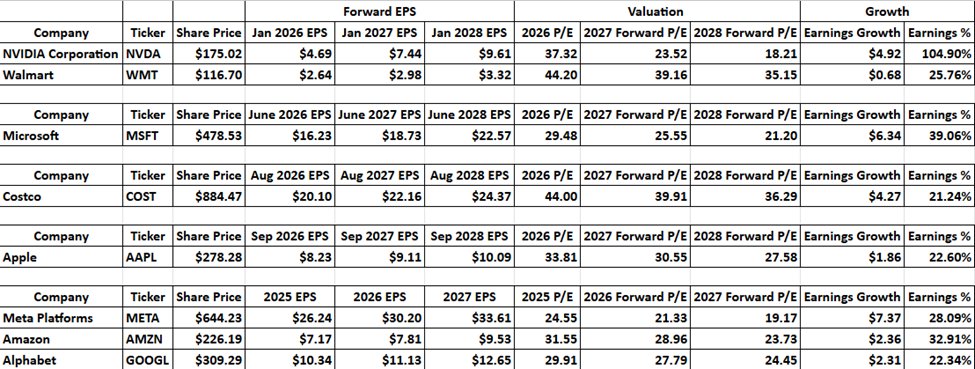

The reality is that the AI Bears just made great companies such as $NVDA, MSFT, AAPL, META, AMZN, and GOOGL cheaper on a forward basis. Below is a table I constructed based on the current fiscal year and the next two fiscal years. NVDA, WMT, MSFT, COST, and AAPL do not report on calendar years so you will see Jan 26, June 26, Aug 26, and Sep 26 to represent their current fiscal years then the next two years of consensus estimate projections to showcase the forward growth rates. META, AMZN, and GOOGL report on a calendar year so it will be a traditional 25,26,27 for the years.

Currently $WMT trades at 44.20 times Jan 26 earnings and 25.15 times Jan 28 earnings with 25.76% of EPS growth over the next two years. $COST trades at 44 times Sep 26 earnings and 36.29 times Sep 28 earnings with 21.24% EPS growth.

I am welcoming the ability to add to my positions in NVDA at 37.32 times Jan 26 earnings with an expected 104.90% EPS growth over the next two years which puts NVDA trading at 18.21 times Jan 28 earnings. NVDA is effectively a value stock here.

Investors are also able to add to META at 19.17, AMZN at 23.73 times, and GOOGL at 24.45 times 2027 earnings. MSFT is trading at 21.20 times June 28 earnings while AAPL is trading at 27.58 times Sep 28 earnings.

There are always pockets of the market that are expensive but its not lurking within the financials of NVDA, META, AMZN, MSFT, AAPL, and GOOGL. If we experience a continued drawdown these companies will get even cheaper on a forward basis so thank you AI Bears for allowing me to pick up more shares of companies I was planning on adding to anyway at lower forward valuations. In the short-term your help is always appreciated, and in the long-term I believe your likely to miss out on a tremendous amount of appreciation.

@amitisinvesting@KrisPatel99@RealMattMoney@Futurenvesting@FunOfInvesting @Kross_Roads @StockMarketNerd@sam_badawi@dhurstell@DivesTech@fundstrat@ChrisCamillo@altcap

@FranVezz 50 day Ema is 217.68. It’s tightening up right above it. I think it’s breaking out from here and ready to bust higher as soon as we get some upside volume. Volume has been super low since 11/21

The key to great trading: stop judging yourself and stop forecasting. When conditions are bullish, act bullish; when they’re bearish, adjust. Trust your process. You’ll buy stocks that go to zero and sell some that go to infinity—the key is what you do in between. You will make many mistakes; you’ll never trade perfectly. You can only learn to perfectly trade your plan. Making mistakes is trading. Mitigating them is professional trading.

“For him who has conquered the mind, the mind is the best of friends; but for one who has failed to do so, his mind will remain the greatest enemy.”

― Bhagavad Gita

the eth core devs don’t tweet a lot about just how hard the work that they do is so let’s talk about it:

1. every line of code they merge can move more money than most banks process in a quarter. there is no staging server for that.

2. they swap consensus logic for a 400B + dollar economy without scheduling downtime. ever.

3. they coordinate hundreds of researchers, auditors, and client teams across time zones, cultures, and philosophies, yet ship like a single mind.

4. they do it all in public, with every decision dissected by the loudest peanut gallery on the internet, and still keep the vibe collaborative.

5. they design for attackers who have nine figure incentives and infinite patience. then they sleep anyway.

6. they keep six independent clients in perfect sync so the same block lives at the same height for every node in the world.

7. they turn bleeding edge research into production code while preserving backwards compatibility for machines that went online before defi even had a name.

8. they debug issues that only happen once a year on a single archive node because someone somewhere will rely on that edge case.

9. they write cryptography that must stay unbroken for decades while the math itself evolves beneath their feet.

10.when the upgrade lands smooth the outside world shrugs. inside ethereum we know it was a minor miracle. every successful fork proves that decentralized coordination can outperform the world’s best hierarchies and shows that open internet capital markets are now the default.

thank you, truly.

we owe you everything.