Book Lover | Championing common sense, embracing the unfiltered reality. Here for the stories that challenge the mainstream. #RealTalk#InspiredByTruth"

So basically, every skilled worker is given the Copilot for “free,” because in some cases the AI will be wrong and will need the skilled field worker to correct it so it can learn. Not all real-life situations are straightforward; sometimes they require thinking and analysis to solve an issue. I guess it’s a great way to get people with specialized knowledge to teach the AI the nuances of their trades at no major cost to the developer! Eventually, when the AI is good enough, the field workers would most likely be required to pay a subscription. It would be interesting to see how it applies in real life and how accurate the output is.

He should have used AI before the sale of the business lol! To advise him how to structure the sale, there is a big difference in ordinary and capital gains! Also, wonder if AI classified some of the gain to personal goodwill if applicable! There were many things to consider before uploading his info into an AI platform and brag about how well it performed!

@Bostonbean90@bradncpa I get what you are saying, I was more thinking from the practical standpoint and possible client exposure after an s-election, so I sent myself into a rabbit hole reading about it, like I have nothing better to do in the middle of tax season lol!

The original comment was regarding a CPA advising a client to make an S election at a certain income level. You brought up the anti-abuse statute, and I wasn't sure how it's relevant to the S corp election! Nowhere on the election form are you required to list your intentions, and I wondered even more if there was case law used as precedent where the IRS disallowed certain deductions using the statute in question for an S corp, concluding that the S election was made in order to evade taxes.

@Bostonbean90@bradncpa Agree on the SE avoidance not being congressional intent, but was unable to find a case where this specific section was applied to an s-corp and resulted in the gov winning the case! You mentioned you know of many, share so we can educate ourselves!

I would like to see at least one case where S-election was disallowed based on sec. 269! Please share! 2553 and 8832 elections determine tax classification(treatment) not the legal creation of the corporate entity. Incorporation is a state-level legal process, while these elections are IRS federal tax processes. “Modern Home Fire & Casualty Insurance Co. v. Commissioner, 54 T.C. 839 (1970): The Tax Court explicitly held that Section 269 does not apply to disallow an S election, even if the sole motivation was to offset corporate income against the owner’s losses. The court reasoned that enjoying Subchapter S benefits is “consistent with the intent of Congress” and thus not tax avoidance.”

@Bostonbean90@bradncpa To my understanding, Sec. 269 is irrelevant here! It covers acquisitions, not S elections! Feel free to correct me if I am wrong, but I do not find language in the statute addressing entity elections.

There are many tax myths circulating on social media, in the news, and even in casual conversations. A common one during tax filing season is that tax refunds are something to celebrate.

https://t.co/601bvlSUVh #taxseason#irs

Just having some coffee and getting ready for a fun-filled day at work. Refresher on some Tax Court hall of shame:

• Al Capone: Guns? Nah, taxes did him in.

• Leona Helmsley: “Little people pay taxes”—says the billionaire who got jail time.

• Chesty Love: Deducting boob jobs as “biz tools”? Denied!

• Ugly mini donkeys: Hairball hobby losses? Approved.

IRS: Where dreams die hilariously. Your fave tax flop? 😈💸 #TaxTwitter #CPALife

Just in time lol! Wonder how many individuals already filed!!!! IRS published schedule taxpayers will use to claim deductions on no tax on tips, no tax on overtime, no tax on car loans, no tax on seniors https://t.co/G7UNjQzedV

With tax season underway, millions of Americans are gathering the necessary paperwork to file their income tax returns, which for many is a time-consuming, resource-intensive, and tedious task.

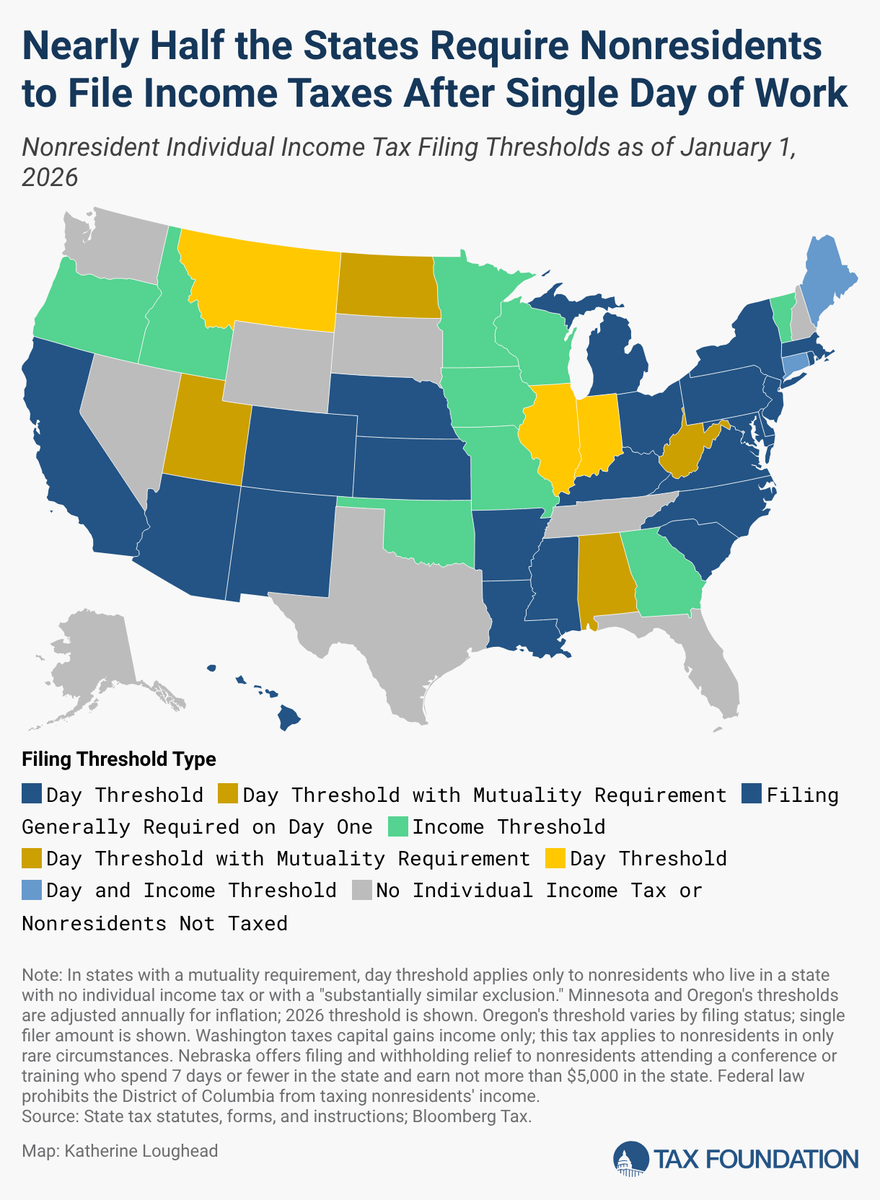

How does your state compare? https://t.co/6Kspjzfxhz

“§163(j) planning alert for 2025+: OBBBA restores EBITDA-style ATI (add back dep/amort/depletion) → 30% limit often much higher for capital-intensive biz. More deductible interest now!

Key strategies:

•Maximize ATI in ’25 (accelerate deductions? time capex?)

•Model carryforwards

•Revisit real prop/farm opt-outs

2025 sweet spot: Use dep add-back to boost ATI & deduct more interest. Consider accelerating large carryforwards from prior years while limit is generous.

But heads up—2026+ change: Elective interest capitalization no longer bypasses 163(j) (applied first, except mandatory under 263A(f)/263(g)). Old workaround gone!

Plan debt/interest timing accordingly.

Don’t forget small biz exemption: Avg gross receipts ≤$31M (2025 threshold, indexed) = full interest deduction, no limit. Aggregation rules apply—review controlled groups!

For leveraged clients: Restructure debt, generate biz interest income, or elect out if qualifying trade/business.

#CPA #TaxTips #BusinessTax #TaxTwitter

@BuffCpa@Taxsavvyjessica@Budgetdog_ Haha! Same, waiting for AI to crank out 48 multi-state 1065! Plz!! Losing it over all the PTE, composite, franchise & withholding state reqs & tax planning!