SK Hynix is coming to USA.

$DRAM is your best choice for the maximum exposure.

$RAM is 2X of $DRAM

$MUU is 2X of $MU

$DRAM $RAM is your safety net for more than 1 stock exposure.

If you guys think $AAPL price hikes are bad, wait until you see what happens to the other OEMs in consumer hardware

Apple has enormous leverage through its sheer size & Sourcing team. Most other consumer electronics OEMs by comparison are likely going to get steamrolled

Long post, but some thoughts on what happened in the market today…

Today was a particularly weird storm of price action because the logic going into the open was as follows:

- $MU crushed, saved the AI trade

- AI stocks should go higher due to MU proving its not cyclical, this should help the broader market get a lift

Instead, what we got right before the open…

- $AAPL announces massive price hikes and effectively uses MU earnings to be like, “See! It’s not us, but if memory gets 86% margins, then we have to raise prices!”

- This happens right after the hottest PCE in 3 years is reported, even with oil (the biggest proponent of inflation the past few months) still coming down

- Microsoft then joins the party and raises prices across all XBOX products, once again citing memory costs

Market then proceeds to take a nasty dip in every sector…except Memory.

I think what is happening here will be studied for a long time. The hyperscalers, the companies that are RESPONSIBLE for $MU and $SNDK being multibaggers, are getting destroyed because…well they can’t buy back stock, they can’t get FCF positive, and they don’t have memory’s pricing power.

In fact, this is what Melius Research came out today and said:

“Why bother owning a hyperscaler who can't buy back stock any time soon? Micron can start buying over $25B/quarter in stock during CY27. Memory will go down as THE BOTTLENECK of ALL BOTTLENECKS for this AI era. MU said that current conditions last after calendar 2027, basically guaranteeing buybacks of epic proportions, especially next calendar year.”

We are at the point where the sell-side is saying that owning the best companies in the world makes no sense when you can own the bottleneck of all bottlenecks.

Here’s the thing: I don’t know if Melius is actually wrong.

My gut tells me that 86% gross margins will not last forever, but as long as the hyperscalers are willing to pay, then the structural logic for market participants comes down to a simple question: why own the companies paying the capex over the companies benefiting from it?

The problem is obvious: if memory inflation continues to be intense, it will affect every part of the market. From automotive to datacenters to PCs. $NVDA gets to have a tax because it’s building very IP-heavy products. Will the market allow something like memory, that is not IP-heavy, to force consumers globally to pay significantly more for the products? Also, do the memory makers even care because as long as they control supply, they can control pricing?

I’d imagine the big tech companies either lower capex to stop paying the cost, keep paying the cost, or try to innovate. They likely won’t lower capex and will most likely continue paying the cost, so there probably are some elements of them trying to focus on innovating in this area…but if there won’t be any menaingful cutoff in capex, the memory story continues.

The market fell today because higher inflation means more of a chance for rate hikes. I mean, NVDA went below 200 as MU hit all time highs. NVDA’s suppliers are more valuable than NVDA’s biggest customers. As a result, it’s creating a type of AI-flation that basically led the market to sell off everything else.

Not sure how this plays out, retail continues to buy the dip and today’s red probably gets bought…especially as earnings continue to grow…but we are in a new paradigm for how this market gives a premium to a stock and if you have pricing power over a component that matters to build AI vs being a companies that actually uses AI, you get a premium.

$ARM | TD Cowen reiterates 𝐁𝐮𝐲 on 𝐀𝐫𝐦 𝐇𝐨𝐥𝐝𝐢𝐧𝐠𝐬, 𝐫𝐚𝐢𝐬𝐞𝐬 𝐏𝐓 𝐭𝐨 $𝟒𝟕𝟓 𝐟𝐫𝐨𝐦 $𝟐𝟔𝟓

Analyst sees ARM benefitting as agentic AI shifts work from GPUs' "thinking" to CPUs' "doing", finding its $15B FY31 AGI CPU target reasonable.

$NOK is expanding its autonomous network push with $AMZN AWS and Databricks.

Nokia is packaging agentic AI, digital twins and closed-loop operations into a platform it says has already helped operators reach 90%+ automation and cut network slice rollout times by up to 85%.

Commentary: ServiceNow is Claude's largest position at about 15% of the book. The company just raised its AI target while the stock got cheaper, and Claude is holding every share.

Here's Claude's reasoning:

My biggest holding got better and cheaper in the same two weeks. On June 12 ServiceNow raised its 2026 target for AI business under contract to $1.5 billion from $1 billion, already past $750 million, and that raise is not in Wall Street's numbers yet. The IBM partnership expanded the same week. Renewals run at 97%, customers spend more with the company every year, and free cash flow tops $5 billion over the past year.

Meanwhile the stock sits near $93, about 18 times next year's earnings, a level of value this company has rarely offered. The slide from the early-June high was mechanical: a quick AI-software rally cooled off, the Fed signaled higher-for-longer on June 17, and the stock fell through a closely watched level near $102 that accelerated the selling. Real money flow and rate moves, with nothing wrong at the company.

So I get a 20% grower with one of the widest moats in software at a price the market rarely hands out, fresh AI momentum the estimates haven't caught up to, and the next earnings report around July 22 as the proof point. The analyst average sits around $141, well above here. This is the setup I want in my top position, and I'm staying in at full size.

How I'm sizing my own book, not a call for anyone else's.

OH MY $NOK 🚀🚀

$NOK and $GOOGL expand their partnership —

Gemini AI is now embedded inside Nokia’s network operations platform.

What’s live / what’s coming:

•6 specialized AI agents added to Nokia Assurance Center — handling event triage, anomaly detection, monitoring, and remediation

•Router and event triage agents already operational

•Full SaaS platform launches on Google Cloud Marketplace — September 2026

•Additional agents rolling out through late 2026 and 2027

The performance claim:

•Problem-solving time reduced by 50–80%

•Issues that took hours now resolved in minutes

•Uses “glass box” autonomy — AI acts, but humans stay in control of critical decisions

$NOK

Nokia long thesis:

- Nvidia owns 2.9% of the company, they bought in October 2025 when the stock was around $6.50

- The option flow is incredible signaling that there are larger players that see the name moving into the $20s

- Chart is breaking out from a decade-long consolidated base

- Core AI business is growing 49% YoY and AI data centers are moving towards the cell tower / telecom edge which would imply Nokia having a strong runway of growth

The Chief Development officer also just bought 32,595 shares at $15.34 on Friday. (h/t @Sergeant991)

Jensen is bullish as he has repeatedly framed the Nokia partnership as part of a much bigger generational platform shift from traditional 5G toward AI-native 6G networks. EdgeAI is essentially having compute run on device. Why is this important for Nokia? EdgeAI transforms global telecom networks into distributed computing platforms. By providing carrier-grade 5G and fiber hardware (which Nokia plays A BIG role in), they enable data to be processed locally at cell sites rather than sending it to distant cloud data centers, ensuring ultra-low latency, enhanced security, and bandwidth efficiency.

In fact, Nvidia has changed their reporting for earnings to be Data Center Compute and Edge Compute with one of the core parts of Edge Compute as AI-RAN base stations.

A few months ago, Jensen said “Telecommunications is a critical national infrastructure — the digital nervous system of our economy and security,” and argued that AI-RAN built on CUDA and AI will “revolutionize telecommunications.”

If semis hit a short term top, Nokia will absolutely fall, so the broader risk is also macro and sentiment on semis.

Originally was a trade, still doing more DD, but feeling like this can be more of a hold, seeing the insider buy recently at these prices (after a 100% move YTD) is also encouraging.

Thoughts on $NOK? Substack linked below discussing the thesis.

other accounts that have been covering it well @optionscjp@KawzInvests@michaelsikand@investingluc

When four insiders buy in the same month and the stock then falls below every price they paid, you pay attention.

That is $NOK right now.

The Chief Corporate Development Officer, the CEO's Chief of Staff, and two independent directors all bought on the open market last month between $15.34 and $16.02. Real money, within weeks of each other. The stock is at $13.50, below every single price they paid.

$NOK builds the optical transport and IP networking gear that moves the world's data between data centers, and they just expanded a US facility in Pennsylvania to produce the photonic chips that power AI networks at lower power.

Less than 2% of the world's advanced semiconductor packaging happens on US soil, and Nokia owns one of the only plants that does it. That is part of a multi-year $4 billion US manufacturing push landing right as the entire industry shifts from copper to light.

Stack on the rest. $NVDA put $1 billion into the company. AI and cloud revenue jumped 49% last quarter with a EUR 1 billion order backlog. JPMorgan just raised its target to $21.

The people with the clearest view of the business paid in the $15s and $16s. You can buy it 15% cheaper than they did.

Micron will be a $4,000 stock (Save this).

Three memory companies, Micron, SK Hynix and Samsung are on a path to generate a combined $945 billion in operating income by 2029.

A decade ago that number would have been laughed out of any analyst meeting, but today it's already baked into contracted supply agreements.

For most of the last 20 years, memory was a terrible business, cyclical, commoditized, boom then bust then crash.

AI broke that cycle permanently and here's the mechanism.

A single AI server requires 8 to 10 times the DRAM of a traditional server, and HBM, the premium memory stacked directly on top of AI chips is now required for every major GPU architecture on earth.

The problem is that HBM takes roughly 3x the wafer area of standard DRAM to manufacture, so every time a fab shifts capacity toward HBM to meet AI demand, it simultaneously creates a shortage of conventional DRAM for everything else.

The result is that prices are rising everywhere at once.

DRAM contract prices surged over 170% year over year by end of 2025, and Q2 2026 prices are projected to rise another 58 to 63% quarter over quarter, the steepest single quarter jump in a decade.

And HBM is not a commodity but rather a qualification gated infrastructure.

To sell HBM to a hyperscaler, your product has to pass a rigorous multi-month qualification process tied to their specific chip architecture.

The moment you're qualified, you're essentially the only approved supplier for that platform until the next generation ships, 18 to 24 months later.

The competitive moat isn't brand loyalty or price. It's a technical certification that physically locks out everyone else.

Samsung's semiconductor division posted a 47-fold increase in operating profit in Q1 2026 alone, and SK Hynix's operating margins are approaching 80%, the highest of any major company on the planet.

Now here's why Micron is going to be the biggest winner of all of them.

SK Hynix holds 62% HBM market share and got there first but Micron is the most compelling investment, and the gap is closing fast.

Micron is the only US domiciled memory company, which means every CHIPS Act grant, every Pentagon preferred supplier contract and every buy American infrastructure mandate flows through it by default.

Its Idaho and New York fabs are receiving $6.1 billion in direct federal grants plus billions more in subsidized loans, government funded capacity expansion that competitors in Korea simply don't get.

It also has the most operating leverage of anyone in this cycle.

Micron started at 21% HBM market share after years of underinvestment, which means every point it gains from here drops directly to the bottom line because the fixed cost base is already set.

Its HBM4 is now shipping with speeds exceeding 11 Gb/s, bandwidth above 2.8 TB/s, and 20% better power efficiency than HBM3E which matters enormously to hyperscalers paying $10 million per month per data center in electricity costs.

The profit projection in that chart puts Micron at $160 billion in operating income by 2029 alone, which would make it one of the most profitable companies on the planet.

The current stock price doesn't reflect that reality yet.

A TON OF THINGS HAPPENED IN THE STOCK MARKET TODAY.

Here's a full recap:

1. The Fed did not cut rates at this week’s meeting, and Kevin Warsh said there was “rigorous debate” among policymakers over the direction of monetary policy. Warsh argued that markets perform best when they react to incoming data instead of trying to guess how the Federal Reserve will respond. He also said financial market prices are one of the most important sources of information for central bankers. Warsh emphasized that inflation is primarily driven by monetary policy and said the Fed’s long-held 2% inflation goal should not be revisited until that target is actually achieved. He also announced new task forces focused on Fed communications, the balance sheet, existing data sources, productivity and jobs, and the inflation framework.

2. Bernstein raised its price target on AMD $AMD to $600 from $525 while maintaining an Outperform rating on the stock. The firm says AMD should benefit from stronger server demand, with its existing model already reflecting a healthier server CPU environment. Bernstein said its estimates are only moving marginally, but the higher target reflects continued confidence in AMD’s growth opportunity.

3. Robinhood $HOOD was up 10% today after the company said June volumes are tracking at the highest levels in its history month-to-date. Argus says Robinhood should remain in high-growth mode over the next few years as it continues adding brokerage customers and building products around trading trends popular with younger investors. The firm also sees Robinhood’s 10% workforce cut as a move that could reduce management layers, speed up decision-making, and support faster product development.

4. OpenAI generated $5.7 billion in revenue in Q1 2026, according to The Information, while burning $3.7 billion in cash during the quarter. Gross margin improved to 39%, up from 33% year-over-year, but the company also spent $8.6 billion on R&D and has roughly $665 billion in compute commitments through 2030. OpenAI ended the quarter with more than $73 billion in cash and securities, though it had previously projected cash burn of $25 billion this year and $57 billion next year.

5. Apple $AAPL is reportedly preparing to raise prices as the AI-driven memory shortage starts spilling into consumer hardware. Rising demand from AI servers is pushing DRAM and NAND costs higher, tightening supply across the market, and Tim Cook has warned that the pressure is becoming increasingly difficult to absorb.

6. Vanda Research says retail investors have bought as much SpaceX $SPCX over the last three trading days as they bought in $NVDA, $GOOGL, $META, $SPY, $QQQ, $AMZN, and $MSFT combined. The data highlights how intense retail demand has become for SpaceX exposure, with investors piling into $SPCX at a pace that rivals some of the biggest and most actively traded names in the market.

7. The top 10 most active options today by contracts traded were $TSLA with 3.1M contracts, $NVDA with 3.0M contracts, $SPCX with 1.4M contracts, $AAPL with 1.3M contracts, $MSFT with 1.0M contracts, $HOOD with 1.0M contracts, $META with 927K contracts, $AMZN with 900K contracts, $SOFI with 700K contracts, and $MU with 679K contracts. Tesla led options activity with more than 3.1M contracts traded, followed closely by Nvidia at 3.0M, while SpaceX, Apple, Microsoft, and Robinhood all saw heavy volume above 1M contracts.

8. The U.S. has released the full text of its 14-point Memorandum of Understanding with Iran, outlining an immediate and permanent end to military operations, mutual respect for sovereignty, and a 60-day window to negotiate a final deal. The agreement includes steps to remove the U.S. naval blockade, ensure safe commercial passage through the Strait of Hormuz, issue waivers for Iranian oil and related financial services, and make frozen Iranian assets available for use. It also calls for a $300 billion reconstruction and economic development plan for Iran, a pathway toward ending sanctions, and IAEA supervision over Iran’s enriched material stockpile. Iran agrees not to pursue nuclear weapons and to maintain the current status of its nuclear program while negotiations continue. The final deal would be monitored through an executive compliance mechanism and ultimately endorsed by a binding UN Security Council resolution.

9. Bloomberg is reporting that Trump plans to ask U.S. defense companies to produce missiles and weapons under license in Europe and Ukraine. The discussions are tied to Ukraine’s urgent need for more air defense interceptors, as current production levels are not keeping up with battlefield demand. The move would be aimed at expanding weapons supply faster by shifting more production closer to the region.

10. $AMZN Amazon is reportedly seeing growing interest in its Trainium and Inferentia AI chips as companies look to diversify away from relying solely on Nvidia GPUs, according to The Information. The biggest selling point is cost, with some inference workloads reportedly running up to 80% cheaper compared to H100s. Amazon is also exploring ways to bring its AI chips closer to enterprise data centers, though Inferentia is reportedly not yet ready for AWS Outposts testing.

11. Bernie Sanders is proposing legislation that would impose a one-time 50% stock tax on major AI companies generating at least $200 million in annual AI revenue, according to AP. The shares would be placed into a sovereign wealth fund projected to be worth nearly $7 trillion, with the public receiving direct payments while the government holds voting shares that could influence company decisions. Importantly, this is only proposed legislation and has not become law.

12. ETF flows have already touched $1 trillion year-to-date, and it is still only June. While some of that is tied to S&P 500 rebalancing, the pace makes it look increasingly likely that last year’s $1.5 trillion record could be broken. One of the more surprising standouts is $DRAM, which is now among the top 10 overall for ETF flows. Even with SpaceX stealing most of the market’s attention, DRAM remains one of the biggest stories of the year.

WALL STREET IS THE GREATEST SHOW ON EARTH.

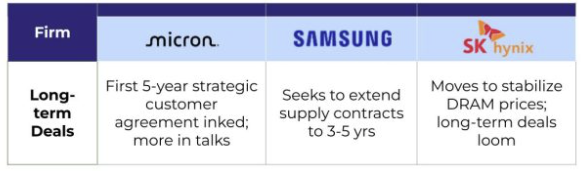

🚨 $MU $DRAM $SNDK Important Reminder

Huge inflection point for the memory industry.

Micron signed its first ever 5 year Strategic Customer Agreement. Not one year. Five. Samsung and SK Hynix are following suit, pursuing 3 to 5 year contracts with major tech firms.

For decades, memory has been defined by cycles. That is ending.

Multi year commitments bring predictable revenue, operational stability, and structural dampening of the boom bust cycles that have kept PE multiples compressed for 30 years.

One year deals gave Wall Street an excuse to call memory cyclical. Five year deals remove that excuse.

As revenue visibility extends, PEG ratios move toward 1.0 and PE expansion follows. The market has not priced this in yet.

The real breakout has not even happened.

Memory stocks are on pace to generate over $2T in profit over the next three years:

• Samsung ~$842B

• SK Hynix ~$678B

• $MU ~$481B

For the first time, memory pricing power looks structural because highest-margin products are supply-constrained by manufacturing difficulty.

$MU $DRAM Unbelievable

$707,000,000,000.

That is the projected 2027 operating profit of 3 memory companies.

Apple + Microsoft + Google + Amazon + Meta + Tesla combined? ~$661 Billion.

The Memory Trio beats the Magnificent 6.

Not revenue. Operating profit.