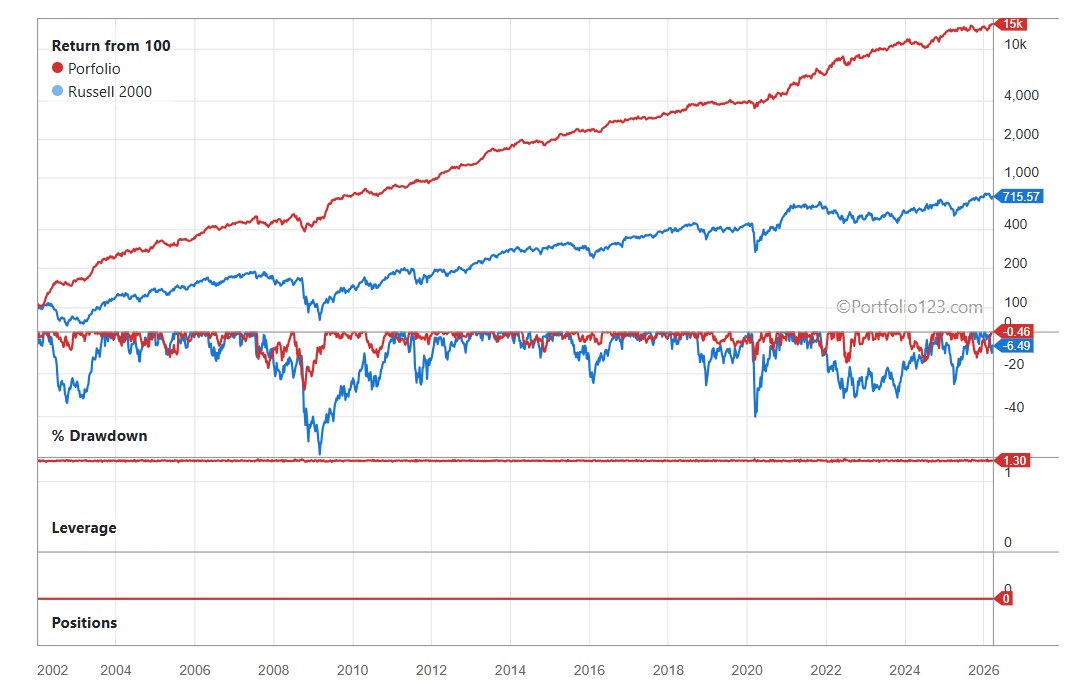

Two years ago, I built a simple system based on just 7 factors.

Since then, it’s been consistently outperforming.

Backtests show it has outperformed every single year since 2002 — except 2019.

I wrote a free e-book explaining the system.

You can use it yourself. No paywall.

People call it factor investing. I think of it as automated due diligence.

Think about what happens in a typical M&A process. You look at stability in returns on capital, trends in working capital, how operating cash flow relates to the gap between capex and depreciation. You stress-test earnings quality, check whether margins are sustainable, whether the business is actually converting profits into cash. The list goes on and on.

A well-designed systematic process does the same thing — across a thousand stocks at once. But sometimes a financial due diligence isn't enough. Especially on the short side.

Some companies indeed have terrible fundamentals — but a CEO convincing the world he built a hydrogen truck when it was gravity doing the work, or one who turns every earnings call into a Bitcoin sermon — and the stock goes up 80% anyway. You can blame the CEO for that, or the ignorance of the average investor, but that won't solve your problem. It's your responsibility to come up with a judgment about companies that works — and a financial due diligence alone won't always get you there.

This is where a human eye makes the difference. Not all bad companies are equal. The ones with a cult following are dangerous to short — no matter how bad the fundamentals. The ones quietly deteriorating, with no story to prop them up, are where you want to be.

I do this on the short side of one of my own strategies. The systematic layer handles the broad ranking. The human layer filters for the kind of risk that numbers alone don't capture. It works — but it's the part that limits your scale.

And that's what makes this moment to be alive so interesting. With the latest AI tools, that trained human eye can now be incorporated into your systems — and potentially even tested with hypotheses. The judgment that used to be purely manual becomes something you can scale.

The line between systematic and fundamental investing is blurring. I think the investors who do best will be the ones who stop treating them as separate disciplines.

When do you rank stocks against country or regional peers?

When the factor has structural country-level differences.

Corporate tax rates vary 10-35% across countries, so any earnings-based factor (E/P, ROE) gets distorted in a global rank. Country-bucketing cleans that up.

You've heard about ranking companies versus their sector and industry peers.

What about ranking against their marketcap peers? What about their country peers?

Results for FCF TTM over assets below.

When I was a child, I used to play soccer at the local soccer club. I have a lot of memories from that time. Some built up over time — the smell of wet grass in the morning, the wind through the trees, the sweaty shin guards, the smelly shoes. The talks amongst the older guys that I usually just observed from a distance. The look of my father, the other parents on the side of the field. I remember those very vividly still.

Other memories are more point in time, and feel like core memories now. At the time, I didn't think much of it — at least not in any analytical way — but its importance did strike me, even then.

There was this one kid on my team who wasn't the most popular guy within the team. One day, the team was brought together, because apparently a teammember had called the coach and mentioned he was considering leaving, because of the way he felt he was being treated by the others. We were sitting together in one of the locker rooms that, in terms of size, could barely accommodate the team, the coach and some of the parents. It was obvious who we were talking about, but his name was left out.

His parents wouldn't let him play in international tournaments, because they considered those too expensive. That hadn't helped the group dynamics. On top of that, comments had been made about the way he looked out of his eyes during the practice that Wednesday before, that some considered beady. The fact that he wasn't the most intellectually talented kid — he went to a school that was low on the academic scale relative to the team members of that small soccer club — also didn't help in terms of image. He was quite tall and a bit clumsy from the look of it, and even though he had a great through pass, it didn't look aesthetically pleasing from a distance. His girlfriend wasn't considered pretty. The scooter he drove to practice was too small for his size. For what it is worth, he was left footed.

I remember the words said by the coach, the elderly and the most vocal teammembers in the locker room. The red paint on the window frame and door, both blattering off. The half-open black bags with the white letters of the team's sponsor on them. The body language of the team members — a mix of some empathy and small signs of judgement, people wanting to keep their social position intact. I remember turning inward, the voices turning blurry.

I remember feeling I wasn't quite like the average teammember either. In some respects my image was the opposite. My father drove a rather fancy car. When asked if I was taught French or German in school, I felt I had to mention I was being taught Latin too. My parents drank red wine, not beer. I ate an apple after the matches, not fries. I didn't know all the different types of sauces you put on the fries, which seemed common language to the others. I was more of a technical player, not physically big or strong, at least compared to my soccer team peers.

I don't remember the closing comments in that small locker room that evening. What I do remember is that he kept playing on the team. And I'm glad he did.

When we played on the same team in training, we would often win. I wouldn't be able to explain to you what made it work, but it did. Call it complementary. We had no common ground. Not much to talk about either. But on the field something clicked — a through pass arriving exactly where I was already moving, a run I didn't have to call for. And in all honesty, those wins felt much more rewarding than other wins.

What stays with me is that all those social judgements within the group didn't matter when it came to getting into a flow. Barely any common ground, no shared language — and somehow the thing flows, the win comes, and nobody is trying to be anyone. No posturing, no judgement. And in the absence of all that, the differences stop being a problem and start being the point. I haven't felt that in a while. I'd like to again.

Stocks listed in a weakening currency, outperform.

That means: investing in Turkey, Poland, Sweden.

The more weakening the currency, the better.

Unhedged that is.

Crazy, right?

Over the past several months, I identified what I believe to be a previously undiscovered meta-factor.

I'm not publishing this one yet.

But the factor and research process that led me to finding it, will be in my book.

For now, the intro E-book is already up for grabs. Free.

For professional clients, I'm always hunting for an edge.

One I like: a factor that tracks how consistently companies return capital.

It sums consecutive years of:

• Buybacks

• Dividend increases

• Debt reductions

Additions to the factors in the free e-book. No paywall.

I built this model about 3 years ago.

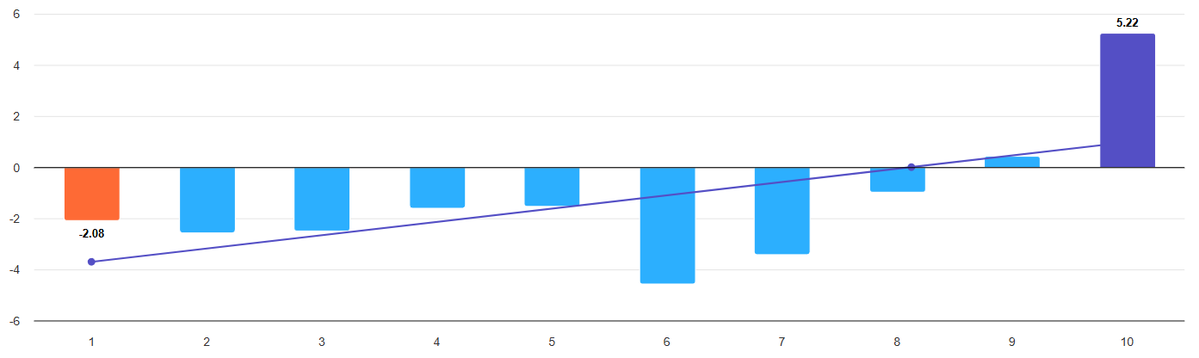

Since then, it's EXCESS return vs the Russell 2000 were:

2023: +5.4%

2024: +8.2%

2025: +11.6%

2026 YTD: +8.2%

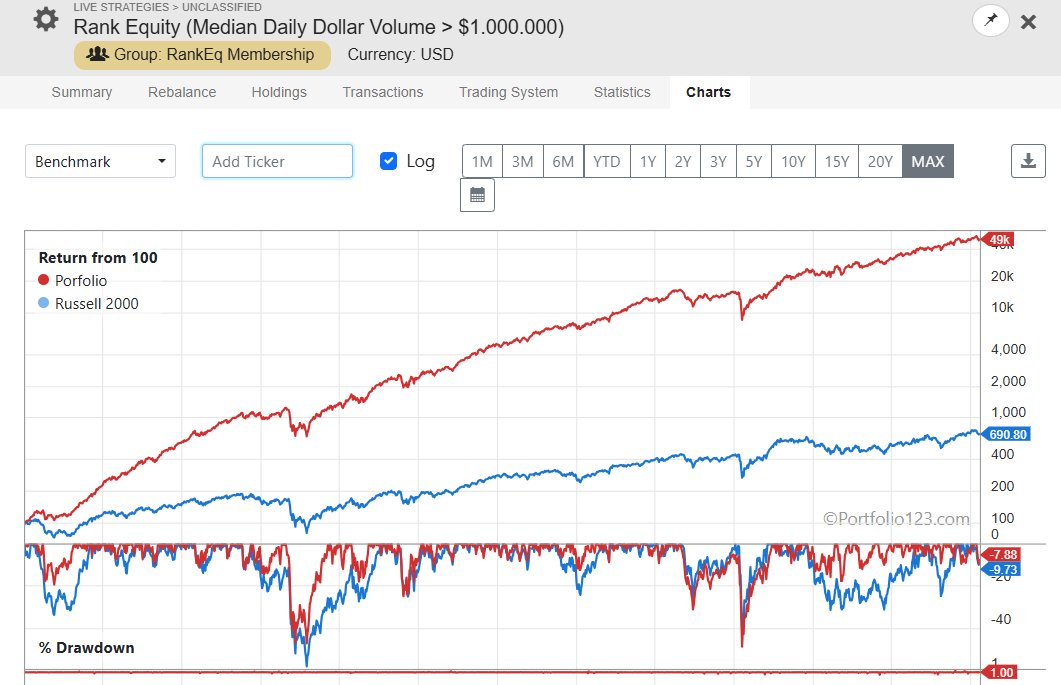

30 stocks. $500k+ median daily dollar volume.

At 5% participation, 500% turnover, roughly 38M max AUM.

Available to members.

@RankEquity I finally understand factor investing thanks to your ebook. Amazing work really. will be in line to buy the full book whenever you publish it. Great work

@nymfree Hi X.M., it is a comment like yours that I really do it all for. So thank you very much for taking the time to write it. It also gives me more enthusiasm to keep on writing the full book. Thanks again and all the best.

A subscriber wanted to link one of my example portfolios with their broker.

So I offered it.

10 minutes to set up. $1M+ median dollar volume — liquidity is no issue here.

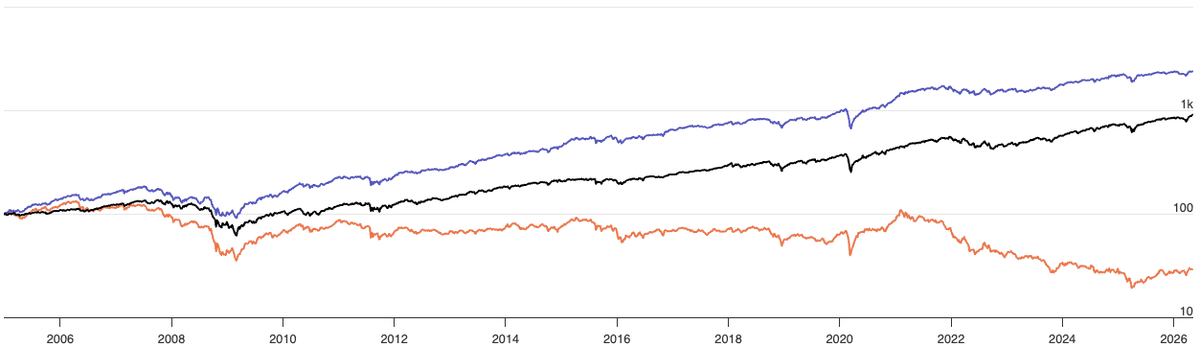

Outperforming every year since 2002, except 2020.

Another happy member.

Two years ago, I built a simple system based on just 7 factors.

Since then, it’s been consistently outperforming.

Backtests show it has outperformed every single year since 2002 — except 2019.

I wrote a free e-book explaining the system.

You can use it yourself. No paywall.

@WolfhartInvest Personally, knowing it is long only - I would have conviction in the system. But each their own, of course.

Levering up to 1.3x and taking a 30% position in TZA (very naïve hedge) would have resulted in a 30% max drawdown with 23% annualized and a beta of 0. Backtested, that is.