Tata Capital looks like a strong buy with a longterm lens

1.Trades at 2.8x Book with solid guidance

2.FY26 numbers showing strong sequential execution

3.Strong Tata Brand

There's a chance of both 30% PAT CAGR & rerating happening which is rare to find in Largecaps

Disc- Invested

Dr Agarwals Health Care Ltd has been consistently putting out 20% revenue and EBITDA growth each quarter.

Currently trades at TTM 25x EBITDA & 29x FCF with only 1.87% of shareholding in retailers hands.

Such high quality + growth + low float stocks are a rare find 🙃

Agarwals Health Care going strong with expansions plans.

- 54 new hospitals/ clinics to be added this FY up from current 249 facilities

- Revenue growing at +20% with operating leverage pushing EBITDA even higher

Entry into various new markets like Delhi, Punjab, UP in the north will create large markets as they have proven in different states in South.

I like the way management is building a brand and growing aggressively to capture this market. Market doesn't yet fully understand there model.

Disc- Invested & biased

Added a new position today #Brainbees

FIRSTCRY

1. Had been the victim of high valuations after IPO and fell 65% from ATHs as market mood worsened.

2. Showing strong recovery now with very good volumes.

3. Fundamentally the company is moving in the right direction with improving margins & Cash PAT.

4. On the revenue front the business grew 18% on consolidated level, which according to the massive TAM and growth opportunities present, is a bit on the lower end.

5. The management is of grade A quality and can steer the currently cash burning part of International channels to profitability over the next 2-3 years.

6. It is difficult to value such new age companies but, currently it has a Cash PAT of 209cr which'll put it at about 103x this metric. Cash PAT has been growing at really high 80-90% YoY.

For me it is a bet on revenue growth coming back to 22-25% range + margins expansions + international business becoming breakeven.

My E-Commerce bet now has 4 names Nykaa, Delhivery, Shopify & Firstcry through which I'll ride the massive consumption boost.

Good jump of 29% in Q4 revenue numbers for HESTER with operating leverage playing out beautifully.

FY 25 EPS 32.31

FY 26 EPS 66.08

2x in EPS with just 7% revenue growth shows what could play out when we see capacity utilization going up.

A solid play for me at TTM PE of 27.8x

This smallcap vaccine maker might be entering its turnaround phase 🧬💥

Added Hester Biosciences to my portfolio today.

Here’s why this smallcap looks interesting after Q2FY26 results 👇

🔹 About the business

Hester Biosciences operates in 2 key segments — Poultry Healthcare & Animal Healthcare.

• Poultry segment grew 18% YoY, driven by better vaccine volumes.

• Just got approval for the H9N2 Avian Influenza vaccine, with production starting Q3 and export oriented orders.

• Animal segment fell ~50% due to delay in govt immunisation programs (PPR & Lumpy Skin). Mgmt expects recovery in H2.

• 3 plants across Mehsana, Nepal & Africa — currently running at just ~20% of toal capacity.

🔹 Growth Triggers I’m betting on

1️⃣ Business shift: Management consciously moving away from govt contracts → towards private & export orders = lesser lumpiness + better margins.

2️⃣ Huge operating leverage: Only 20% capacity utilisation means any demand uptick can significantly boost profits.

3️⃣ Pet care opportunity: Planning entry into the fast-growing pet vaccine market (esp. rabies). Expect partnerships with global players to bring tech + manufacturing to India.

4️⃣ Margin story: Despite a 7% revenue decline in H1FY26, margins improved to 32% (vs 25%) — shows pricing power & strong moat.

At 22x FY26E EPS, with capex already done and growth triggers lined up, this looks like one of those setups where the market has priced in all the negatives (govt dependency, Africa slowdown, no growth)…

…and when the tide turns — these names move fast 🚀

Low float, operating leverage, shifting mix —

this one could surprise on the upside 💡

#HesterBio #Smallcap #Investing

Great start to Q4 results by Tips Music

Management walking there guidance with strong performance in H2.

PAT up 30% & Revenue up 21% for FY26

At current valuations it trades at about 30x FY27 EPS which is quite reasonable for a high growth clean management business.

We’re spending $200B+ a year on data centers to power AI. One company raised $11M, grew human brain cells on a chip, and the cells taught themselves to play a 3D shooter in a week.

Cortical Labs grew 200,000 human neurons on a silicon chip and taught them to play Doom. The cells navigate, target enemies, and fire weapons in real time. Their previous game, Pong, took 18 months on older hardware. Doom took a week. An independent developer with zero biotech experience built the integration using a Python API. The neurons did the rest.

That compression from 18 months to one week tells you everything about where this is going.

Here’s what the “can it run Doom” crowd is missing: each CL1 unit costs $35,000. A full 30-unit server rack draws 850 to 1,000 watts total. Your brain runs on 20 watts. A single GPU cluster training an LLM can draw megawatts. The energy economics of biological compute are orders of magnitude better than silicon, and that gap scales.

The investor list tells you who’s paying attention. Horizons Ventures, Blackbird, and In-Q-Tel, the CIA’s venture arm. In-Q-Tel doesn’t fund science projects. They fund intelligence infrastructure. 115 units started shipping in 2025.

Cortical Labs is now selling “Wetware-as-a-Service” through the Cortical Cloud. Developers can deploy code to living neurons remotely without touching a lab. They’re pricing access at the level of a software subscription while the hardware runs on real human brain cells derived from adult skin and blood samples.

The Doom demo is marketing. The platform play is a bet that biological neurons will eventually outperform silicon at exactly the tasks AI struggles with most: real-time adaptation under uncertainty, learning from minimal data, and processing ambiguity without brute-force compute.

The question was never “can it run Doom.” The question is what happens when it can run everything else.

▶️Entero Healthcare now trades at 25x FY27 EPS

▶️Organic LFL revenue growth pace expanded to 17%

▶️ 9m revenue up 25% YoY with EPS growing 40%+

▶️ Improving working capital days & +ve operating cash flow

The company threw out a perfect Q3FY26 in a high growth runway sector but markets are busy selling it off with the other smallcaps 🙃

I guess it gives me time to load up some more

Disc- Invested

Hence the strong technical & performance of Polycab 🫡

It has just been a year since Investors called doomsday when Grasim announced wire capacity and it's almost up 2x from there.

Disc- Invested & biased

Each 1 GW of data centre capacity requires ₹3,500-4,000 crore in cabling.

8-10 GW of additional data centres capacity can generate demand worth 28-35k crores worth of demand for Cables by FY30-31 in India

Tough time to be a long term investor

Markets are beating up a new portfolio stock everyday. Even good flow of news or low valuations isn't stopping the selling in many names.

I can feel that recovery is just around the corner & is inevitable, but the "waiting" part is the hardest.

Paramount just bought a $111 billion media empire with a $12 billion market cap.

Read that again. Paramount’s market cap is roughly $12 billion. Warner Bros. Discovery’s enterprise value in this deal is $111 billion. David Ellison is buying a company nearly 10x his own company’s size.

How? Larry Ellison’s net worth: $201 billion. He’s personally guaranteeing the equity commitment. Bank of America, Citi, and Apollo are providing $57.5 billion in debt financing. Saudi Arabia’s Public Investment Fund, Abu Dhabi’s L’imad Holdings, and the Qatar Investment Authority are providing equity. The combined entity will carry over $90 billion in debt.

This tells you everything about what actually happened. Netflix offered $83 billion for the studios and streaming (the good parts). Paramount offered $111 billion for everything (including the dying cable networks nobody else wanted). Netflix looked at the math to match Paramount and said “at this price, the deal is no longer financially attractive.” That’s Netflix-speak for “we’re not overpaying for linear TV in 2026.”

Netflix stock jumped 10% on the news it lost. Paramount rose 5%. The market is telling you which company made the better decision.

What makes this really interesting: Paramount promised $6 billion in cost synergies. That’s code for mass layoffs across two studios, two streaming platforms, and overlapping cable networks. CNN and CBS News under one roof. HBO Max and Paramount+ merged. They’ll need those savings because the debt service on $90 billion will be brutal.

David Ellison attended Trump’s State of the Union as Lindsey Graham’s guest on Tuesday. Ted Sarandos was at the White House Thursday afternoon. Both were lobbying. Ellison won. And his father’s close ties to Trump will matter when DOJ reviews a deal that puts CBS, CNN, HBO, Nickelodeon, Comedy Central, MTV, and TNT under one owner.

The real story: a 42-year-old with a rocky box office track record just assembled the largest media conglomerate in history, financed by his father’s fortune, Middle Eastern sovereign wealth, and $57.5 billion in bank debt. Netflix walked away richer. The question is whether Paramount can service the debt load while linear TV revenue keeps declining or whether this becomes the most expensive content library acquisition ever assembled on borrowed time.

We featured Entero Healthcare in Growth Titans Q1 and Q2.

The stock went down 40% for a year.

Then Q3 numbers dropped.

The roll-up is finally inflecting, and the market hasn't caught on yet.

A thread on what just changed 🧵

@vaibhav2ghadge Even if we take 0 value for international business the leftover business is being valued dirt cheap. They even have 1000cr+ of cash on books to build there new qwik and rocketbees segment.

International business for me is just an optionality that could play out.

Doubled my position in Firstcry today

It doesn't look like a business that is dying with the way the stock price has been performing.

Most of the so called financial gurus have been advocating the fall on losses, but one look under the hood and we can see the massive 240crs of CASH that the business has already generated in the past 9months.

Even on CASH multiples it trades at a modest 35x for an e-commerce multi year play with A grade management.

If we are to take only the India business into account and skip all the other verticals it now trades at 22x EBITDA.

For me E-commerce & consumption are long term bets and such pessimistic environment are large opportunities to add.

Nykaa breaking out today backed by great Q3FY26 results

The topline growth has been increasing for 3-4 quarters now, with margin expansion also kicking in now.

Looks like a good place to be in 😇

Disc- Invested & biased

Continued strong performance by Dr. Agarwals Healthcare in Q3FY26

20%+ growth in topline & 74%+ growth in EPS

This remains one of the least retail owned and talked about healthcare stock in our markets even after continuous strong performance by the promoters

Disc- Invested & biased

Buried inside 800+ pages of the Economic Survey is a stark warning:

India is staring at BIG global risks in 2026.

In the worst-case scenario, the situation could be more brutal than the 2008 Global Financial Crisis.

Let’s break it down 🧵

Continued good times for #Lauruslabs Q3FY26

Strong revenue growth of 26% & PAT growth of crazy of 176%

Ebitda margins at 27.3%

Cash flow to EBITDA @ 113%

Reducing debt and all segments firing

What more do you need from a portfolio company ? 💪

Disc- Invested

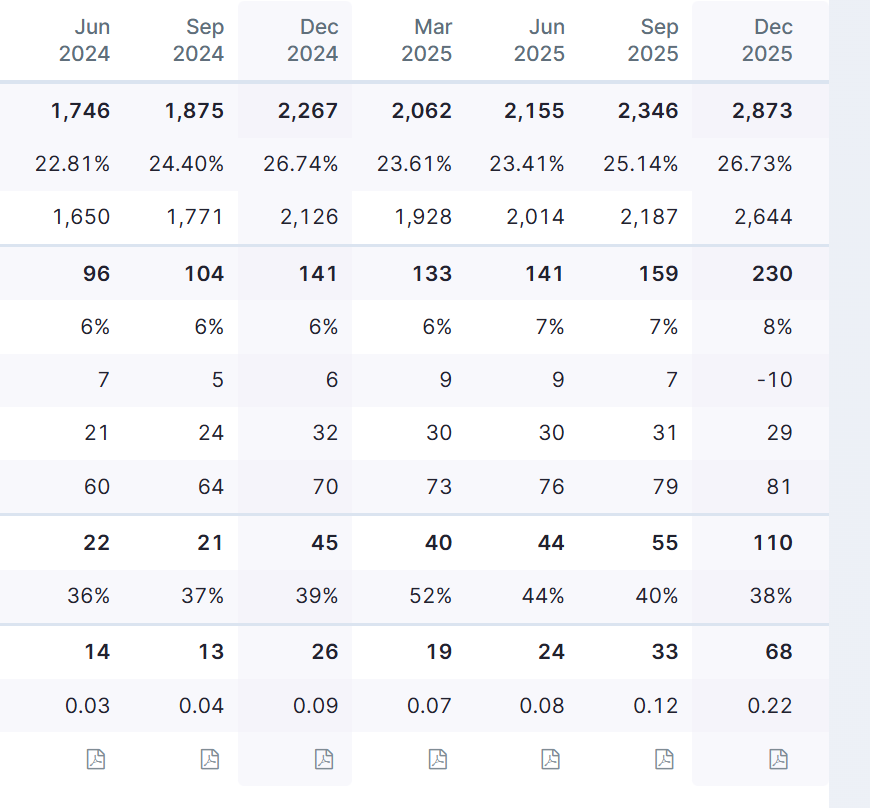

Good results for #Eternal Q3FY26

- Quick commerce became Adj. Ebitda profitable for the first time paving and showing the markets that this model is financially viable. Management is confident of achieving 5-6% margins in long term & don't see any ceiling for topline for now.

- Delhi NCR has a 3.5% margin & growing at 55% whereas the next 10 cities are growing at 100%+ but still account for combined 1.5x size of Delhi. It shows the long runway of growth pending in quick commerce.

- Food delivery remains stable with growth in there guided 16% mark and margins healthy at 5.4%

- District showed deep losses of -121cr due to heavy burn done to promote the new District Pass. Judging by the hype they created for there app on social media in the past month it seems to have worked. How they'll monetize it in future and consumer stickiness remains a "?" for now.

It feels like a perfect time for Deepinder to step down from the CEO position and pass on this baton to Albinder. He has proved that the models are profitable at scale with even quick commerce becoming breakeven which is quite positive for it's peers as well.

Finally the tables seem to be turning for RBA after 6 long years.

New promoters should bring much required fresh approach & liquidity in the form of 1500crs by way of issuance of fresh equity and warrants.

Valuations and Burger King brand remains strong and it is only the profitability metrics that need to be worked on.

This one remains in watchlist for now due to no liquidity, but is a strong turnaround contender.

Restaurant Brand Asia #RBA raises 500cr via QIP to reduce debt and expand store count.

1. Stock price has been constantly on the down hill since IPO in 2020. Has fallen from 160 to 65 now in 5 years.

2. In these 5 years Burger King has constantly diluted equity to reduce debt by raising 1400cr first and 500cr now. Additionally promoters also dumped there stake and reduced holding by 27%

3. Indonesia business acquisiton when India business was itself capex heavy also changed market sentiment.

4. On the brand front Burger King has been doing fine and revenue growth has been as per industry standards. Margins for India business have been on the uphill but Indonesia has been loss making.

It's a counter I'll track as valuations are attractive. If market sentiment changes on this one due to consumption growth in H2 it could be good place to be in.