$CHTR about to break $200. Round trip since Spring 2016. No dividends but over $75B of share buybacks.

Current Market Cap $30B

Black mark for Dr. Malone and Rutledge.

Rutledge got out at the right time.

@MarioGabelli and sub $20 last week, around $16 in October.

question: are you okay with Malone saying the Braves won't be sold in Ted Turner's lifetime?

For someone who often says everything is for sale - he seems pretty intent on keeping this around for a while.

@CapitalFang very aggressive buybacks in the 3rd quarter as well.

3mm shares in buybacks is almost 20% of shares outstanding.

this is a smart move - in my opinion - if they believe the trends can stay okay.

@DismAssetBkd lots of risks (obviously) - 1) industry doesn't rationalize and downcycle takes 5 years 2) instead of switching/closing their weakest plant SW sells a plant to Suzano. 3) Europe imports are price insensitive 4) CEO likes his $6mm a year job, refuses buyout offer. plenty more.

a LT chart of $CLW is a sad chart.

so much capital destroyed over the years. Across the board - in cap ex, in mergers, divestitures.

stock cut in half over the last decade. negative returns over the last 15 years.

they are the patsy at the table.

fyi - i own the stock.

$CLW is extremely attractive here IMHO. It feels like a 5/1 upside downside trade - at 17.50 - upside to 35, downside to 14. (14 is roughly 2x mid cycle ebitda).

the market/sell side has the SBS glut continuing for several years. I think that is wrong assumption.

$CLW - another really bad quarter.

the Augusta acquisition is turning into a disaster for a variety of reasons.

The board should be ashamed of themselves for the pay package they give the executives.

@Nate93658762@DadInvest the recent sell was bad look. same with CFO sale in May. The stock has leaked down since then recent sale.

Fair value now or in a sale?

in a sale, it's hard to see this going for less than $60 - which leads me to believe it's not happening anytime soon. unfortunately.

@Nate93658762@DadInvest Insiders don't see a sale, they been exercise and selling options for a while now.

It would clearly sell for a significant premium but i do get the sense they want to wait they can get a much higher revenue multiple - which would need a owner friendly labor deal.

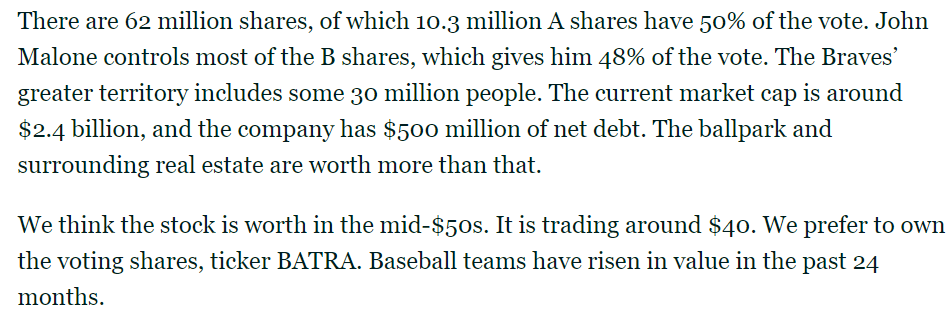

$BATRK $BATRA

Ever since pounding the table at the analyst day in june on the value of the battery and the team - management has been dumping shares via exercise of options. That are not expiring for 2 years.

It's compelling at $40 if you think there is a sale in 3 years.

@MarioGabelli Mid 50s for the $Batra (Braves) is significantly below fair value. I think in a sale it would be at least $60 - which is approximately $3B for the team and $1.2B for RE.

That being said the CFO selling shares might add credibility to your mid 50s value.

thoughts?

Mag 7 index since early 2015 versus the performance of the Bloomberg 500 Ex Mag 7 index Amazingly the Mag 7 index is up 2,800% versus a gain of just 129% for the Ex Mag 7. Essentially all of the market’s huge gain over the last ten years has come from the Mag 7.

$CLW - In boxboard, RISI reported that pricing remained unchanged from July. In SBS, fewer competing European FBB imports appear to be providing pricing support, though orders may be slower given overall tariff uncertainty. Early but positive S/D news.

Great outcome for $GBIO

This was a net-net biopharma with mostly pre-clinical assets trading at a massive discount to net cash. The bet was on the company announcing a strategic review of its remaining assets or a potential liquidation.

This has just occurred, and the stock has popped 65%+ since the post.

The company announced a 90% workforce reduction, the settlement of a large portion of its lease liability at a decent discount, and the intention to sell its early-stage assets.

By my estimates, the discount to net cash at this point is limited — around $60M as of mid-August versus a market cap of $45M. This does not account for severance costs, wind-down expenses, and continued cash burn until the final resolution. For reference, just the severance could cost the company anywhere from $6–10M, fully eliminating any upside from current levels. Given that most of the company’s assets are pre-clinical, their sale is unlikely to result in meaningful value that would change the dynamics here, so upside from current levels is limited.

Generally, betting on highly discounted pharmas with pre-clinical assets and high insider ownership (22% here) in a basket is a decent way to continue playing the busted biopharma space, with a bet on similar announcements.