I’m calling this shift now. The new memetics around Ripple/XRP. Ripple news and tech is the proxy for crypto adoption in the global banking industry. Goodbye SWIFT replacement narrative, hello full banking payment “inside/outside” tech stack transition.

$XRP #ripple

While a little buried (in WSJ print edition), the latest CPI data shows a 3.5% reduction in financial services costs for consumers… dare I say that this could be in part because of the Administration’s pro-crypto policies? https://t.co/2l9WHwvAhj

The banks are PISSING THEMSELVES.

They’ve just realized that some autistic crypto startup in a WeWork with $20 million in T‑Bills and a React front-end is about to nuke the entire $17 trillion U.S. deposit base…

…by offering 4.9% yield on a stablecoin while JPMorgan gives you 0.01% and a debit card that expires in two years.

“BUT THAT’S NOT FAIR” – every bank lobbyist ever

Now the banking system, this Godzilla made of soy, duct tape, and 11,000 physical branches, is whining to Congress like:

“This isn’t fair! If people can earn yield on dollars outside the bank… they might leave the bank!”

No shit. That’s the point. You locked everyone into a zero‑yield Ponzi for a decade while printing $7 trillion, and now you’re shocked people want out?

What’s next, are you gonna sue water for being wet?

This is a regulatory street fight between code and bureaucracy, between global liquidity that settles in five seconds and the rotting husk of Bretton Woods wearing a suit made of FDIC pamphlets.

And guess what?

The White House is hosting peace talks.

Yes.

Trump’s team just invited Circle and Coinbase to sit down with Jamie Dimon and tell him that the future of dollars may not involve Jamie Dimon.

Can you imagine the mood in that meeting?

“Hi Jamie, meet Brian from Circle. He tokenizes T-Bills with six engineers and a Discord server. He’s taking 3% of your deposits and none of your regulatory costs. Thoughts?”

The reality is that every time one of these banks says “we’re concerned about financial stability,” what they mean is:

“Please don’t let these crypto goblins disrupt our ability to harvest yield off the lower-middle class with 18% credit cards and 0% checking accounts.”

They want protection rackets codified into law.

Like “you can’t offer yield on stablecoins unless you’re a licensed bank,”

aka:

“We missed the boat, so let’s blow up the dock.”

Banks can’t compete.

Let’s model it:

A bank: 11,000 branches, 75,000 tellers, legacy core systems from 1982, and a CFO who thinks Solana is a fish.

Circle: 25 people, 100% T-Bill backing, 24/7 redemptions, yield streamed on-chain like Netflix.

Now let me make this brutally simple... Who wins?

The guys with marble lobbies or the protocol that turns dollars into yield-bearing bearer assets?

The banks are playing defense against stablecoin yield... but what happens when it clicks that stablecoins are just a transition vector to full monetary exit?

What happens when people use stablecoins to bootstrap into Bitcoin treasuries with self-custody?

You go from “5% yield off Circle’s T-Bill stack” to “30% CAGR in purchasing power in a bearer asset that can’t be diluted and lives outside the IMF death loop.”

That’s endgame stuff.

The banks are scared of USDC + USDT.

Wait until every mom in Omaha is yield farming STRC dividends from their Roth IRAs using a Lightning app.

We’re replacing the entire fiat architecture with a monetary black hole.

https://t.co/FgXOFs2ikL

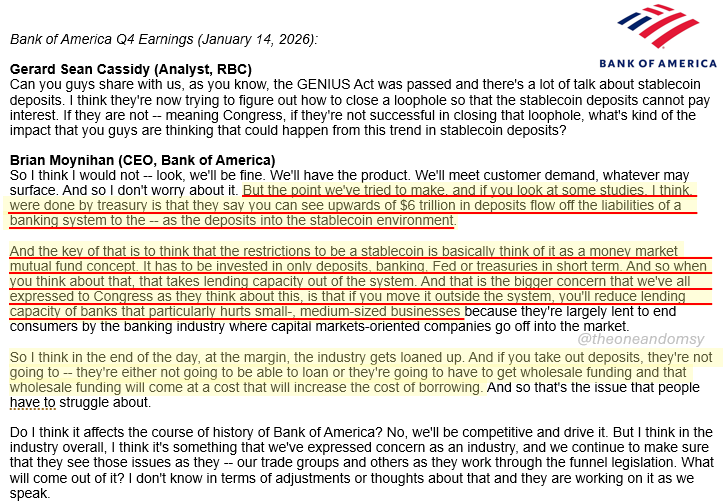

Bank of America CEO on why stablecoins shouldn't pay interest:

(TLDR: consumers shouldn't earn yield so banks can)

Quick summary:

Interest on stables -> mass deposit flight

Fully reserved money -> no fractional leverage

Banks lose free funding -> profits go bye bye!

https://t.co/ftARbdGVAv

It’s “banks vs on chain finance”. Watching this legislative battle around what the Clarity Act is trying to do in the final few drafts is fascinating.

#realtimerails#Coinbase#DigitalAssets#defi

Coinbase pushing back didn’t surprise me.

What did stand out was Armstrong saying the quiet part out loud: banks don’t want competition.

If banks can lend, but crypto firms can’t, that’s not regulation - that’s protection.

Today’s Senate meetings matter because this has stopped being “crypto vs regulators.”

It’s banks vs onchain finance.

And whoever wins decides who gets to offer financial products next cycle.

Ripple is at Davos. For a financial and digital asset conversation it started many years ago. And now leads and teaches. The transformation continues. #Ripple#Davos2026#DigitalAssets#XRP

Happening Tomorrow in St. Moritz

Title: Oil and Water?

Are Crypto Companies Compatible With Traditional Public Markets?

Crypto M&A reached some of its highest levels in 2025 (130+ deals), with no signs of slowing down, as others take traditional capital market paths such as IPOs. A new paradigm is emerging as crypto matures with different pathways and hurdles facing acquirers, investors and those wanting to be acquired or go public. With respect to token issuance and public market listings, is it “either/or”, or “both/and”?

"Blockchain is going to be the infrastructure of financial services. There is no question in my mind on that."

@FTI_Global CEO Jenny Johnson

@cfcstmoritz | @AlgoFoundation | @StaciW_DC