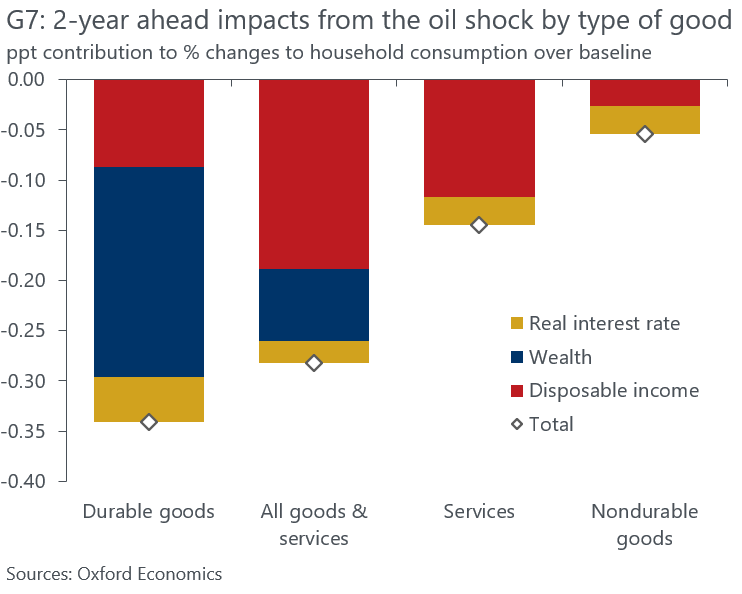

In our latest research note, Global Chief Economist Ryan Sweet (@RealTime_Econ) and I explored the repercussions of oil price shocks on G7 consumer spending and find visible negative impacts that can linger up to two years after the initial hit. What's interesting is how uneven these impacts are felt across different types of goods.

Durable goods, which are often perceived to be more responsive to economic cycles, are largely so because of its large exposure to wealth effects. During oil shocks, higher inflation and interest rates tend to erode the purchasing power of the present value of wealth.

In our research, we also explore additional downside risks coming from the further escalation of the Middle East conflict and how they affect each member of the G7. Find out more here: https://t.co/FWlYgHHuvA

This isn't good: "BLS is reducing sample in areas across the country. In April, BLS suspended CPI data collection entirely in Lincoln, NE, and Provo, UT. In June, BLS suspended collection entirely in Buffalo, NY."

https://t.co/yZIbZKtziu

Former NY Fed President Bill Dudley lays out why the Fed should KEEP the 2% inflation target:

"I agree with Powell that the Fed shouldn’t consider increasing its 2% inflation target. Such a move could undermine the Fed’s credibility and unanchor inflation expectations. Meanwhile, the main advantage — reducing the risk of getting pinned at the zero lower bound — has waned as the neutral short-term interest rate has risen."

#inflation

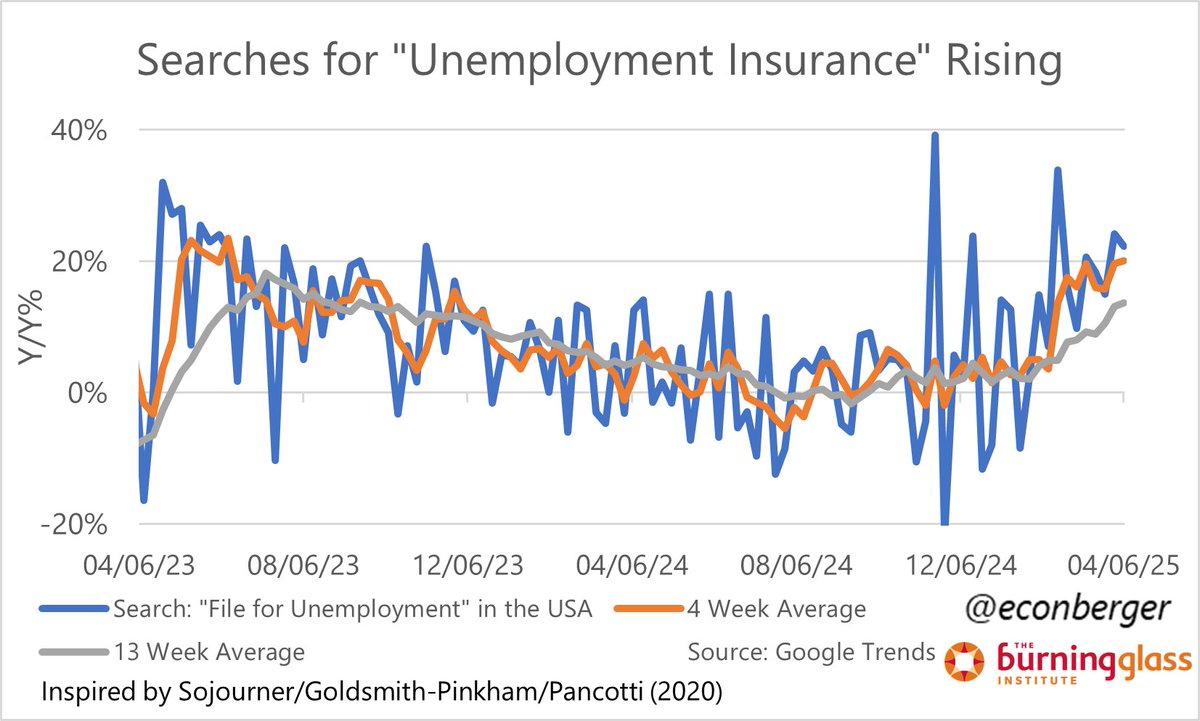

Google searches for "filing for unemployment":

1/ This thread is inspired by the great @aaronsojourner , who is a pioneer (along with Paul Goldsmith-Pinkham and @ENPancotti ) in nowcasting unemployment insurance claims using @GoogleTrends data.

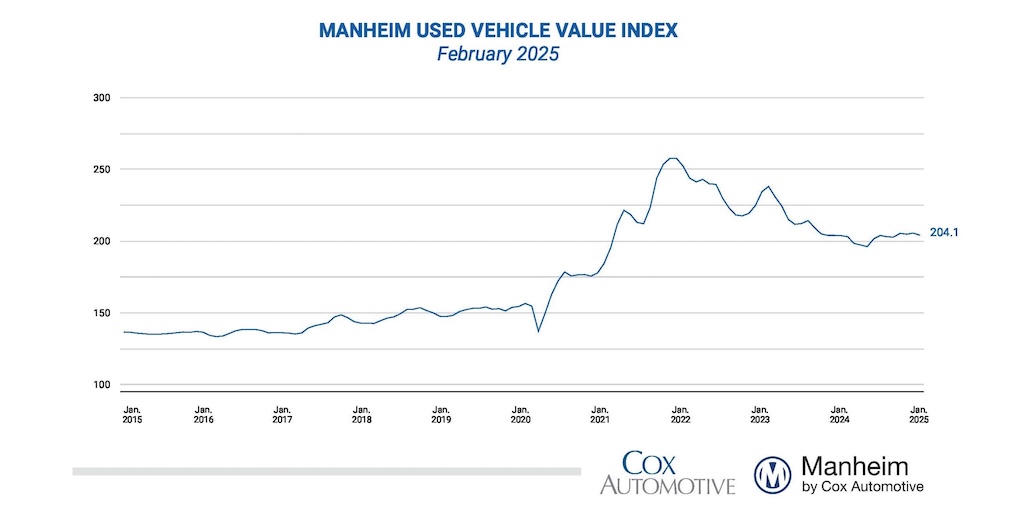

Wholesale used vehicle price (mix, mileage & seasonally adjusted) based on @Manheim_US Index declined 0.7% in February leaving the index up 0.1% y/y https://t.co/Tt0RVbysQb………… NSA ave price increased 1.4% leaving unadjusted ave price up 0.8% y/y

I’m really interested for JOLTS and to see how much of what we saw for federal government was the hiring freeze vs early layoffs (my bet is on the first)

In the week ended February 22, federal workers filing for initial claims rose roughly 1,000 to 1,654. The good news is that we already have a look at filings for the week ended March 1 and they edged lower. This will unfortunately be temporary.

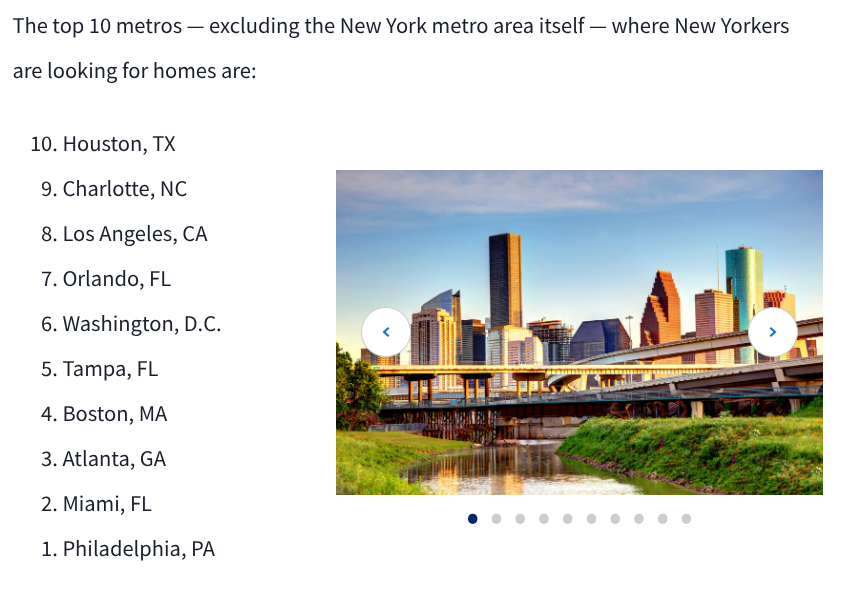

Metro pairs & gross migration: "Coming in at number one is Philly, unseating Miami as both the top metro searching for homes in the NYC area & the top metro where New Yorkers are searching for homes"

In a speech on Monday, John Williams of the NY Fed seeks to answer the question: Why is the Fed cutting interest rates at all?

"The simple answer is that while growth in demand has been strong, growth in supply has been even stronger. Specifically, robust growth in both the labor force and in productivity has meant that the economy can expand at a higher pace than we saw before the pandemic, without creating inflationary pressures."

Like Waller, he suggest progress on getting inflation down will be uneven but expressed confidence that it will return to target

Inflation is the foremost issue voters are concerned about, and how it is perceived will determine the election. Our modeling suggests Pennsylvania will be the state that pushes the eventual presidential winner over the finish line. https://t.co/ssGO8KmbiJ

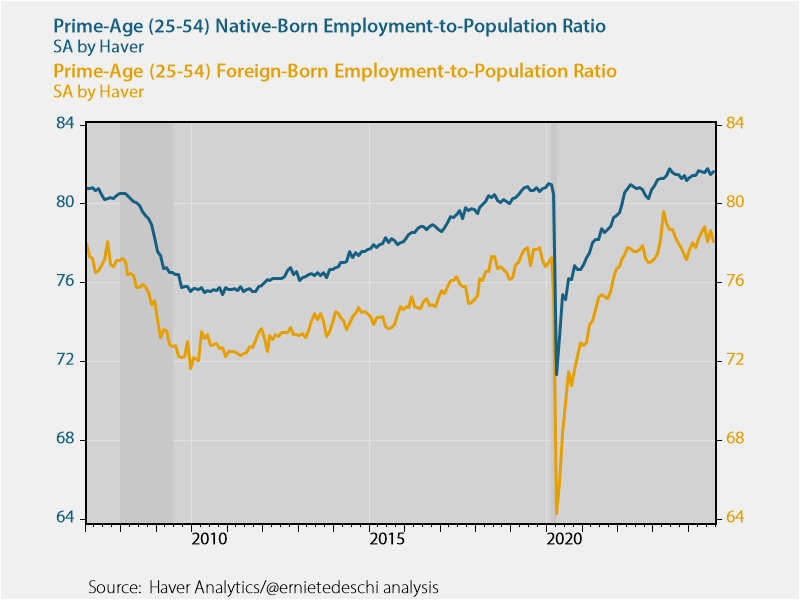

The prime-age (25-54) native-born employment rate remains both higher than the foreign-born employment rate and higher than at any point pre-pandemic since BLS began publishing the series in 2007, including higher than any point in the Trump Administration.

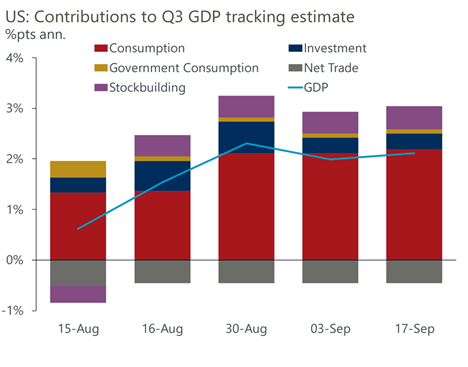

Accounting for our estimate that the PCE deflator rose by 0.11% last month, we estimate real consumption growth was up 0.1% in August. That would put real consumption on track to rise 3.2% annualized in Q3, better than Q2's gain of 2.9%. Consumer is hanging in there.

The Fed faces a finely balanced set of considerations over whether to cut by 25 or 50 basis points at its meeting that begins today.

The case for 50 comes down to what Fed officials call risk management but what might be thought of as regret minimization. Per former Dallas Fed President Rob Kaplan, if you cut 50 here and you think the Fed will need to cut again after that, you are unlikely to regret such a cut even if the economy chugs along between now and your next meeting. But if you cut 25 and things worsen a lot in the coming weeks, you'll feel bigger regret as you'll be behind the curve.

The case for 25 boils down to some combination of 1) process issues (i.e., 50 will signal something more urgent; there's an election soon; communications were not explicit enough about 50 in the run-up to this meeting), 2) a view that the economy is doing just fine and will continue to do so with more gradual reductions, and 3) that because financial conditions are easy (in part because markets expect the Fed to deliver a string of cuts), igniting risk assets could make it harder to finish the inflation fight.

There is a gift link to the full article here:

https://t.co/IXvsmRZID9

One of the most interesting things the PPI tracks that the CPI doesn't is retail markups. Retail markup growth has slowed considerably & this has been a contributor to disinflation. In August in particular, growth in grocery markups fell to 0.7% YY, the slowest in 3 years.

🇺🇸 Ryan Sweet of Oxford Economics tried a different version of the Sahm Rule focusing on the 25-54 age group; it has recently diverged sharply from the overall unemployment rate version and suggests little risk of recession - Bloomberg

https://t.co/zS3z2OdY9z

Weekly jobless claims come in at 230,000.

“I think this is a good sign for the Fed that even though the labor market has risen, it’s not because of a lot of layoffs,” Oxford Economics chief economist @RealTime_Econ says.