Profits Without People - The 19th century French Philosopher Auguste Comte argued that “demography is destiny.” If true, our destiny is about to hit an inflection point.

The US has experienced population growth since WW2. While the US fertility rate has been at or below replacement level (2.1 births per woman) since the early 1970s, net positive immigration offset fertility declines and resulted in continuous, if low, population growth (Fig. 1).

Why, and what does this mean for the economy and investments?

We’d start by asking, “what do retirees buy?” and then thinking about the impact of labor constraints on the firm. If the investment requires more people for success, whether it be consumers or workers, challenging times are ahead. On the other hand, if the firm can grow without population growth, then it is well positioned for our profits without people destiny.

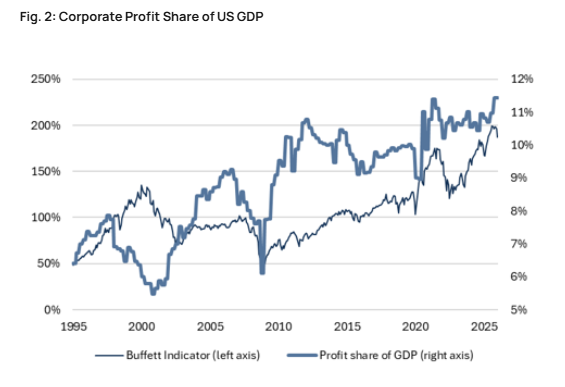

Higher profit share contributes to a higher Buffett Indicator, all else equal, but demographics, deglobalization and artificial intelligence (AI) bring a tension into the analysis. Slowing population growth and deglobalization would generally benefit for labor (wage growth) over corporate profits, but AI could lead to higher employee productivity and offset those trends.

https://t.co/3LbpymPq1l

In 2001, Warren Buffett discussed a gauge for stock market valuation that is now referred to as the Buffett Indicator. It is the ratio of the market cap of the US stock market divided by US Gross National Product (GNP).1 At the time, Buffett suggested that a ratio over 120% indicates that the stock market is overvalued. Today the indicator stands at over 200%

If the Buffett Indicator is high, it could be because:

1. The market is expensive (valuations are high), or

2. Corporate profits have increased as a percentage of total economic growth.

Just for emphasis... the wealth of the top 1% (approximately) in 1774 included the human capital of the bottom 20%, and they still only controlled half of the wealth share versus the top 1% today. And the bottom 50% had a higher share of wealth in 1774 even though 2/5ths of that segment were enslaved.

@dollarsanddata Since 1774, a year in which 20% of the American population was enslaved, wealth inequality for the top 1% vs everyone else has gotten worse, not better, in the US.

Our latest 90/60 ETF idea out today

This idea came from a client in our capital efficient overlays w/ gold.

Problem: current portfolio was 100% US stocks --likes idea of adding international, but doesn't want to sell US core.

Solution: Capital efficient Intl overlay >>>

A longer (+ 2 months) closure of the Strait of Hormuz increases the risk of global economic stagflation and an equity bear market, particularly if oil price exceeds $125 a barrel for a sustained period. Spending on crude oil, as a percentage of global GDP, would reach 2% at $125 a barrel and 3% at $200 a barrel. We would likely reduce portfolio risk if such a scenario became more likely, but believe it is too early to do so at the current time.