🇬🇧 UK investors are getting a raw deal: financial services awards are broken.

⬇️ Vote in the Finimize Awards and help us fix this ⬇️

https://t.co/4Cl7dcMBII

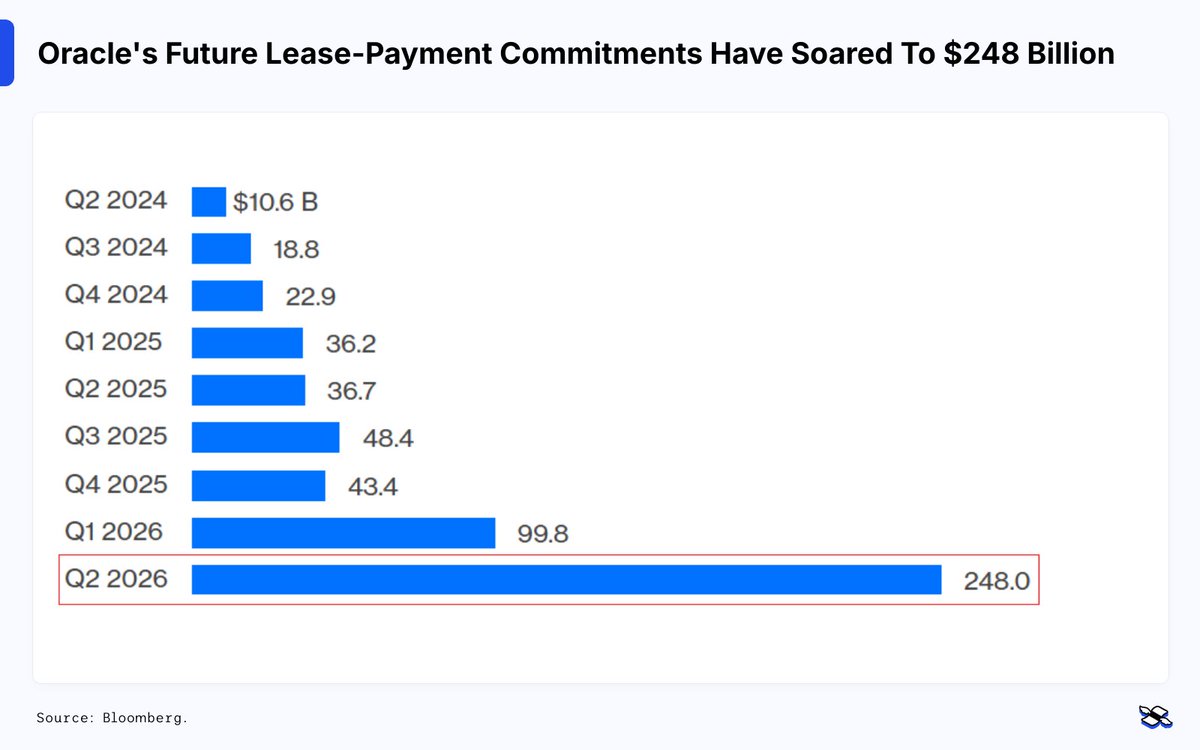

Oracle $ORCL just dropped a $248 billion bombshell. Not in its earnings call – but buried in its 10-Q.

See, the tech firm has chosen to rent rather than own the buildings that house its data centers. And thanks to recent big AI deals, its future lease-payment commitments (i.e. future rent obligations) have jumped to a whopping $248 billion – none of which shows up on its balance sheet (yet).

That’s nearly $150 billion more than previously disclosed, and it’s almost all tied to AI data-center buildouts.

The kicker? These leases run for 15–19 years, while many of Oracle’s biggest AI customers – including OpenAI – sign contracts that last just a few years.

So Oracle is locking in massive long-term payments for infrastructure it doesn’t own… while betting that today’s AI demand will still be there decades from now.

If it’s not? Profitability and cash flow could take a serious hit.

And that $248 billion in future rent is on top of the roughly $300 billion Oracle is expected to spend over the next five years decking out those data centers with GPUs and related gear.

Oracle expects capital spending to more than double to $50 billion in its current fiscal year. That’s about 75% of the revenue it’s forecasting over the same period.

All of this is very risky. Here’s a (non-exhaustive) list of what could go wrong:

• OpenAI walks away from its Oracle contract

• OpenAI, still burning lots of cash, struggles to honor its massive spending commitments

• After OpenAI’s contract ends in 2030, Oracle can only rent out those data centers – now running older GPUs – at much lower rates

• AI demand cools or shifts to more efficient hardware, leaving Oracle stuck with long-term leases but underutilized capacity

• Next-gen GPUs arrive sooner than expected, forcing Oracle into expensive mid-lease upgrades

Investors aren’t impressed – and a 40%+ slide in Oracle’s stock since peak AI euphoria pretty much says it all.

Brought to you by the @finimize chart of the day.

"I don't think many people understand how profoundly AI is going to transform healthcare."

- @CathieDWood

Catch the Modern Investor Summit live now:

https://t.co/RQcCitqRlA

Today’s @Finimize chart of the Day shows Gemini is steadily closing the popularity gap with ChatGPT.

A year ago, plenty of people had written off Google’s stumbling attempt to close OpenAI’s massive lead. With fears that ChatGPT (and AI search upstarts like Perplexity) would eat into its search cash cow, Alphabet’s stock trailed its Big Tech peers in the AI-fueled rally of 2023 and 2024.

But the mood has flipped in 2025. A confident set of upgrades at May’s I/O developer conference, plus the viral hit of its “Nano Banana” AI image tool over the summer, have helped revive momentum.

The payoff: monthly users of the Gemini mobile app have surged to 650 million, up from roughly 400 million in May. Investors are buying in too: Alphabet is up around 70% in 2025, making it the best performer in the Magnificent Seven and more than doubling Nvidia’s gain.

Week-ahead preview: Inflation and inflation expectations

🔎 It’s a packed economic calendar this week, but here’s the real thing to watch: the Fed’s preferred PCE inflation and consumers’ expectations, which could make or break the next rate cut.

The consumer price index (CPI) tends to grab the headlines, but when it comes to inflation gauges, the Fed’s favored the personal consumption expenditures report forever. And that’s because the PCE, as it’s known, covers a broader range of items and actually adjusts to how folks spend – for example, when they choose a substitute because a price has gone up. It also factors in data acquired by surveying businesses. So it’s more useful than the ol’ CPI, which is a pure-and-simple record of the cost of a set basket of goods.

The PCE’s all-items inflation rate peaked at 7.2% in 2022 but has hovered between 2% and 3% since. Economists expect September’s pace to sit at 2.8%, up from August’s 2.7%. That’s the bad news. The good news, however, is that they expect the core measure – which strips out volatile stuff like food and energy to give a better idea of underlying price pressures – to dip to 2.8% from 2.9%.

Still, inflation’s stuck above the Fed’s 2% target, and more importantly, people are starting to expect that it will continue to linger. And that’s a problem. When people and businesses anticipate higher prices, they act accordingly – asking for bigger wages, raising prices earlier, and rushing to buy things before costs increase. All of that can turn inflation into a self-fulfilling cycle.

That’s why traders will also be watching the US consumer sentiment report (due Friday, too), which includes closely watched inflation expectations. If those jump or inflation runs hotter than forecast, the Fed just might rethink its rate-cutting game plan.

The central bank has lowered interest rates twice this year in response to a softening labor market, and traders are betting on another cut next week. But any hint that inflation might be picking up speed would complicate those plans, forcing policymakers to weigh the trade-off between supporting the job market with lower borrowing costs and reigniting price pressures as a consequence.

👉 Liked this post? Follow us for institutional-grade markets and investment research – built for the modern investor.