In a static system (i.e. assuming that the flows do not affect the timeline of Hormuz reopening) - yes. But if the flows suppress the price and prolong the disruption period (since neither side would feel they need a deal right away or that conditions maximise their leverage) it will be a net negative.

Btw those flows reduce the available "inside Hormuz" reserve, which is supposed to smooth the ramp up period (and help to create a "flood of oil").

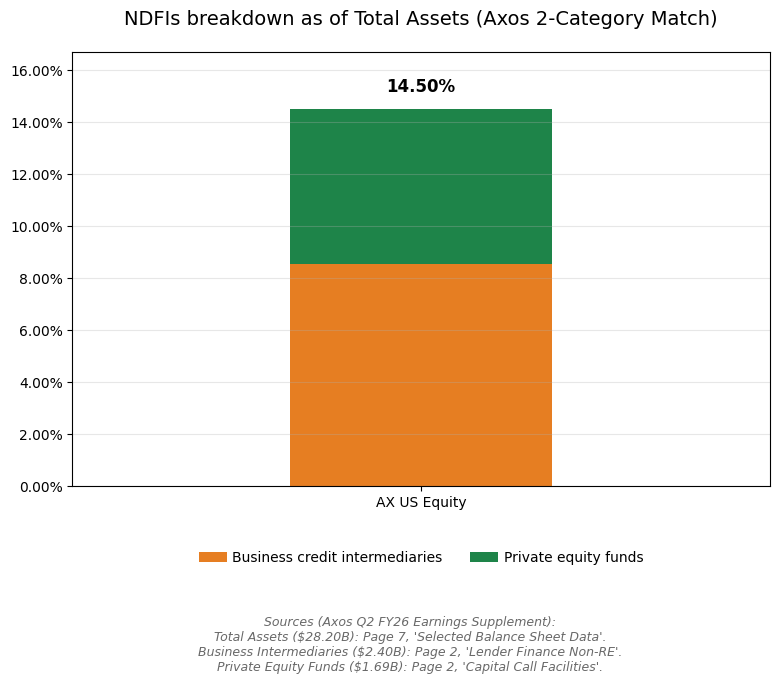

@JoshYoung https://t.co/1fufdLFVNH

Some relevant context - seems this pushes back on the significance of dark fleet STS transfers. Flows are still FAR too low to make a significant dent in inventory draw pace.

Here is what “very meaningfully” looks like once you compare it with the data: precisely nothing. At this point, Energy Secretary Wright gives the Pravda a run for its money.

Source: Kpler; incl. crude & products, LNG + LPG tankers - both with & without transponder signals

A good point, but something I always keep in mind with respect to quant strategies is their streakiness. Which likely suggests that yes, alpha does exist, but another often overlooked aspect are fund flows driving returns. Thus, why trend following applied to a quant strategy in theory seems like a solid strategy.

I haven’t verified the cause of streakiness but just my intuition.

Sure is hard when the indices become a single factor bet. Capex up 70% YoY in 2026 against ~$150-180B in disclosed hyperscaler AI revenue. Question I've been pondering is, what % of that revenue traces back to frontier labs and VC backed startups (which themselves funded by hyperscaler equity and venture capital) vs real arms length enterprise demand? Hyperscalers don't disclose customer concentration. Hard to know. But strip out the subsidized portion and the ROI math on 750B/year of capex looks meaningfully different.

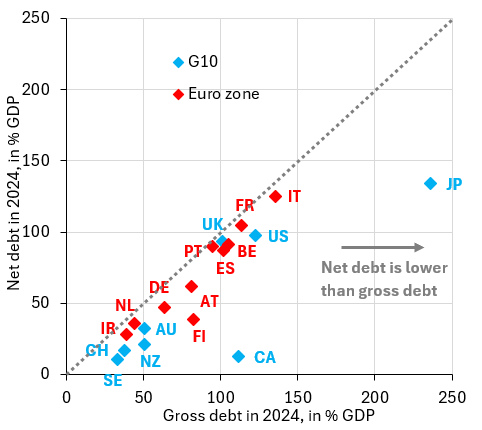

Yep, a high inflation environment triggers an automatic deleveraging cycle on a net basis. I see the 235% gross debt always cited, but it completely ignores the other side of the balance sheet. 135% net debt requires netting out 100% of GDP state asset buffer:

Forex reserves: 30% GDP

GPIF assets: 33% GDP

FILP capitalizations: 37% of GDP

Liabilities are almost entirely domestic while the asset portfolio is weighted toward foreign currency.

Rising domestic inflation directly erodes the real burden of the 235% gross domestic debt. Any resulting JPY depreciation then mathematically expands the JPY valuation of the foreign assets. I.E. JPY depreciates 20 percent against the USD, the real value of domestic debt falls while the FX reserve buffer instantly increases in value by 20 percent. The falling value of domestic liabilities and increase in the foreign asset base engineers a rapid net deleveraging.

Japan seems to finally be working through the debt woes!

@frothyassets Has to do with the JHEQX collar roll combined with quarterly rebalancing, and now leveraged ETFs buying.

JHEQX was ~10 bln buy flow today, mandate funds were around that, potentially bigger, and now LETFs are around that size due to the one sided price action today.

@ShortSeller https://t.co/DhftgUc4LZ Don’t let the little people steal your focus and energy, Andy. The true test is having character - and that you have my friend! Keep up the great work, always amazed at your charting abilities

Matt was a junkie who was living in his car. I got him clean, and gave him and his wife a place to live. He is the most incredible person I have ever met. He does my carpentry, electrical, plumbing, landscaping, and ANYTHING I task him with. He had never worked on a car, but after watching YouTube videos has since replaced the wheel bearings, blown head gaskets, engines, brakes,etc in my various Prius and Outback's. If I needed open heart surgery tomorrow, Matt would watch YouTube video's and perform it. Matt is priceless to me. Matt will always be the 1st cost I will pay, and I am confident he will pay it forward (not that he owes me anything).

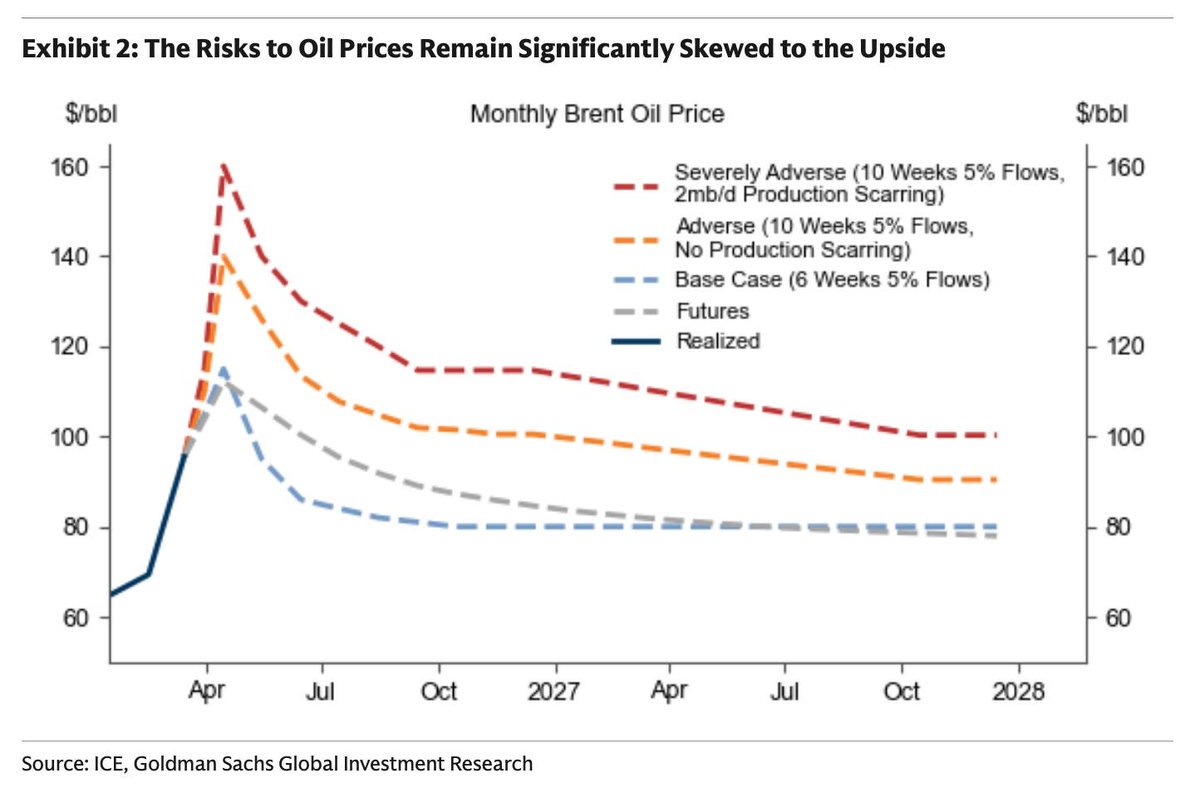

Yep, time and degree of energy infrastructure damage are the two key variables (chart 1). Relatively benign now, but has the potential to turn into a tail event. Global oil on water is close to 2025 lows - notably Asia is now back to pre-Russian sanction levels- meaning globally, we'll likely start dipping into on-shore reserves. Expect price going forward to be more unruly barring any resolution.

Starting to think an invasion may actually be a bull case. Initial sell-off, but markets begin to price reopening of the strait.

Iran is an existential front for the American empire. Can’t leave w/o a settlement, would be viewed as a loss left for our allies to clean up. Iran has zero incentive to negotiate, and even if they were open, DC is delusional about the state of US power & our real bargaining position. No clean exit. Agreed, boots on the ground are likely the next move. Ignore the words, track the military asset movements.

I’m seeing about a 3.50 spread prior to this war. It’s blown out to ~8.00 which seems a fair bit wider than normal. On the front month, now approaching ~$15.00. Have to imagine tier 1 guys like Trafigura are attempting to arbitrage the living hell out of this spread.

Makes you wonder if oil export bans are coming. Seems to be the talk of the town.

@orrdavid@ferderser Oil tourist here, but BRNZ2026 is saying something a bit different. Might be more representative of oil scarcity given US’s proximity to oil production.

@DsrPrivate On the 110 naked put, if we were to blow through that, hit the 109 stop, and IV has expanded considerably, would you delta hedge through ZN futures as opposed to buying back the contract? Trying to think through the worst case scenario there and how to best execute. Thanks!