@GagolaValue@Trading212 I got caught with this during the England game and got double excited then realised it was just a few out of hours shares and no catalyst behind it

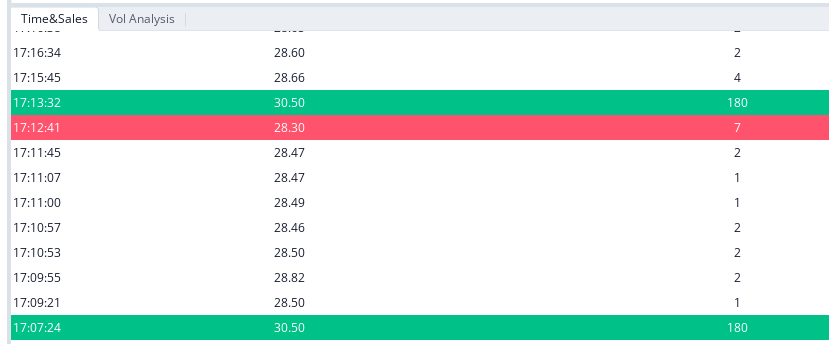

The shares genuinely changed hands for $30.50 but only 360 of them

@investingwithac yeah, it's the opposite, they seemed to have pumped up Q1 2024 numbers but the opposite in 2026

I suspect they were however guessing more at the 2024 RA and have more of a scientific method and better data now

@DanNeidle Early indicators of third order effects of the £100k tax trap, the group of 45 - 59 year olds were in their earning primes in early 2010s earning £100 to £150k, sacrificed buckets into their pensions, made fortunes from the US Stock boom, retired early.

I'm with you, I see the update coming late June or first week of July with the quiet period and no news then immediately starting in the run up to Q2 earnings

Scott may as well have been holding up a sign saying "big beat and raise imminent" with his chat the other day

What a time to be alive!

I love it and it is what we have heard Mark B and Cathy Grason talk about with getting state legislators to adopt ICHRA and promote it with a few carrots.

However this could be pocket change compared to what could happen in the possible third reconciliation bill. The Republican Study Committee/ R. Pfluger seem to be wanting to put the HR6703 / CHOICE legislation into it

Specifically the policy framework includes (quoted verbatim)

1) Reform the existing Affordable Care Act (ACA) subsidy structure so that money flows directly

into the hands of patients through Health Freedom Accounts

- So money in the hands of the consumer to buy the insurance or ancillary care they need, this has Lucie written all over it!

2) Require health insurance companies and providers to disclose cash prices for medical care and

disclose out of network access to low cost providers, enabling patients to pay cash rates for

care and see the doctor they want.

- You may as well just call this the "push every person to Lucie" clause

3) Codify policies included in the Lower Health Care Premiums for All Americans Act to expand

Individual Coverage Health Reimbursement Agreements and offer two year, per employee

tax credits for businesses under 50 employees, and codify Association Health Plans.

- This is ICHRA, or CHOICE as it would then be called codified at the Federal level

If these get encapsulated into US law, then the sky is the limit for Oscar and Mark's pirate cannons will be firing broadsides into those legacy Galleons

Nothing in my thesis of why I am heavy into this company now comes close to the effects the above would have over the next 5 years.

@X

Guys, I get why you have done this but please please make this tickbox that allows me to hide all the spammers work again on an opt in basis.

FinX research and information sharing has become next to impossible

It's amazing how few people are doing this relatively simple analysis themselves and even fewer understanding the implication that this is saying a fair value on a fundamental basis for Oscar shares is circa $100 each right now, not in 5 years but at this instant in time

78.0% - 78.5% is my base case for MLR and a few of these tailwinds are telling me it could be lower, some of which are on a one off basis and some are structural.

14.5% - 15% SG&A also seems to be the trend, elevated in Q1 due to the extra risk adjustment accrual which will likely be added back in coming quarters

I also realise what happens when you take 100% and subtract the midpoint from the above numbers. I'm almost too scared to write it down.

Guidance is about to be raised by a substantial amount, somewhere between x1.5 and x2.5, that could be anytime between Mid June and the Q2 earnings call in 60 days but it will happen in this short time frame

If the above plays out for the full year and the outlook for 2027 is positive based on the Feb 27 full year earnings call.. then I retire from my 9-5 and I am a free man so I do accept my bias but to paraphrase Scott Blackley the CFO from his fireside chat a few days ago

I keep looking for some piece of bad news about $OSCR. And at this point, I just haven't seen any.

With the wafer thin liquidity and wide bid/ask spreads on the one clearinghouse open around that time, it was probably just some drunk degenerate throwing a few $k in and climbing the order book ladder momentarily hence the instant vertical line

Anything outside of normal trading hours is noise unless there is a genuine out of hours catalyst

The Street was listening to that and heard what we heard which was (paraphrased)

"We aren't increasing guidance yet because the Wakely report is the key to us doing that responsibly but here is a list of all the tailwinds that have really already crystalised that are going to add $250 - $300m to this year's profit that we haven't already accounted for

The Wakely report is coming very soon so hold onto your britches or they'll be blown right off"

I'm looking at the pattern for last year, 22 July was when the bad 8k hit tanking guidance

Mark recently said in an interview over at Ivy .com that they got the Wakely report then reported to The Street within 2 days with what it meant so that must be when the next one is due +- a few days. I also think there are 5 a year published but I have no idea where that titbit came from. This does suggest assuming they are equally spaced that one came in early May i.e. 2.4 months apart assuming equal spacing but no raised guidance on the back of it on the earnings call.

I have no idea what my point is here, probably just using you to get my thoughts and expectations straight. i think it is that we shouldn't expect any movement until late July but that would also be a quiet period so we shouldn't expect anything to change until Q2 earnings reported on circa 6th Aug

@investingwithac I was kind of disappointed the best words in the English language "Meet or exceed" were not in there but not going to mope about it all day

Have we massively underestimated medical cost inflation? No, we've put it at 10% and we're still getting sub 80% MLR for 2026

Have we overestimated new membership? No, there is no way they are shrinking with this level of app downloads and 250 new roles being advertised during Open enrollment, combined with @Steelmindcap 's incredible work on the credit card data we are not wrong.

Is SG&A going to blow up? No, it's clearly trending down to the fixed costs of taxes and broker fees

Is anyone at Oscar showing panic? No, calm, composed and locked in

The 4 year old middle child ran the maths on a bit of A4 paper and said 5% in 2026 would be reasonable given what we've seen and what we know, personally I think he is trying to get on my good side so he gets Kirby for his Nintendo on his 5th birthday but the numbers do check out.

The youngest is more bullish and worried about rebate accruals capping the bottom line

Something that seems to have not been spotted by FinX yet in the $OSCR bull case, 2 days ago Dr Oz at the CMS announced fees for carriers in the ACA market were reducing from 2.5% to 1.9% for Federal Marketplaces (FFE) and from 2.0% to 1.5% for State marketplaces (SBEs) for 2027?

Why does this matter you might say, it's tiny!

Here is why it does:

1) This is effectively a reversal back to 2025 pricing, CMS put the fees up for 2026 because they expected 30% reduction in market place size and needed to maintain income. So evidently, this bear case is now gone i.e. ACA shrinkage is minimal and we're hearing it indirectly from the horse's mouth

2) The fee is based on the gross premiums, that's before risk adjustment so disproportionally benefits Oscar who have a high risk adjustment of 20%. As an example a person paying $8.0k a year for coverage would appear on the revenue line for Oscar as $6.4k then incur a FFE CMS market place fee of $200 which is 3.125% and makes up that amount in the SG&A costs. This effect is now $152 so 2.375% falling into SG&A, this a 75 bps improvement on SG&A from the stroke of a pen or roughly one $ in twenty lower SG&A costs

3) "That's still immaterial" some will say, however a gold standard for ACA insurers is 5% margins, that means 15% more profit going from 5% margins to 5.75% margins and even more at the lower end when profits are only 2% or so of revenue

4) Oscar predominantly operate in the FFE markets, the SBEs are rates are down as well albeit marginally less, it will effectively have the same impact on the sub 10% of members Oscar hold in SBEs

Mark B said this in the latest earnings call

"taxes and fees are pretty much fixed for us based on the level of membership. It's 9%-10%. We're looking at the variable piece that we can manage versus that fixed piece, which we literally is sort of a tax for being in the game."

so that 9% to 10% range, just dropped to 8% to 9%

announcement in the link for the detail orientated folks

https://t.co/hCiye6w9uf