Also worth noting an important clarification that transfers of S&S ISAs to Cash ISAs WILL be permitted for over 65s, thereby retaining full flexibility of two-way transfers from that point.

The rules were always going to be clunky and add complexity to an already-cluttered ISA regime. But thankfully investors are to be spared draconian restrictions around 'cash-like' investments that would have undermined perfectly normal risk management.

https://t.co/bEdh4yE5GJ

@John_Stepek I imagine most money market funds would be in the line of fire. Harder to argue short dated gov. bond funds are 'cash like'. The more worrying part is that loads of perfectly normal activity such as derisking for house purchase or renovation is harder / more taxable.

Watch The Spectator's post-Budget briefing live tonight at 7pm.

Economist Stephanie Flanders joins our editor Michael Gove, our political editor Tim Shipman, our economics editor Michael Simmons, and John Porteous from Charles Stanley to give an insider’s take hours after the Budget is announced.

If you want to receive a reminder 30 minutes before the event starts, click the link and complete the form.

@michaelgove@Simmons__@ShippersUnbound@MyStephanomics@_CharlesStanley

https://t.co/lxU4g7BfIK

£12k limit on Cash ISAs for under 65s: Some people who are unable to take risk with their money will see their tax-free options significantly curtailed. For them there are some low risk options in Stocks & Shares ISAs such as money market funds.

Investment involves risk #Budget

Restricting salary sacrifice from April 2029 isn’t an explicit tax rise, but many employees will either see less in their pay packets or in their pension pots. The long-term effects on the nation’s retirement pots could be considerable.

Investment involves risk #AutumnBudget

Two possible loopholes to the lower Cash ISA allowance. Open a £20k Stocks & Shares ISA and then transfer to a Cash ISA, or hold cash or a money market fund in a Stocks & Shares ISA. I'd expect the first to be closed off, but probably not the second.

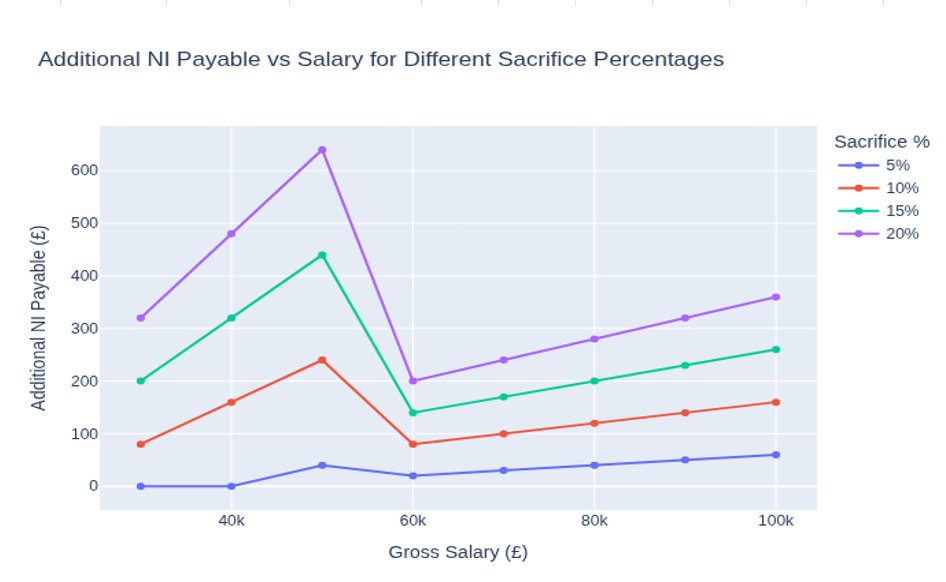

Appreciate full details to emerge, but if this Budget rumour is true as outlined, limiting pension salary sacrifice to first £2k earnings really hits those with pre sacrifice earnings in the £40-50k region and making large contributions. This is because NI is 2% > £50,270 not 8%.

Perhaps a compromise would be to permit all UK listed shares and domiciled funds and exclude overseas. Support UK market and financial services without overly restricting consumer choice.

No surprise today on UK interest rates. With September's CPI set to be c. 4%, the figure at hand for the November meeting, an extended pause beyond looks odds on. Budget also complicates matters and December will offer more clarity, but doubts over inflation cooling by then too!