We need new ideas to lower mortgage costs for young families. Here's one: have the GSEs provide a targeted backstop bid for MBS to lower the 30/10 spread, which is costing young Americans extra cash.

Community lenders think it will work.

$fnma $fmcc @pulte@FHFA@FannieMae@FreddieMac

https://t.co/xl1RWsYtky

@theclearthinke1@robbysoave No the world needs more people of action, making a better tomw.

We already have too many useless doomsayers. And most of what they predict ends up wrong anyway.

And of course mortgage ppl would rather have peace in the Middle East and sub 6% mortgages, but we gotta live with reality, and the backstop bid delta is real $$ for first-time homebuyers and others.

US 10-year Treasury rate, June 2, 2025: 4.46%

US 10-year Treasury rate, June 2, 2026: 4.45%

But....look at the US 30-year, fixed-rate mortgage coupon then and now.

GSE backstop bids for MBS make a difference, people.

@FHFA@pulte@NewsLambert $fnma $fmcc

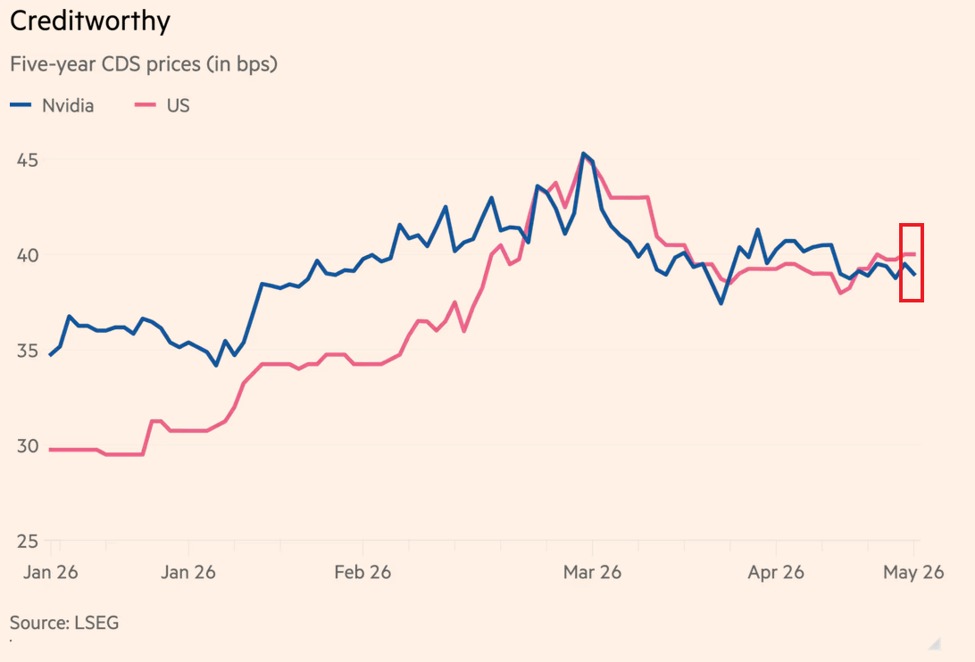

This is absolutely incredible.

Investors now perceive Nvidia to be as creditworthy as the US government.

Nvidia's $NVDA, 5-year credit default swap (CDS) is trading at ~38 basis points, slightly below the US sovereign CDS, at 40 basis points.

In other words, markets consider the world's largest company to be less likely to default on its obligations than the US federal government.

This comes as in FY2026, Nvidia carried only ~$8.5 billion in total debt against ~$10.6 billion in cash and generated nearly $100 billion in free cash flow, giving it one of the strongest balance sheets of any company in the world.

Even if Nvidia's earnings dropped -90%, it would still rank among the 100 most profitable companies in the world.

Markets are treating Nvidia as one of the safest companies on the planet.

A reasonable expectation is: they are looking to buy a major nonbank lender as well, before valuations recover from this long sector slump. $BRK.B

(Reminder: this sector cannot recover fully until gov't addresses the endless, and inefficient, conservatorships of $fnma and $fmcc.)

https://t.co/jCrhvSlNTJ

While we’re at it here, roll back that Internet thing. And electricity too—bring back those many tens of thousands lamplighter jobs.

https://t.co/L6wesFzzjq

@0xtechquity Growth is ONLY coming from mortgage credit score price hikes and they can’t keep raising these bc too many in Washington DC are deeply unhappy about it.

@unciacapital Change is coming. Americans hate monopolies. So do lenders & their customers.

Defend a monopoly—that’s pissing off a lot of people—at your own peril.

@Larryjamieson_ This guy, as usual, gets it.

“Eisman said he is short FICO, the company best known for its widely used credit scores, arguing that its pricing strategy has alienated customers and opened the door to competitors.”

Steve Eisman likes the market overall here, but:

“Eisman said he is short FICO, the company best known for its widely used credit scores, arguing that its pricing strategy has alienated customers and opened the door to competitors.”

Yep.

$fico $fnma

https://t.co/0qXoQBEWcy

You are missing the Big Picture. Americans hate monopolies. And with any monopoly, there is no price discovery, which incents abusive pricing.

Also—basic economics tells you that monopolies by their nature inhibit innovation.

Which is why the US mortgage market has been using an outdated product. Even the FICO ceo admits the current product is inferior.

@em013L Wrong. Change is coming. MBS investors will easily incorporate VantageScore 4.0. And lenders want more options here for their customers bc a monopoly is naturally abusive.