Drop these two Meta updates into Bobby, see how they actually move $META, then make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/BoDgsJX8UP

Meta's chief AI officer Alexandr Wang told employees at a town hall that the company's next model, codenamed Watermelon, has caught up with OpenAI's GPT-5.5 on benchmarks, according to two sources cited by Business Insider. The same week, CEO Mark Zuckerberg admitted at a separate internal meeting that AI agent development hasn't accelerated over the past four months the way the company expected, and that the high hopes executives had for Anthropic's Claude Code haven't materialized yet.

Watermelon is still in training and uses roughly ten times the compute of April's Muse Spark (internally codenamed Avocado). Wang didn't specify which benchmarks he cited. On Artificial Analysis' Intelligence Index, GPT-5.5 (xhigh) scores just 55, already trailing Claude Opus 4.8 (56) and Claude Fable 5 (60). On llm-stats, Gemini 3.1 Pro currently leads the coding arena, and Claude Mythos Preview tops GPQA Diamond at 94.6%. In other words, even if Watermelon truly matches GPT-5.5, it's catching up to a model that's no longer at the front of the pack.

Zuckerberg was blunt in his own remarks: the trajectory of agentic development "hasn't really accelerated in the way that we expected." He also acknowledged the layoffs and reassignments tied to this year's AI restructuring weren't as "clean" as they should have been, and that leadership misjudged the timing.

Here's the chain: Meta cut about 10% of staff and reassigned 7,000 to AI teams earlier this year, betting agents would boost productivity. Four months later, that acceleration hasn't shown up, so leadership is now reviewing the restructuring instead of pushing forward unchanged. At the same time, the "caught up with GPT-5.5" line goes out publicly, effectively giving Wall Street a story to hold onto for $META 's AI infrastructure spend, now guided as high as $145B, up from an earlier $115B-$135B range. Translation: this reads more like expectation management ahead of an earnings call than a product launch.

Worth noting: Muse Spark did beat rivals including Opus 4.6 and Gemini 3.1 Pro on HealthBench Hard when it launched in April, but Meta itself admitted the model still lagged on "long-horizon agentic systems and coding workflows" — the exact area Zuckerberg now says hasn't accelerated.

The pushback is straightforward too: Wang's claim comes from a single Business Insider report citing anonymous sources, with no published methodology, and neither Meta nor OpenAI has confirmed it. Muse Spark itself was originally slated to ship by late 2025 and slipped to April, so "caught up" claims from Meta have missed before.

Claiming parity with a frontier model in one breath and admitting agents haven't sped up in the next reads less like a product story and more like narrative support for a $145B infrastructure bill. Whether Watermelon actually delivers will likely only be clear once it ships and independent evaluations run. Zuckerberg says the payoff shows up in three to six months. Do you think this time it holds?

Drop this Dow-record-vs-chip-selloff split into Bobby: see how it actually impacts the tickers you're watching, then make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/CXbVQGkEJZ

The Dow closed up 594.18 points (+1.14%) at 52,899.42, a fresh record high, while the Nasdaq fell 207.36 points (-0.80%) to 25,832.67 and the S&P 500 inched up 0.01% to 7,483.24. Two opposite forces were driving the market on the same day.

June US payrolls: +57K vs Est. +113K 🔴; unemployment rate 4.2% vs Est. 4.3% 🟢; April-May revised down a combined 74K. After the release, traders raised bets the Fed pauses in July, lifting rate-sensitive Dow components to a record close.

The Nasdaq told a different story. Chip and storage names got hit: $MU -5.4%, $SNDK -14%, $INTC -5%, $STX and $WDC both near -10% on Nasdaq. The trigger: Mark Zuckerberg told Meta staff at an all-hands that AI agent development "hasn't accelerated the way we expected" over the past four months, sending $META down almost 5%. Vital Knowledge analysts then cut their 2026 Fed rate-hike forecast from "1-2 hikes" to "0-1."

Translating the chain: weak payrolls lowered rate-hike odds, lifting Dow blue chips. But Zuckerberg's admission, layered on top of Meta's earlier plan to resell excess AI compute externally, shook the "compute is permanently scarce" narrative that's held up AI infrastructure valuations. That doubt spread straight into storage and chips, dragging $MU and $SNDK lower and pulling the Nasdaq into the red, a split from the Dow's record.

$AAPL was the outlier, up 4.8%. One week earlier (June 25), Apple dropped 6.12% in a single day and lost $263.4B in market cap after announcing Mac and iPad price hikes. Same underlying logic this time, storage costs passed to customers, but sentiment flipped from "a price hike kills demand" to "a price hike proves you have pricing power to protect margin." Micron's chief commercial officer Sumit Sadana has suggested Apple's own history of squeezing suppliers on price helped cause this shortage in the first place. Same storage price spike, two stocks moving in opposite directions.

New Fed Chair Kevin Warsh said Wednesday the Fed is charting a new course built on real-time data, but declined to give forward guidance on rates, leaving a July pause an open question. Zuckerberg, for his part, gave Meta a three-to-six-month window before AI shows a clearer payoff.

The Dow's record rests on a fragile trade: weak data, easier Fed. The Nasdaq getting dragged down by chips and Meta on the same day shows the AI capex monetization anxiety hasn't gone away, it's just been papered over by the index headline. This week: Dow +1.97%, Nasdaq +2.12%, S&P 500 +1.76%. US markets are closed Friday for July 4th, observed a day early since the holiday falls on a Saturday. Meta's late-July Q2 earnings, and how it frames the AI agent roadmap, may be the next real test. Does "weak data, strong stocks" hold up through the July FOMC meeting?

Drop this jobs-report miss into Bobby, see how it actually impacts the broader market (like SPY/SPY/ SPY/QQQ), then make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/CoDwtA8chJ

U.S. nonfarm payrolls rose by just 57,000 in June, well below the 115,000 Bloomberg consensus, while the unemployment rate unexpectedly fell to 4.2% from 4.3%. The drop isn't because more people found jobs, it's because the labor force participation rate plunged to 61.5% from 61.8%, the lowest since March 2021, as workers dropped out of the labor force entirely.

The data:

Payrolls: 57K vs Est. 115K 🔴

Unemployment rate: 4.2% vs Est. 4.3% (flat expected) 🟡

April revision: 179K → 148K (-31K)

May revision: 172K → 129K (-43K), combined -74K

Average hourly earnings: +0.3% MoM to $37.64, +3.5% YoY

Institutional voices: Jefferies senior economist Thomas Simons noted the pace is strong enough to hold the jobless rate steady without wages overheating, leaving the Fed little urgency to move. Principal Asset Management's Seema Shah said the report weakens the recent "renewed labor market strength" narrative while easing pressure for Fed tightening.

Causal chain: The payroll miss plus the 74K combined downward revision → traders all but scrapped bets on a September hike (per CME FedWatch) → the 2-year Treasury yield fell 3.5bps to 4.13% → U.S. equity futures rose, with rate-sensitive growth and tech names ($QQQ, $SPY) getting a near-term lift → but the participation-rate plunge signals a supply-side pullback, not demand strength, so a soft September print would reopen uncertainty over Q4 policy.

Micro example: The household survey showed 507,000 workers effectively vanish from employment in a single month, roughly the working population of a mid-sized city dropping out overnight. Leisure and hospitality shed 61,000 jobs, a summer hiring season that was supposed to get a World Cup boost instead came in soft.

Opposing view: E.J. Antoni, chief economist at the Heritage Foundation, called the report "ugly," noting that after the downward revisions, June's real net gain was actually negative (-17K), meaning the labor market looks weaker underneath the headline.

The miss eases near-term hike anxiety, but a falling jobless rate driven by people leaving the labor force isn't historically a healthy combo. Is this participation drop short-term noise, or the start of a structural labor-market pullback?c

Drop Anthropic's chip plan into Bobby, see how it actually impacts supply-chain names like $TSM and $AVGO, then make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/ZGq03ltGRT

🚨Anthropic has started early-stage work on its own AI chip and is in talks with Samsung over a 2nm process and advanced packaging.

The move follows OpenAI and Broadcom's June 24 unveiling of their first inference chip, Jalapeño, and retail investors might read both as "AI labs are ditching Nvidia" — but $NVDA 's (Nasdaq) AI chip market share currently sits at 74%, higher than before this custom-silicon race heated up.

Anthropic's project is at the earliest stage: the chip's target workload, compute specs, and server configuration are still undecided, and the only concrete step so far is hiring Clive Chan, an early member of OpenAI's own custom silicon team. Talks center on Samsung's 2nm (SF2/SF2P) process and advanced packaging. Samsung's 2nm entered mass production in late 2025, with early yields near 70%, and its Taylor, Texas fab is set to start 2nm output in 2027. For comparison, OpenAI has already run the full cycle: Jalapeño went from design to tape-out in nine months, with a claimed ~50% cut in inference cost, though it won't be sold externally and is meant only for OpenAI's own use and Microsoft's data centers, targeting deployment by end of 2026. The real manufacturing bottleneck sits with $TSM (NYSE): its 2nm (N2) capacity is already booked by Nvidia, Apple, AMD and others into 2028 and beyond, with lead times of 78-104 weeks.

Anthropic's statement to TechCrunch matters here: AWS Trainium, Google TPUs, and $NVDA GPUs "will continue to be pivotal to its compute strategy," this is diversification, not a supplier swap.

The chain: if Samsung actually lands the Anthropic order, it grabs a marquee AI client right as $TSM's capacity overflows, repricing Samsung foundry's entire valuation story, a business only now climbing out of consecutive losses and targeting over 2 trillion won in operating profit this year. It also validates $AVGO 's (Nasdaq) "chip design partner" model as repeatable beyond OpenAI. None of that, though, translates into Nvidia losing share, because AI compute demand is still growing faster than alternative chips can mature.

Concrete numbers: Samsung, SK Hynix, and $MU (Nasdaq) all joined Anthropic's $65B Series H in May as "strategic infrastructure partners," a round that pushed Anthropic's valuation to $965B, passing OpenAI's $852B. A single Samsung 2nm wafer now costs over $30,000, roughly 50% more than the 3nm generation.

Pushback: Samsung's leading-edge yields have historically lagged $TSM, and whether it can hold 70% at volume is unproven. Anthropic itself admits the project could still be shelved, so calling this "successful in-house silicon" is premature.

Right now Anthropic is still at the "hiring plus foundry-shopping" stage, while OpenAI has already put a physical chip in Altman's hands. How long do you think Anthropic needs to catch up, or does it even need to?

Drop this print into Bobby — see how it moves $000660.KS and $005930.KS. Make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/xKXQR3ygHP

🚨BREAKING SK Hynix ($000660.KS) surges 11%, Samsung ($005930.KS) up nearly 9%, KOSPI's gain widens to 6%, back above 8,100 — under 24 hours after an 8% rout on AI-overcapacity fears. Korea's chip duo is erasing yesterday's panic almost in full.

Drop Meta's compute-leasing news into Bobby — see how it actually moves $MU and $SNDK, then make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/wsnFxLdnNp

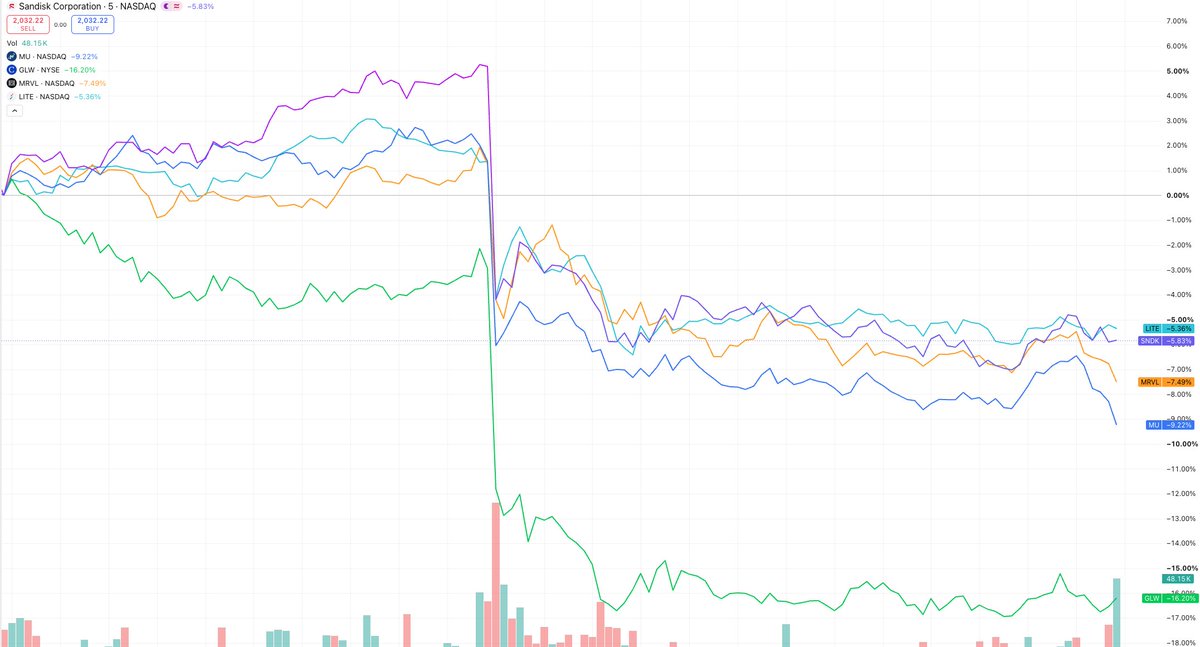

On July 1, memory and optical stocks got crushed on Wall Street: $SNDK -10.82%, $MU -9.7%, $GLW -13%+, $MRVL -7%+, $LITE -6%+, after Bloomberg reported Meta is building a cloud business to rent out its idle AI compute capacity. The market read it as an "AI compute glut" signal, but the more likely story is that Meta's own models aren't strong enough to absorb the capacity it has stockpiled.

$META jumped over 10% the same day to around $619, after being down nearly 15% year-to-date and lagging the S&P 500. Meta has guided 2026 AI capex to $115B-$135B, almost double last year's spend. The hoarded capacity includes a 2,250-acre hyperscale campus in Louisiana, a gigawatt-scale data center in the Midwest, and roughly 1.6GW of new capacity from Crusoe.

At Meta's May shareholder meeting, Zuckerberg said entering cloud computing was "definitely on the table," noting firms were approaching Meta almost every week to buy compute or model access.

Here's the chain: Llama 4 launched last year already facing accusations of benchmark inflation, underperforming Qwen and Claude in independent tests. In April, Meta rushed out closed-source Muse Spark to fill the gap, but it hasn't proven it can go head-to-head with OpenAI, Anthropic, or Google — meaning Meta's actual internal compute demand is running well below the capacity it spent two years stockpiling. The overhang keeps growing, so Meta is packaging bare-metal compute and hosted models to sell outsiders, competing directly with AWS, Azure, and Google Cloud, and squeezing neoclouds like CoreWeave (Nasdaq: CRWV). Translation: this selloff is pricing Meta's model problem into the entire storage and optical supply chain.

The template already exists: SpaceX's xAI is renting spare Memphis capacity to Anthropic, a deal Bloomberg Intelligence estimates could bring in over $50B by 2028 and $100B by 2030. Renting out excess compute is becoming standard operating procedure for AI infrastructure players, not a problem unique to one company.

Meta hasn't confirmed the Bloomberg report, and Reuters said it couldn't independently verify the details. If the leasing business never materializes, or every hyperscaler tries the same move at once and a real compute glut shows up, this selloff isn't a misread — it's pricing in a real risk early.

If the leasing model gets validated, Meta likely won't cut hardware spend. It would probably accelerate data center buildout to grab cloud market share, which turns into incremental orders for storage and chip suppliers as Meta scales up. Do you think this selloff gets proven wrong in three months, or is this the start of a real compute glut cycle?

Nvidia calls this new model "revenue-sharing and credit-support" — in plain terms, it's underwriting smaller clouds' compute business in exchange for usage-linked recurring revenue. First movers Sharon AI ($SHAZ) get 72MW of new capacity and up to 40,000 GB300 GPUs, taking total footprint to 132MW; Firmus is building a 360MW campus in Indonesia for up to 170,000 GPUs through 2034. $SHAZ popped 25% intraday on the news.

Trace the mechanism: Nvidia backstops unsold capacity → clouds borrow more easily against that guarantee → the new orders flow straight back onto Nvidia's own revenue line → the exposure lands on Nvidia's own balance sheet ($17.5B in disclosed private investments in fiscal 2026 alone). This is Nvidia using its own credit to manufacture some of its own demand.https://t.co/qpH06ogcXz

🚨BREAKING: $NVDA said on its blog it's partnering with AI cloud firms including Firmus and Sharon AI, using a revenue-share and credit-support model to deploy large-scale, multi-tenant AI factories that these clouds will resell as NVIDIA DSX-powered compute. You'd read this as another chip order. It's actually Nvidia turning itself from a GPU seller into the bank that underwrites its own buyers.

Hard numbers: Sharon AI ($SHAZ , Nasdaq) is adding 72MW of Nvidia-backed data center capacity, planning up to 40,000 GB300 GPUs, taking its total AI factory footprint to 132MW (102MW already contracted). Firmus is building a 360MW campus in Batam, Indonesia, scaling to as many as 170,000 GPUs, under a deal running through 2034. $SHAZ shares jumped as much as 25% intraday on the news.

Sharon AI co-founder and CEO James Manning called it a milestone for the company's sovereign AI compute strategy. Firmus co-CEO Tim Rosenfield said AI-native companies need scalable, efficient infrastructure to compete globally.

Trace the mechanism: Nvidia backs young clouds' unsold GPU capacity with revenue-share and buyback guarantees — the same structure behind its pledge to buy CoreWeave's unused capacity through 2032 ($6.3B) and its $1.5B chip leaseback with Lambda covering 18,000 GPUs → that backing works like a credit backstop, making it easier for these clouds to borrow and keep buying GPUs → the new demand flows straight back onto Nvidia's own revenue line → but the exposure piles up on Nvidia's own balance sheet too, with $17.5B in disclosed private-company investments and $3.5B in land/power guarantees in fiscal 2026 alone. Translation: some of Nvidia's order growth is demand it financed itself — booked as revenue while the risk sits on its own books.

Scale check: one Firmus campus alone is built for 170,000 GPUs, roughly the order-book equivalent of a mid-size country's entire data center industry. And a small-cap Australian cloud, Sharon AI, saw its market value pop 25% in a day purely on the strength of Nvidia's credit backing.

The skeptics aren't quiet either. Michael Burry, known for shorting subprime, has disclosed bearish bets against Nvidia and Tesla on AI-bubble concerns. Analysts have compared Nvidia's direct investment exposure — now above 60% of annual revenue — to Lucent's vendor-financing peak before the telecom bust, at a multiple of that ratio. Chip stocks broadly had a rough start too, with SK Hynix and Samsung both dropping more than 7% intraday.

Short term, this model does what it's built to do: get small clouds building faster and get more GPUs sold. But it also means Nvidia is using its own balance sheet to guarantee some of the demand it books as revenue.

Next time you see a headline about "expanded partnerships" or "surging orders," it's worth asking whether that's organic end demand or capacity Nvidia financed itself. Ecosystem-building, or one more layer of insurance on the next bubble? Let us know below.

Drop this SK Hynix leveraged-ETF mechanic into Bobby — see how it actually moves $7709.HK and $000660.KS, then make your own call.Objective reporting of facts. Not investment advice.

https://t.co/TJMQ1qHW81

SK Hynix's leveraged ETF has become the world's largest single-stock leveraged product. The $13 billion fund, HKEX-listed under $7709.HK, reached that scale in just nine months, and on volatile trading days its volume can equal two-thirds of SK Hynix's ($000660.KS, KRX) own turnover. You'd assume SK Hynix's near-100% rally this year is pure AI-order momentum. Actually this $13B leverage machine accelerates the stock on the way up, and it's built to do the same thing on the way down.

The ETF grew from a standing start to $13 billion against SK Hynix's own $1.2 trillion market cap, one of the most extreme ETF-to-underlying turnover ratios among large-cap leveraged products. SK Hynix and Samsung together make up 57% of the Kospi (28% and 29%), so their moves largely dictate the index. On June 23, the ETF plunged 23% in a single session. To replicate 2x exposure, banks buy downside protection from hedge funds through exotic "cliquet" derivatives, and the annualized cost of that protection has jumped from about 3% in March to over 10% — hedging one stock's downside now costs more than double.

Dean Curnutt, CEO of Macro Risk Advisors, argues SK Hynix alone won't drag down the S&P 500, but the same feedback loop that fueled the rally can work in reverse and trigger a very fast sell-off. Janus Henderson portfolio manager Jamie Sandells notes bank balance sheets are absorbing record-high equities, mega IPOs, and leveraged-ETF flow all at once.

Trace the chain: the ETF's growth to $13B in nine months forces banks to replicate 2x exposure via swaps and cliquets → hedging costs jump from 3% to 10%+, pushing some banks to trim exposure to SK Hynix-linked products and charge more → if the stock ever drops close to June 23's 23%, tighter liquidity turns selling into a feedback loop. Translation: part of SK Hynix's short-term price discovery has shifted from earnings fundamentals to leveraged-position rebalancing.

Every afternoon around 1:30pm Hong Kong time, a market-maker trader named Ian sits down at his desk to trade ahead of the ETF's rebalancing, then flattens the position before the close. He calls the money "too easy" — the hard part is timing it, since entering too early risks unexpected news and entering too late means fighting a crowded trade. For many professional traders, predicting this ETF's closing rebalance now matters almost as much as modeling SK Hynix's earnings.

Nothing here suggests the system is breaking. CSOP has simply warned that new ETF unit creation could pause if counterparties hit risk limits. In other words, the machine is still running — it's just getting more expensive to keep it running.

When one ETF can account for two-thirds of its underlying stock's turnover, a meaningful chunk of that volatility is being priced by $13 billion of leveraged positioning, not fundamentals alone. If this ETF drops 23% again in a single day, do you think banks pull back exposure first, or retail gets caught in the stampede first? Curious what you'd bet on.

Drop Nvidia's revenue-share and guarantee playbook into Bobby — see how it actually moves $NVDA, then make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/q5z2r00TqE

🚨BREAKING: $NVDA said on its blog it's partnering with AI cloud firms including Firmus and Sharon AI, using a revenue-share and credit-support model to deploy large-scale, multi-tenant AI factories that these clouds will resell as NVIDIA DSX-powered compute. You'd read this as another chip order. It's actually Nvidia turning itself from a GPU seller into the bank that underwrites its own buyers.

Hard numbers: Sharon AI ($SHAZ , Nasdaq) is adding 72MW of Nvidia-backed data center capacity, planning up to 40,000 GB300 GPUs, taking its total AI factory footprint to 132MW (102MW already contracted). Firmus is building a 360MW campus in Batam, Indonesia, scaling to as many as 170,000 GPUs, under a deal running through 2034. $SHAZ shares jumped as much as 25% intraday on the news.

Sharon AI co-founder and CEO James Manning called it a milestone for the company's sovereign AI compute strategy. Firmus co-CEO Tim Rosenfield said AI-native companies need scalable, efficient infrastructure to compete globally.

Trace the mechanism: Nvidia backs young clouds' unsold GPU capacity with revenue-share and buyback guarantees — the same structure behind its pledge to buy CoreWeave's unused capacity through 2032 ($6.3B) and its $1.5B chip leaseback with Lambda covering 18,000 GPUs → that backing works like a credit backstop, making it easier for these clouds to borrow and keep buying GPUs → the new demand flows straight back onto Nvidia's own revenue line → but the exposure piles up on Nvidia's own balance sheet too, with $17.5B in disclosed private-company investments and $3.5B in land/power guarantees in fiscal 2026 alone. Translation: some of Nvidia's order growth is demand it financed itself — booked as revenue while the risk sits on its own books.

Scale check: one Firmus campus alone is built for 170,000 GPUs, roughly the order-book equivalent of a mid-size country's entire data center industry. And a small-cap Australian cloud, Sharon AI, saw its market value pop 25% in a day purely on the strength of Nvidia's credit backing.

The skeptics aren't quiet either. Michael Burry, known for shorting subprime, has disclosed bearish bets against Nvidia and Tesla on AI-bubble concerns. Analysts have compared Nvidia's direct investment exposure — now above 60% of annual revenue — to Lucent's vendor-financing peak before the telecom bust, at a multiple of that ratio. Chip stocks broadly had a rough start too, with SK Hynix and Samsung both dropping more than 7% intraday.

Short term, this model does what it's built to do: get small clouds building faster and get more GPUs sold. But it also means Nvidia is using its own balance sheet to guarantee some of the demand it books as revenue.

Next time you see a headline about "expanded partnerships" or "surging orders," it's worth asking whether that's organic end demand or capacity Nvidia financed itself. Ecosystem-building, or one more layer of insurance on the next bubble? Let us know below.

Drop OpenAI's equity proposal into Bobby — see how it actually plays out for $GOOGL and $META, then make your own call.

Objective reporting of facts. Not investment advice.

https://t.co/lvE64JkiET

OpenAI has proposed donating a 5% stake to the U.S. government, worth roughly 42.6B at its current $852B valuation, in a bid to defuse mounting political pressure in Washington.

The framework reportedly envisions every leading U.S. AI developer handing 5% to a government vehicle: Google ( $GOOGL ), Meta ($META ) and even Anthropic get named, but right now OpenAI is the only one actually at the table.

The $42.6B stake costs the government nothing in cash: equity flows straight into what OpenAI calls a "Public Wealth Fund," a concept it first floated in an April policy paper. Compare that to Sen. Sanders' rival plan — a one-time 50% stock tax on OpenAI, Anthropic, xAI and others, plus board seats and veto power — and OpenAI's 5% offer looks less like generosity and more like a preemptive move to keep Congress from passing something far more aggressive.

Trace the chain:

① OpenAI trades 5% equity for political cover, easing the "AI only enriches a few" narrative ahead of its IPO.

② If it lands, OpenAI's cap table gets a new permanent shareholder: the U.S. government, and any IPO valuation model has to price in that governance risk premium.

③ Google and Meta get named as "potential" participants, but Anthropic is reportedly not even in these talks, which means "every AI giant pays up" is still a pitch, not policy.

④ The real inflection point is whether Congress ever legislates this framework onto already-public companies — at that stage it stops being a voluntary donation and becomes forced dilution, and boardrooms would respond very differently.

The pushback matters too: Sen. Warren has warned that once government holds equity, it's both regulator and shareholder, which can soften safety enforcement and plant the seeds for a "too big to fail" bailout logic. Add a Quinnipiac poll showing 55% of Americans think AI does more harm than good, and OpenAI's rush to hand over equity starts to look like reputational insurance as much as policy.

If this framework ever spreads from OpenAI to already-listed Google and Meta, do their boards vote yes — or does the whole thing never leave the "proposal" stage?

倒计时 3 天|AI Agent × 投资交易黑客松即将开始 🚀

3 Days to Go | AI Agent × Investment Trading Hackathon Starts Soon 🚀

FLOW AI 投资交易 Agent 黑客松,3 天后正式开启。

The FLOW AI Investment Trading Agent Hackathon kicks off in 3 days.

关注 AI Agent 却没场景验证?对量化交易、金融科技感兴趣却没机会动手?欢迎你来。

Been following AI Agents but no real scenario to test your ideas? Interested in quant trading and fintech but no chance to build? Join us.

这不是只讲概念的活动——从 idea 到策略设计、模型调用、数据处理,最终完成 Demo 展示。

This isn't a talk-only event — go from idea to strategy design, model integration, data processing, and a live Demo.

适合谁来:

Who should join:

→ AI / Agent / LLM 开发者

→ AI / Agent / LLM developers

→ 量化、交易、金融科技从业者

→ Quant, trading, and fintech professionals

→ 产品经理、设计师、创业者

→ PMs, designers, and founders

→ 对 AI + 投资交易感兴趣的学生和研究者

→ Students and researchers into AI + trading

→ 有想法,想快速做出原型的人

→ Anyone with an idea ready to prototype

报名持续开放。想把想法变成 Demo,现在加入。

Registration is open. Turn ideas into Demos — join now.