Strategy announces a Digital Credit Capital Framework designed to strengthen Digital Credit, enhance liquidity, preserve long-term Bitcoin exposure, and support long-term value creation. $MSTR $STRC https://t.co/AUoUCtem53

The wake up call is for you, Senator.

You have spent 30 years in government. Name one thing you built. One product, one service, one system that works. You can't. Your entire career consists of redistributing value created by others, and lecturing the people who create it.

Elon built reusable rockets for less than what Washington spends in 3 hours. The government you represent spends $7 trillion a year and can't balance a budget, fix a border, or build a train. He did 100 times more with 100 times less.

A trillionaire who earned it by serving billions of customers is not a problem. A bureaucrat who never created a dollar of value deciding how value should be allocated, that's the problem.

The era of the builder is here. You can keep tweeting from the back seat of your government car, or you can step aside and watch.

History remembers the people who build. It footnotes the ones who taxed them.

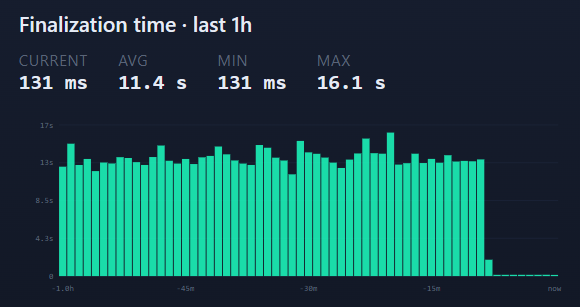

HUGE: SOLANA JUST ACHIEVED 100X FASTER FINALITY

Anza’s first successful Alpenglow “Alpenswitch” cut finalization from ~12.8 seconds to ~100–150ms

That’s Visa-level speed on a public blockchain! solana:So11111111111111111111111111111111111111112 🤯

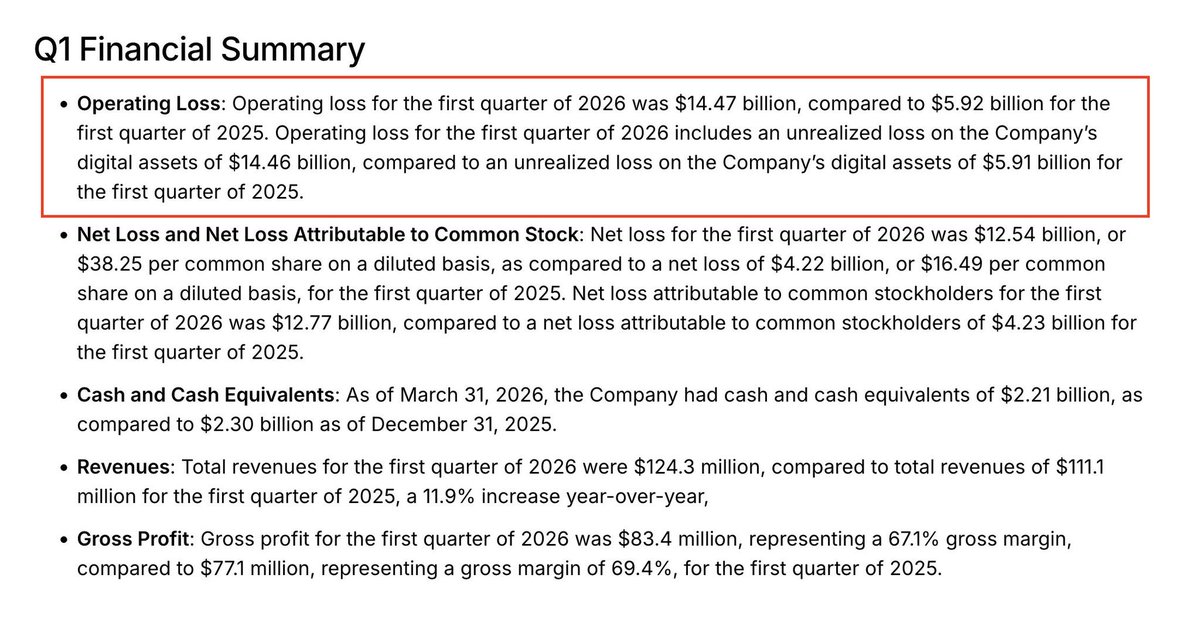

Strategy just reported a $14.47 billion operating loss for the first quarter of 2026. Its quarterly revenue was $124.3 million. The loss was 116 times the revenue. The stock closed up 1.69% on earnings day.

It is difficult to find a precedent in American corporate history for a company reporting an operating loss 116 times its revenue and seeing its share price rise on the same day. The reason is not irrational exuberance. It is that the loss is an accounting entry required by ASU 2023-08, which mandates Bitcoin be marked to fair value every quarter with unrealized changes flowing through the income statement. Bitcoin fell approximately 23% in Q1. Strategy held 762,099 coins at quarter end. The mark-to-market produced $14.46 billion in unrealized losses. No coin was sold. The software business grew 11.9% with a 67.1% gross margin.

The loss is the size of a mid-cap bank failure. The business underneath is growing.

On the same release, Strategy disclosed it now holds 818,334 BTC as of May 3, having acquired 63,410 coins year to date at a cost of $11.68 billion raised through ATM offerings of common stock and STRC perpetual preferred. BTC Yield, the company’s custom metric measuring per-share Bitcoin accretion on a fully diluted basis, stands at 9.4% year to date. The company’s average cost per coin is $75,537 against a current market price near $80,800, placing the entire treasury approximately $2.3 billion above water. Cash on the balance sheet: $2.21 billion. Total preferred claims stand at $13.54 billion with an annualized dividend run-rate of approximately $1.55 billion, giving the company roughly seventeen months of cash coverage before further raises or Bitcoin sales become necessary.

Here is what the earnings release does not say but the mechanism implies.

In February, Micheal Saylor told CNBC that concerns about forced Bitcoin sales are “unfounded” and that Strategy holds “50 years worth of dividends in bitcoin.” On the May 5 earnings call, per multiple accounts citing the exchange, Saylor stated: “You buy Bitcoin with credit, you let it appreciate, and then you sell Bitcoin to pay the dividend.” The shift from “never sell” to explicit willingness to harvest is the most consequential narrative evolution in Strategy’s history. It means the 818,334-coin treasury is no longer a pure HODL position. It is a carry trade: long Bitcoin volatility, funded by equity holders accepting BTC beta as yield, with a preferred layer extracting 11.5% annually from the same pool.

The company’s own filed disclaimers state that BTC Yield “may overstate the incremental value accretion” and “does not take into account the preferential rights of the Company’s preferred stockholders to dividends and the Company’s assets in a liquidation.” Preferred claims now total $13.54 billion, ranking senior to common equity on the identical 818,334 coins.

Strategy is no longer a Bitcoin holding company. It is a Bitcoin bank without a license. It borrows at 11.5% via preferred, deploys into a single volatile asset, marks gains via a custom metric excluding borrowing costs, and now signals willingness to liquidate holdings to service depositors. Every bank that operated this model eventually faced a maturity mismatch. Strategy’s version has no maturity because STRC is perpetual. That is either the innovation or the trap.

The $14.47 billion loss told you nothing about the company. The shift from “never sell” to “structured harvesting” told you everything.

https://t.co/FRwSI1w8WU

$MSTR

“NOTHING WOULD MAKE ME HAPPIER THAN TO RIP THE FACES OF ALL THE SKEPTICS AND THE SHORTS AND DRIVE $MSTR TO THE MOON” - Saylor

I love this company.

$BTC $MSTR $STRC

solana ($SOL) is shipping a 700x capacity upgrade and the market is pricing it like a shitter chain at 2.5-year lows on SOL/BTC. firedancer targets 1m TPS vs current 1,300 TPS production. live on testnet. $1m audit bounty open. full release 2026. alpenglow already shipped sub-200ms finality on mainnet in Q1. validator costs dropped 98% from $60k/year to $1k/year. $1.1t in on-chain economic activity last quarter. $832b stablecoin volume. 99% tokenized equities market share. JPMorgan, B2C2, SoFi, Western Union all chose solana for settlement infrastructure. 416 new projects added in Q1, most of any chain. shitter volume share dropped from 70% to 20% and the builders kept building. the meme tourists left. the infrastructure stayed. 12-18 month accumulation play at a 71% discount from ATH

@ThatARCGuy 50 runs and still happily opening cointainers, breaching doors, killing arcs for trials. Its a winddown after a longday at work. See u topside

THREAD: The number that’s about to break Wall Street. $STRC and a sharp ratio: 10-24

1/

$STRC is printing a Sharpe Ratio that doesn’t exist in the history of capital markets.

Let me explain why every portfolio manager on Earth should be paying attention.

2/

First. What is a Sharpe Ratio?

It answers one question:

“How much return am I getting for every unit of risk I’m taking?”

It’s the universal scorecard of institutional finance.

Hedge funds live and die by it.

Pension funds won’t allocate without it.

It’s the one number that cuts through all the noise.

3/

Here’s how the scores break down in the real world:

🔴 Below 1.0 — Poor

🟡 1.0–2.0 — Acceptable

🟢 2.0–3.0 — Very Good

💎 3.0–5.0 — Exceptional. Rare.

👻 5.0–10.0 — Almost never seen

☠️ 10.0+ — Doesn’t exist in recorded history

For context — Warren Buffett’s lifetime Sharpe ratio is roughly 0.76.

4/

$STRC right now:

📌 Price: $100.00

📌 Yield: 11.50%

📌 30D Volatility: 2.0%

📌 30D Sharpe: 3.92

Already exceptional.

Already historically rare.

Already making fixed income desks uncomfortable.

But we’re just getting started.

5/

Here’s where it gets interesting.

Preferred securities are designed to trade near par.

If $STRC trades in a $99.97–$100.00 range— daily volatility drops to 2–3 basis points.

Run the math:

5 bps- sharp of 10

3bps- sharp of 16

2bps - sharp of 24

A Sharpe of 16–24. (That’s not a typo).

6/

Let that sink in.

The greatest investors in history spent entire careers trying to crack a Sharpe of 3.

$STRC — a Bitcoin-adjacent preferred stock — could print 5x to 8x that.

Not through leverage.

Not through accounting tricks.

Through a Bitcoin treasury strategy Wall Street spent 16 years calling rat poison.

7/

What happens when a 10+ Sharpe asset enters the market?

Every quant model gets forced to reallocate.

Not as a choice.

As a mathematical conclusion.

Risk-parity funds. Pension algorithms. Institutional mandates.

They don’t debate Sharpe ratios. They follow them.

8/

It gets worse for TradFi.

Right now portfolio managers risk their careers by buying Bitcoin-adjacent assets.

At a 10+ Sharpe?

They risk their careers by not buying it.

The entire institutional incentive structure flips overnight.

9/

The 60/40 portfolio.

Built to optimize risk-adjusted returns.

Taught in every MBA program.

Trusted by trillions in pension capital.

A 10+ Sharpe asset doesn’t compete with the 60/40 model.

It makes it look criminally negligent.

10/

Some CFA right now is staring at his Bloomberg terminal like it just started speaking Aramaic.

He spent 20 years memorizing bond ladders, duration math, and the sacred liturgy of modern portfolio theory.

Just to watch a Bitcoin preferred security print numbers his models say are impossible.

11/

The Sharpe Ratio is the language Wall Street trusts above all others.

It cuts through narrative. Through hype. Through opinion.

It’s pure math.

And the math is saying something Wall Street isn’t ready to hear.

12/

If $STRC sustains a Sharpe above 10 — even for a quarter —

It won’t just turn heads.

It will force the largest reallocation of institutional capital in a generation.

Not because Bitcoiners said so.

Because the math said so.

13/

$STRC has soaked up over 5k of Bitcoin so far today and we still have an hour left of trading. Imagine a year or two from now when every portfolio manager is forced to buy $STRC. currently it’s less than a year old and 99.99% of the world has never even heard of $strc. Let that sink in.

14/

If you read this far and you’re as obsessed with Bitcoin as I am, consider checking out our new company — Bitcoin Strategy Group — inspired by Michael @saylor himself.

Our mission is simple: educating the world on Bitcoin through the power of storytelling.

If you’d like to share your personal Bitcoin story or experience about how @saylor has impacted your life or way of thinking and have it published in our book “This Is Why We Bitcoin” visit our website and submit Bitcoin or Saylor story!

https://t.co/FzM2rypMF2

$STRC explodes—10.6M shares above threshold for ~7,130 BTC estimated.

Largest single-day haul ever. Volume at 458% of avg, every share crossing threshold. That's more than the entire previous week combined.

Yield at 11.50%.

https://t.co/lVNalzUMK3