BREAKING: SpaceX's IPO is expected to create 4,000 new millionaires, including some cafeteria workers whose compensation packages include employee stock options, per Bloomberg.

$LITE Management Speech from Mizuho Technology at today’s conference.

The company expects to start shipping CPO scale up optical products in the second half of 2027.

With formal ramp up in 2028.

No delays, as this aligns with previous timelines shared.

So today, we also got confirmation from

$NVDA SVP no delays on CPO scale out timelines H2 2026, and they’re beginning mass production.

And $LITE management also stated no delays on CPO scale up timeline.

The leading companies in Nvidia and Lumentum probably know their own timelines the better than incorrect analyst reports telling them no.

And both are incredibly bullish on TAM and opportunities.

TrendForce: Thanks to agentic AI, global DRAM market revenue is expected to grow 303% YoY in 2026 and 46% YoY in 2027.

Likewise, global NAND flash market revenue is expected to grow 208.7% in 2026 and 40.2% in 2027.

This is a really remarkable report from UBS.

I was genuinely stunned by a lot of it.

In particular, the point that Kioxia's NAND wafer cost is $2,000 — only half of Samsung's — and that Kioxia's lateral (horizontal) scaling architecture is what gives the company its industry-leading cost advantage was something I really had no idea about.

There's so much else in there too — HBF, the outlook for the NAND flash market itself, and more.

McKinsey humanoid supply chain mapping:

Confirms that Actuators are set to be the key battleground for mass production.

Coupled with BofA analysis where Actuators = 51% total BOM.

A few companies have overlap in different Actuator parts like:

-> Harmonic Drive Systems (6324)

-> Nabtesco Corp (6268)

-> THK (6481)

-> Schaeffler

I'm close to picking 1-2 names for exposure.

HDS are the glaringly obvious pick though, purely from a supply chain overlap POV.

I wasn’t planning to share this, but it’s such a high-quality explanation of CPO that I have to.

Just watch it. You’ll regret it if you don’t.

https://t.co/Z5M3TvHH2B

Morgan Stanley recently published a bottom-up model on hyperscaler datacenter CAPEX spending.

A 1GW NVDA Vera Rubin datacenter costs $41bn. A 1GW Trainium3 cluster costs $15bn.

The Powered Shell sits at 6-14% of every build.

That is $2-6bn per GW.

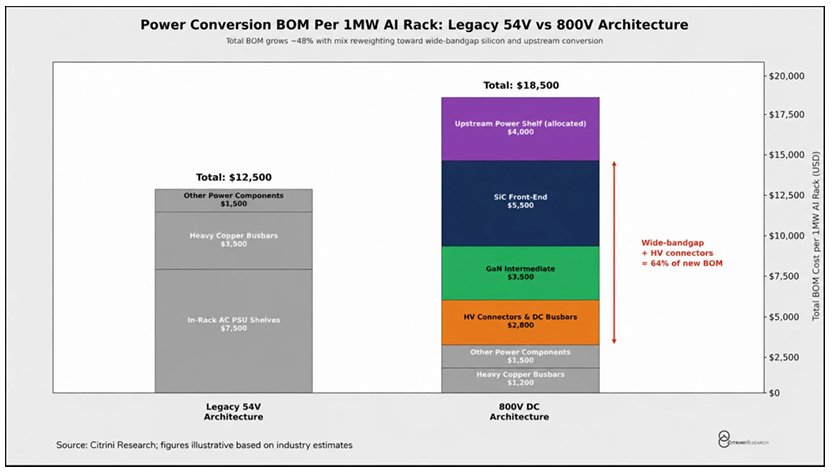

This is the power semis opportunity.

Here is a list of stocks that benefit the most in each generation:

Current Gen - Silicon Power Delivery

$MPWR – The rack power incumbent. Monolithic has accumulated design wins across the Blackwell generation for DC-DC conversion. Higher switching frequencies mean less copper, less heat, more density. 800V datacenter samples already out, but the bigger revenue ramp lands in 2027.

$VICR – Factorized Power Architecture pure-play. Products are concentrated in the datacenter and hyperscaler segments for power delivery on server motherboards and inside racks. Working toward delivery of a next-gen high-density VPD system for a lead AI customer. Underowned relative to how architecturally embedded it actually is.

$POWI – The GaN entry point. PowiGaN technology is being developed directly with NVIDIA for the 800 VDC architecture transition. Industry-first 1250V GaN switches achieve greater than 98% efficiency, outperforming both stacked 650V GaN and 1200V SiC alternatives.

Confirmed NVIDIA collaboration.

Next gen - Wide Bandgap Semiconductors (2026 to 2028)

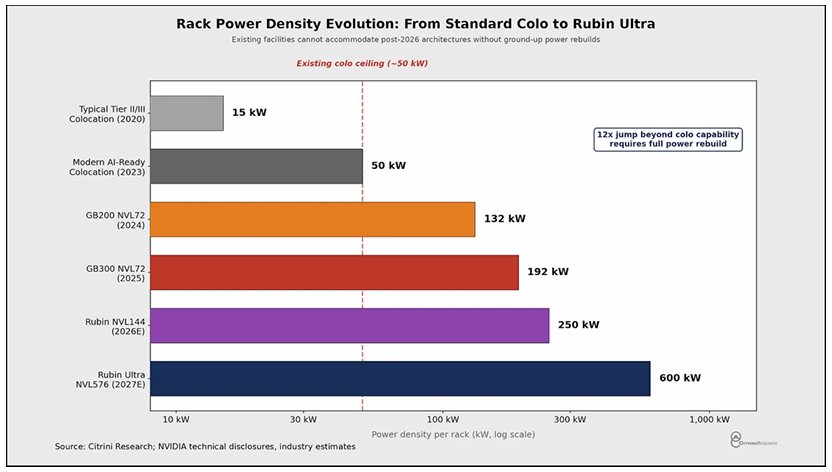

When rack power hits 100kW and beyond, silicon hits its switching wall. GaN and SiC move in.

$NVTS – The GaN pure-play. Confirmed NVIDIA collaboration on 800V HVDC architecture for Kyber rack-scale systems powering Rubin Ultra. GaNFast and GeneSiC platforms cover both AC-DC and DC-DC conversion layers. Strongest confirmed design win of the group.

$AOSL – The GaN challenger. Also collaborating directly with NVIDIA on 800 VDC architecture, covering SiC for high-voltage conversion and GaN FETs for high-density DC-DC conversion inside the rack. Smaller cap, higher beta to design win acceleration.

$WOLF – Post-bankruptcy optionality. Emerged from Chapter 11 in September 2025 with debt cut 70% and interest expense cut 60%. Now targeting AI datacenters alongside EVs and aerospace as the next growth vector. Highest beta to SiC datacenter adoption if the thesis plays out, but revenue confirmation is still ahead.

Test infrastructure

$AEHR – Wafer-level burn-in leader for SiC, GaN, and silicon photonics. The only name that sits on both the power and photonics layers. Expanding into AI processors and GaN production orders with improved visibility into H2 fiscal 2026. Scales with every new wide bandgap production ramp regardless of who wins the platform battle.

Disclosure: I own $NVTS $AEHR on this layer.

Bullish Power Semis

Thread: Korea’s Memory Exports, May 1–20

1. DRAM

DRAM, including modules: export value of $11,527mn, +498% Y/Y, +27% M/M

The DRAM export unit price, including modules, reached $60,319/kg, up 5% from April 20, 2026, and up 432% Y/Y.

New TIL: I figured out how to use my LLM CLI tool in a shebang line, which means you can write executable scripts in English, or hook up more complex scripts with a snippet of YAML template