We pulled off a coup when we got 3 of the sharpest minds in the mutual fund industry to meet our clients in Pune for our Annual Investor Conclave.

The lucid @AashishPS, the calibrated @hktg13 & the incisive @SahilKapoor.

One stage. 3 experts and 150+ investors in the room. Our clients had heard a lot of noise over the past 15 months and were wondering how to tackle this uncertain environment.

One evening sorted that out.

No fluff. No jargon. Just three experts sharing their perspectives on navigating markets with clarity and discipline.

Beyond the insights, the evening fostered meaningful conversations and stronger relationships.

Grateful to our special guests for making the trip. 🙏

Every client who gave us their Saturday evening — thank you. It means a lot. 😇

And the Aksha team? Wonderful execution. Proud of you all. 👍

1/ Look at this viral post. The investor has been in the market since mid-2021 (nearly 5 years as of April 2026).

Invested: ₹17.62 Lakh

Returns: ~5.73% (Absolute)

The Complaint: "Mutual funds are a scam."

But the problem isn't the fund. It's the MWRR vs. TWRR gap. Let’s break it down. 👇

The "Silent Dashboard" of DIY platforms is failing investors. 📱🤫

AMFI data shows a massive jump in SIP stoppages (100%+) this March. Without a guide, market corrections lead to emotional exits.

At Moneyworks4u, our 1-to-1 reviews and proactive education keep stoppage for Q4 at 3% of SIP book. Out team acted as an emotional anchor and as a gatekeeper against emotional decisions for our clients.

Stop being a "transaction." Become a "relationship."

Most people invest… but very few understand what they’re doing.

Markets, investments, or money behavior — ask me anything 👇

No question is too basic or too complex. I’ll pick the top 20 questions and answer them in detail on YouTube.

🎥 Video link will be shared by here — stay tuned.

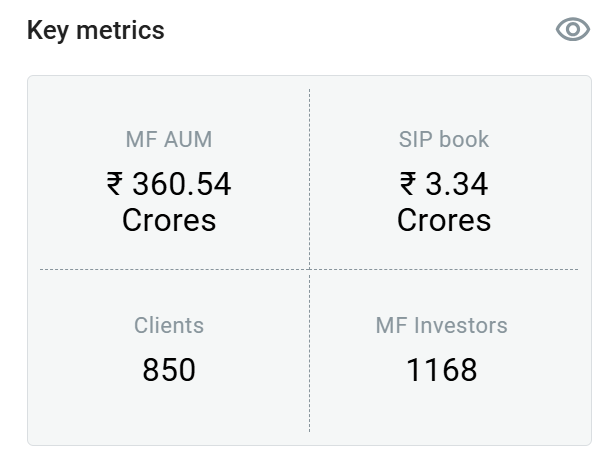

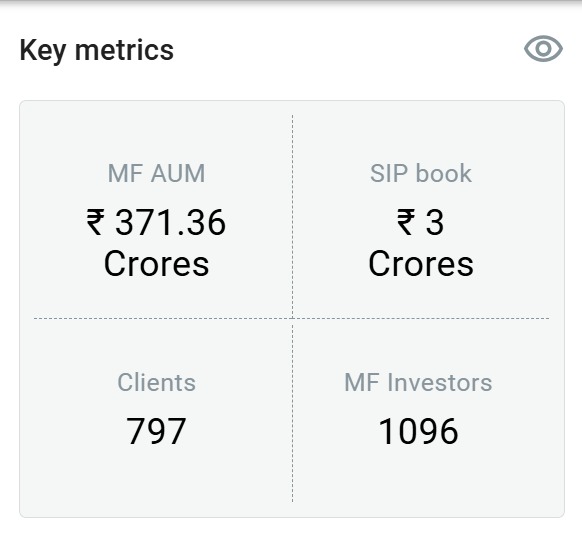

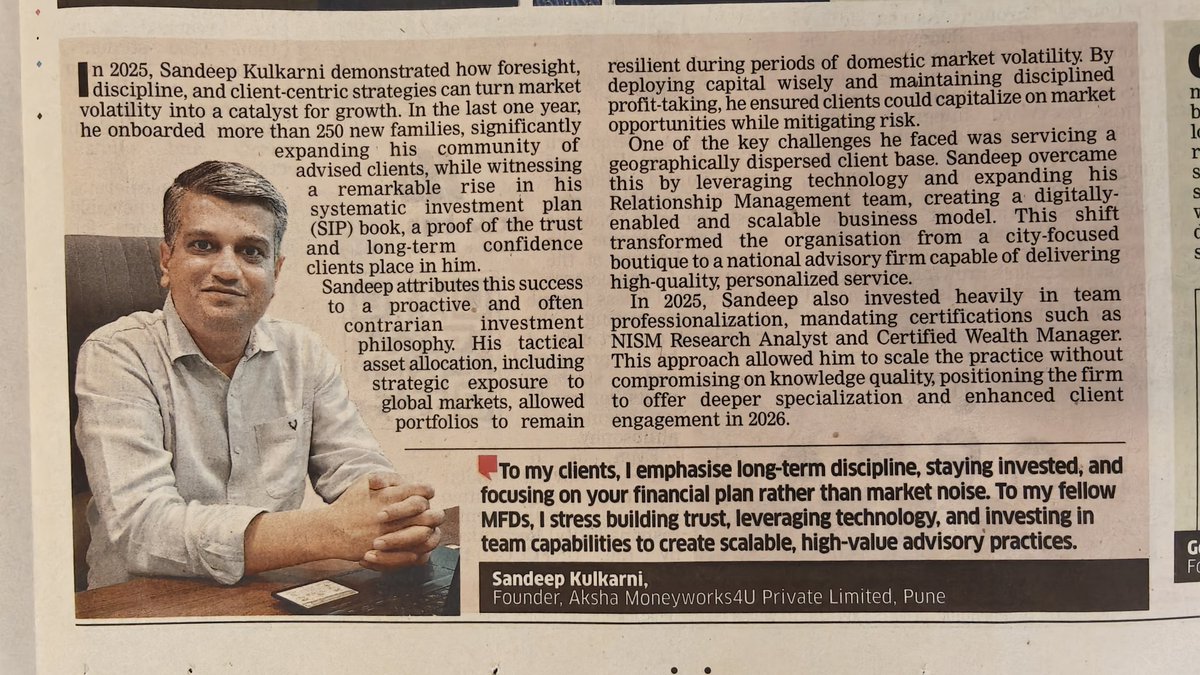

We had yet another phenomenal year at Aksha Moneyworks4u. Our AUM grew by 38%, the SIP book group grew by 1.53 Crs & we got 104 Crs of net new inflow in a challenging year like FY 25-26. We added 170+ new families and over 150+ family members of existing clients.

The Aksha Moneyworks4u team is also shaping up well as they pursue professional certifications and gain invaluable experience in managing client relationships across market cycle. We recently hired an experienced Research Analyst to deepen the quality of our investment thinking.

We are grateful to our clients for putting their trust in us in such a difficult year and for being our brand ambassador while referring us to their friends and family.

@SD_7242@_RAJAT_2@PKoltepatil@sanketr_7121@Aditya_Tilekar_@kakbhushundii

They say "Time in the market beats timing the market." Usually, they’re right. But when the Smallcap index goes sideways for 2 years, tactical allocation becomes the ultimate superpower.

Here’s how we ensured our clients are poised to make beat the market over the medium term with less stress. 👇

In Feb 2024, we reduced mid/smallcap exposure by half. We didn't sit in cash. We rotated into:

Arbitrage & BAFs

Gold Mining & US Value

China & Banking/Financials

The result? While smallcaps stayed flat, the "parked" capital kept working.

The Math: By avoiding the drawdown and reinvesting lower, a hypothetical 60% recovery in smallcaps over the next 3 yrs leads to a 13.8% CAGR vs. 9.8% for Buy & Hold. That’s a 30% excess return over 5 years—all while sleeping better at night.

The kicker? That 6% total portfolio alpha covers roughly 7 years of management fees. Good advice doesn't just grow wealth; it pays for itself by managing the "volatility tax" most investors pay blindly. 📈

Fill up the enquiry form to setup an meeting with us

https://t.co/bVieUu6rhs

What a year 2025 has been! It was the year of "the pivot." We started by aggressively buying the correction and trusting our gut on the Indian equity markets when the sentiment was low. Aside from selling gold a bit too soon (my biggest lesson this year!), it felt like we had the Midas touch.

The growth metrics reflect the deep trust our clients place in us:

AUM Growth: 57% (vs. an industry average of 17%).

Inflows: ₹100 Cr+ in new capital.

Scale: Our client base expanded by 33%, and our SIP book nearly doubled.

Interestingly, most of our new growth came from DIY investors seeking professional management as their portfolios grew in complexity or their professional lives grew more demanding.

Between travelling across India to meet the new and old clients, moving into our beautiful new office, and being featured in The Economic Times, it’s been a whirlwind. I’m incredibly proud of my team—we’ve upskilled, evolved, and worked harder than ever.

The only thing that didn’t grow? My fitness levels! 😅 With all energy poured into the business, personal goals took a backseat. As I look back, I’m just deeply grateful. We are no longer just a local firm; we are a national team ready for what’s next.

YouTube advise v/s Hiring an Advisor: What is the difference?

👉Good Financial Advice is personal not a generic broadcast. It takes into account many things including client's financial situation, financial goals and his temperament.

👉Good financial advice is not one time portfolio suggestion: it's an ongoing engagement.

Good financial advice involves being an emotional anchor for clients at market extremes.

An Advisor needs to be available to talk/chat when client wants to discuss anything.

👉Good financial advice involves cutting the market noise and making sense of prevailing market situation.

👉Value of financial advise should not be measured only in money saved but also in time saved by handing over the market tracking/portfolio tracking to the advisor. A 30 mins saved every day can be priceless for a busy working professional.

👉Often the content on social media is curated to your 'tastes'. So, you it is designed to feed your confirmation bias. Good financial advice entails showing you the mirror and having some hard conversations that can help the clients in the long run.

I feel we are making too much noise about expense ratio. The mistakes people make in going DIY cost them way more than the fees for hiring an advisor.

My gut feel from meeting 100s of MFDs/RIAs in the last 12 yrs is that 80% of MFDs/RIAs do a good job. 20% maybe be indulging in ethical practices. Its for you to find out who is a good financial advisor. Refrences from your friends and family are a good source to scout for trust worthy advisors.

Baki apka paisa, apki marzi! 🤗

Active v/s Passive: Where should you invest?

If you are an investor, you have to flip the question from

How many funds beat the index?

to

Which fund beats the index consistently over a 3/5 yrs time frame?

You can use rolling returns analysis to determine which fund consistently outperforms the index. Any fund that has outperformed the index for more than 70% of the time over 3/5 yrs t/f is a good fund imho.

I had spoken about it in my podcast with Groww. Check it out.

https://t.co/qKGrzE7x8i

Hello Dlliwalo👋

We are doing an Investor meet in Green Park, Delhi on Sunday, 21st Sept. Kindly fill up the Google form to register your attendance.

https://t.co/tAq1LVNFVq

Please RT & share it with your friends who may be interested in attending.

Hello Bengaluru!

We are coming to meet mutual fund investors in Bengaluru on Saturday, 7th June. The agenda is to showcase our portfolio creation framework and how it has helped our clients generate good risk-adjusted returns, share my perspective to look at the markets and we will share our favorite theme for the next 3 yrs.

Kindly register your attendance by filling up the registration form. 👇

https://t.co/ctOhppcQF3

Please RT for wider reach & share it with any of your friends who may be interested in joining.

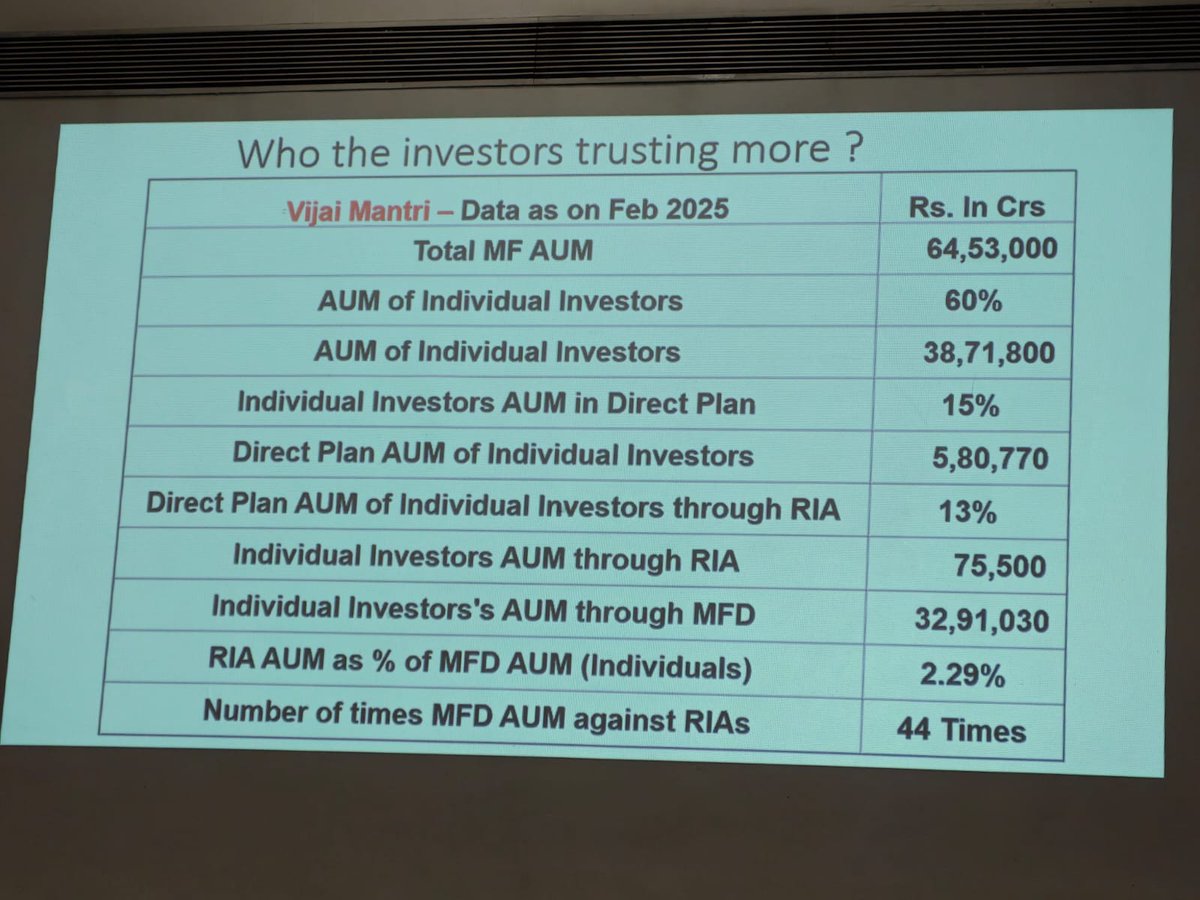

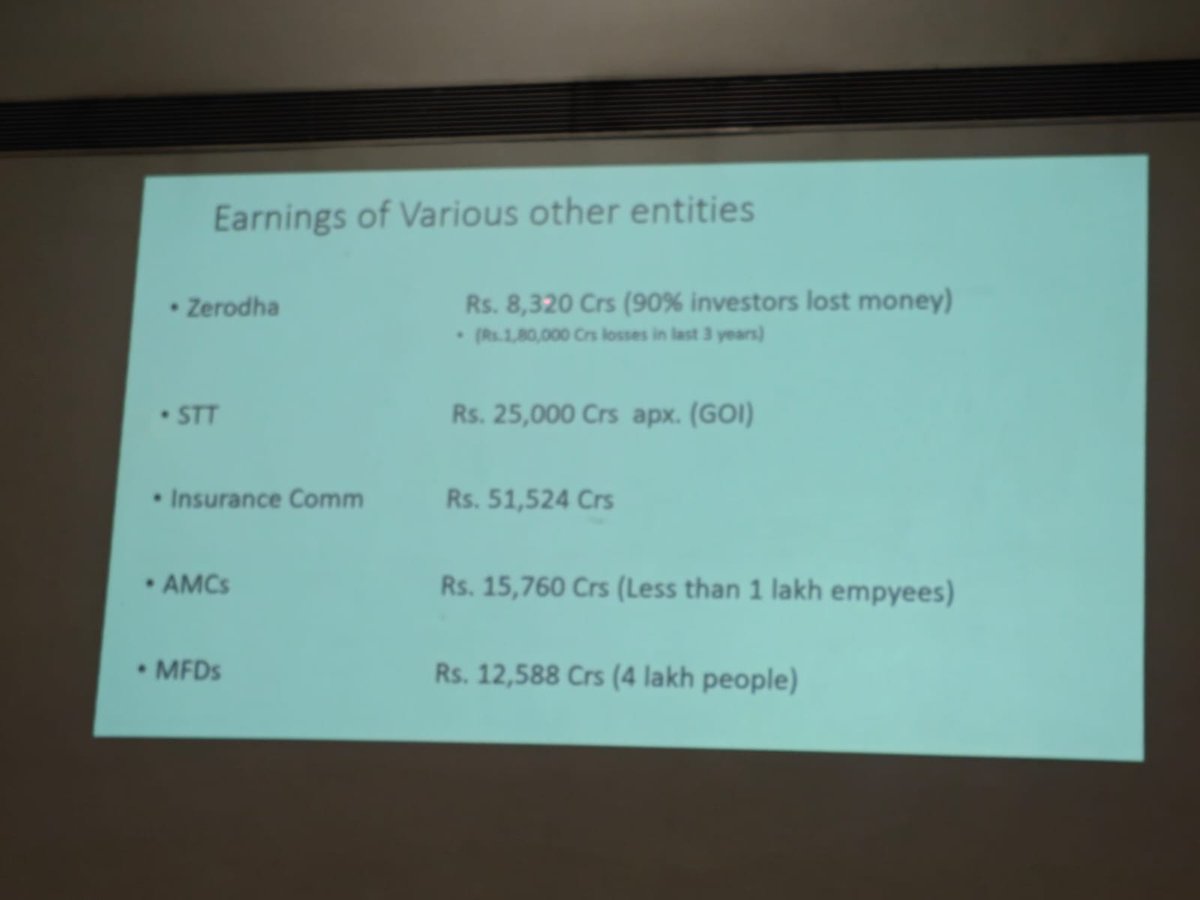

Got these slides from an industry friend.

No one blames zerodha, govt taxes or insurance agents.

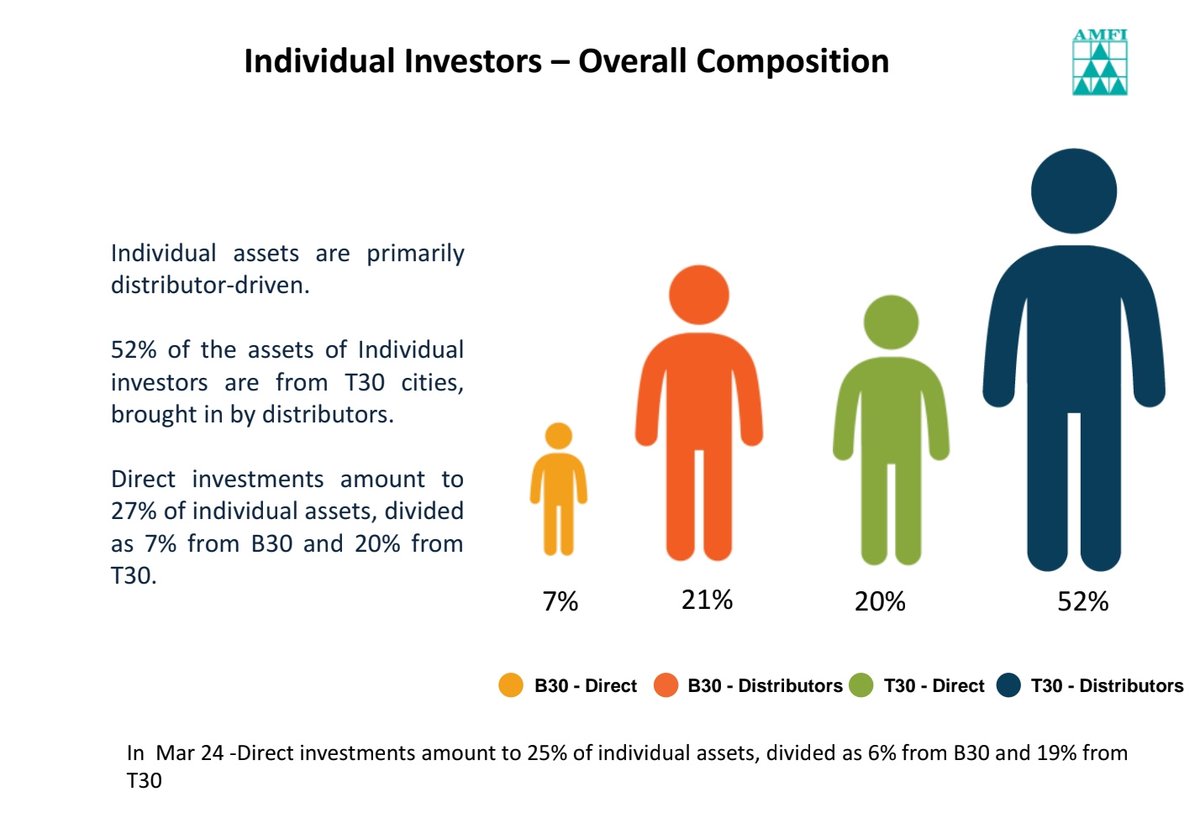

85% of individual AUM is invest via an MFDs/NDs/Banks and another 2% is via RIAs. So only 13% of individual AUM is in direct. If we remove debt funds I believe more than 90% of the AUM will be via intermediaries.

Of the 13% direct plan clients many are now seeking advice as they get busy with their jobs or their portfolios become too big to handle without emotional biases.

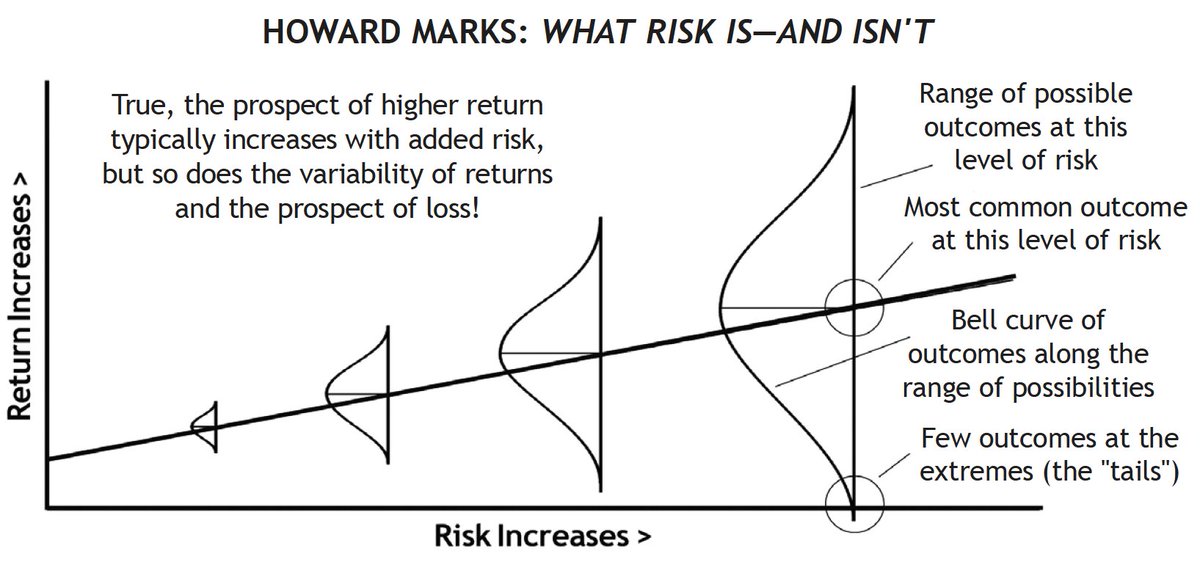

Concentrated portfolios are risky because the range of returns is wide. If things go well, you make a killing. If things go bad you underperform in a significant way.

This was the first time I asked people to build their portfolios with me. The message is still relevant as many of our calls have been 🎯

If you are interested in availing our services as a mutual fund distributor please fill up this Google form.

https://t.co/qdD1G2XC73

Baseless statement.

Market share of MFD in MF AUM has actually improved in last 10 yrs. 74% of Individual money is invested in regular plans. Even in the rest of the 26% there will be money routed through RIAs and large family offices portfolios. Banks & National distributors have lost market share in the last 10 yrs. Market Share of direct plan for equity/hybrid segment is not growing as some would want you to believe. If we add PMS/AIF to the equation the MFD market share is even higher.

Most of the direct plan AUM is either Corporate treasury money or retail money via Fintech platforms. Very smallcap fraction of HNIs would have a large direct portfolio.

People have to go to Fintech platform because there aren't too many MFDs out there and it really is not feasible to manage a very large number of retail investor book because profit margins are wafer thin.

Sure there are MFDs who may be indulging in mis-selling. But to make a broad brush statement about 1000s of MFDs spread across India is not fair.

Many studies in India(Axis MF) and in USA(Dalbar) have highlighted that investor returns are much lower than fund returns because of the Behaviour Gap.

In the past yrs we have onboarded a few hundred DIY clients.

Most of these investors started off as DIY, but when the portfolios became too big or when the job roles became demanding they decided to give up control to us.

I know a few other MFDs who have also onboarded many DIY investors.

Instead of painting things in black and white, why don't we talk about red flags and green flags to see in a MFD?

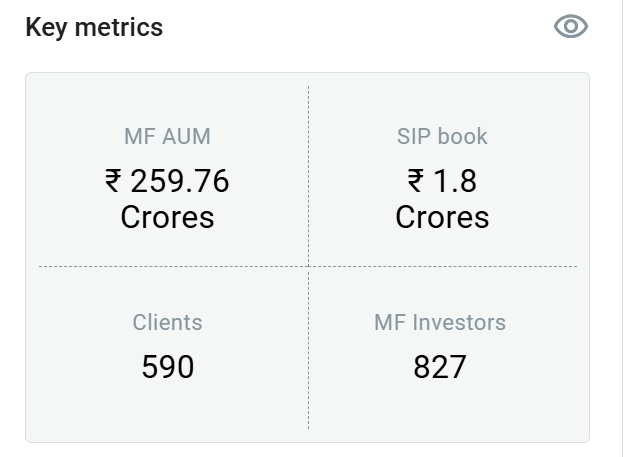

We have had a huge influx of new clients in this quarter. We onboarded 52 new families in the last 3 months. Almost all of these clients were DIY investors. We invested 29 Crs of new money in equity MFs in the last 10 weeks.

We are now one of the fastest growing mid-size boutique wealth mgmt outfits in India with MF AUM growing by 2.5x in last 2 yrs.