A proud milestone for Team Aksha Moneyworks4u.

All 4 of our experienced Relationship Managers are now Chartered Wealth Managers.

Our growing RM credentials:

Snehdeep Chalak — CWM| NISM XV (Research Analyst) | QPFP |

Prathamesh Dhawade — CWM | QPFP |

Prathmesh Kolte — CWM | QPFP |

Sanket Rathod — CWM | NISM XV | CFA L1 candidate.

This was not an individual race. The team studied together, shared resources, followed up with one another and ensured that everyone kept progressing.

Certifications alone do not make someone a great relationship manager. But they build credentials, strengthen the foundation and give young RMs the knowledge required to learn, practise and eventually develop real expertise.

At Aksha Moneyworks4u, we are trying to move from a solar system, where everything revolves around one founder, to a galaxy of stars—multiple capable RMs with their own knowledge, judgment, credibility and client relationships.

The journey is still long, but the foundation is getting stronger.

@SD_7242@_RAJAT_2@PKoltepatil@sanketr_7121

Rethinking Retirement

Most people view “retirement” as a sharp break – working full-time one day, then suddenly doing nothing the next. This outdated mindset is flawed and often leads to problems later in life, leaving people disconnected and purposeless.

Instead, it is far better to think of retirement as a gradual shift.

Image source (Kevin Dahlstrom’s tweet)

Early in life, work dominates out of necessity, driving how you spend your time and shaping your identity.

But this approach has serious downsides:

1 - Work’s Fading Appeal – Work loses its shine over time. When people say “I love my work,” they often mean it’s all they have. There’s more to life than another milestone or deal.

2 - Health Demands Time – As you age, prioritising health becomes critical to maintain high performance in all areas.

3 - One-Dimensional Limits Growth – A one-dimensional life limits your chance to explore passions while you’re still young. You need space for those to grow.

This pattern is seen repeatedly among “successful” people with wealth and status, but sadly, with hollow lives. It’s more common than you’d think, and it’s a warning sign.

Ideally, the goal should be to slowly gain (back) control over your time and build a multi-faceted identity.

Here’s the key: this won’t happen without intentional effort. It requires deliberate action.

Life unfolds in seasons. There’s a time for grinding, but always with the end in mind. Plant seeds for what’s next, ensuring you’re not left empty when work’s grip loosens.

Dr. Howard Tucker, a neurologist, is the world’s oldest practising doctor at 102. He attributes his longevity to staying mentally and physically active, warning that idleness kills. He once said, “Retirement is the real enemy of longevity. If you stop working, learning, moving… It’s like telling your body and mind they’re obsolete.”

He still walks five kilometres a day, keeps learning, and got his law degree at a ripe ‘young’ age of 67. At his age, many people are just waiting for life to pass by. But he keeps studying, walking, and working. Not out of duty, but out of conviction. Because nothing is more dangerous than standing still. Even the heart rusts if you don’t use it. Tucker emphasizes that remaining engaged - whether through work or meaningful activities—keeps the mind sharp and body resilient, a lesson he learned from his own experience and from his father, who practised medicine into his late 80s.

His advice: Don’t retire from life. Retire from inaction.

And as Kevin Dahlstrom (@Camp4) tweeted recently - Retirement is a trap. The end goal of a career is not to suddenly stop working & live a life of leisure. Humans NEED the stimulation & fulfilment that comes from challenging work.

I will digress a bit here, given my profession as an investment advisor. A long life is good and desirable, but we also need to ensure that we don’t run out of money before running out of years! You don’t want to be old and without money. Isn't it?

So please do read the following (financially) contextual articles I have written over the years about this:

The real edge in investing is increasingly shifting from access to information → access to high-quality people and conversations.

At Aksha Inner Circle, we had entrepreneurs, HNIs, senior professionals, along with Harsha Upadhyaya, CIO, Kotak Mutual Fund and his analyst team, for a candid discussion on markets, behaviour, AI disruption, capital allocation(India vs Global), and India’s long-term opportunity.

No noise.

No sensationalism.

Just thoughtful dialogue in a room full of serious people.

Special thanks to @sachinamusood, Zonal Head at Kotak Mutual Fund, for bringing together Harsha and the Kotak Mutual Fund team for this interaction.

Grateful to everyone who traveled in from across the country to be part of it.

People ask what's the edge of an MFD in an AI age.

A few things stand out:

1) MFDs who read widely across topics: markets, history, psychology, business — will have a natural edge. The role itself helps: you meet people from all sectors, all age groups, all walks of life. Every client interaction is a lesson, if you're paying attention.

2) Those who learn from the masters but execute via their own frameworks will outlast those who simply follow. The purpose of learning isn't to become a better follower. It's to become an independent thinker.

3) Cultivating genuine curiosity, not just about markets, but about people and ideas is what separates an advisor worth talking to from one who forwards research PDFs. AI will handle execution.

The MFD who brings original thinking, a distinct point of view, and the courage to occasionally disagree with the popular narrative that's who clients will seek out. Intelligence is no longer scarce. Independently generated intent is.

Easy to mock mutual fund distributors time and again. Much harder to acknowledge the role they have played in financially educating and bringing crores of first time investors into formal savings and capital markets.

India did not build a Rs 70 lakh crore mutual fund industry only through apps and fancy “global allocation” podcasts.

It was built ground up by thousands of MFDs who travelled city to city town to town convincing families to move from gold lockers, FD obsession and LIC-only mindset towards disciplined investing and SIP culture.

The irony is amazing.

The same intellectual ecosystem that constantly lectures India about “financialisation of savings” also uses MFDs as a punching bag every second week… especially many of those whose entire personality now revolves around selling international funds or investing in every fourth loss making glamour stock listed as 4 AM!

Apparently a guy convincing a middle class family to start a Rs 5000 SIP is the problem… not blind global momentum chasing packaged as sophisticated investing..

MFDs manage behaviour more than money.

They stop panic during crashes.

They create discipline during volatility.

They bring first generation investors into markets.

They build last mile trust in a country where financial literacy is still evolving.

Without that layer India would still be largely sitting in idle savings and insurance policies sold as investments.

Of course there are bad actors in every industry. But reducing the entire distribution ecosystem into a sarcastic one liner has now become fashionable.

Easy to joke about distributors. Far harder to build investor behaviour for 15 years through two bear markets and multiple crashes.

The High Cost of "Cheap & Fast" Financial Advice

In the world of professional services, there is an inescapable rule: You can have it Good, Fast, or Cheap—but you can only pick two.

Fast & Cheap? It won't be Good. This is the domain of generic, mass-market "opinions" that ignore your specific context.

Good & Cheap? It won't be Fast. Deep, quality analysis takes significant time and cannot be scaled for the masses at a discount.

Good & Fast? It won't be Cheap. Personalized, expert guidance that reacts to your life in real-time requires a dedicated professional.

The "Mass-Market" Mirage

Many generic platforms and services downplay the role of a professional Mutual Fund Distributor (MFD). Their goal is simple: attract the masses with a low price point and sell a "one-size-fits-all" solution in bulk.

But wealth management is not a bulk commodity. While these services focus on volume, an MFD focuses on Accountability.

Why Personalization Wins:

Context over Content: A mass-market service doesn't know your temperament, your family's baggage, or your long-term goals. They provide content; we provide context.

Accountability: When the markets turn volatile, "cheap and fast" services often offer little more than an automated FAQ. A professional MFD stands by you as a fiduciary, accountable for the long-term journey.

The Complexity Gap: Personalised advice helps you navigate the spectrum—Equity, Debt, Gold, and Global—to ensure your portfolio isn't just "cheap," but actually effective for your specific risk profile.

Don't bet your family's future on a "cheap" shortcut. In the long run, the most expensive advice is often the kind that cost you the least upfront.

Disclaimer: I am an AMFI-registered Mutual Fund Distributor. This content is for educational purposes only and does not constitute investment or financial advice. It is not a recommendation to buy or sell any specific securities. Mutual Fund investments are subject to market risks. Read all scheme-related documents carefully.

We pulled off a coup when we got 3 of the sharpest minds in the mutual fund industry to meet our clients in Pune for our Annual Investor Conclave.

The lucid @AashishPS, the calibrated @hktg13 & the incisive @SahilKapoor.

One stage. 3 experts and 150+ investors in the room. Our clients had heard a lot of noise over the past 15 months and were wondering how to tackle this uncertain environment.

One evening sorted that out.

No fluff. No jargon. Just three experts sharing their perspectives on navigating markets with clarity and discipline.

Beyond the insights, the evening fostered meaningful conversations and stronger relationships.

Grateful to our special guests for making the trip. 🙏

Every client who gave us their Saturday evening — thank you. It means a lot. 😇

And the Aksha team? Wonderful execution. Proud of you all. 👍

Tracking Nifty daily. Scrolling finfluencers. Watching CNBC. You think that's taking control of your portfolio?

It's not. It's just anxiety with a financial dashboard.

If your portfolio is 2x your annual income, a good MFD costs you around one week of your salary. That's it.

And one emotional mistake on that portfolio? Easily months of salary gone!

In return for one week's income equivalent fees, you stop being that person who checks markets at dinner, who loses sleep before every budget day, who reads 14 contradictory opinions and still does nothing

Instead, you get 51 weeks of actually living.

→ Present with your family, not distracted by tickers

→ Focused on your career, your actual primary income

→ At the gym or on the trekking trail, not glued to a screen

Most finance content isn't knowledge. It's noise designed to keep you hooked. A good professional doesn't just manage your money. They manage your mental load around it - so you don't have to carry it alone.

Don't just invest in the market. Invest in your time.

If this hit home, DM is open.

1/ Look at this viral post. The investor has been in the market since mid-2021 (nearly 5 years as of April 2026).

Invested: ₹17.62 Lakh

Returns: ~5.73% (Absolute)

The Complaint: "Mutual funds are a scam."

But the problem isn't the fund. It's the MWRR vs. TWRR gap. Let’s break it down. 👇

The "Silent Dashboard" of DIY platforms is failing investors. 📱🤫

AMFI data shows a massive jump in SIP stoppages (100%+) this March. Without a guide, market corrections lead to emotional exits.

At Moneyworks4u, our 1-to-1 reviews and proactive education keep stoppage for Q4 at 3% of SIP book. Out team acted as an emotional anchor and as a gatekeeper against emotional decisions for our clients.

Stop being a "transaction." Become a "relationship."

Most people invest… but very few understand what they’re doing.

Markets, investments, or money behavior — ask me anything 👇

No question is too basic or too complex. I’ll pick the top 20 questions and answer them in detail on YouTube.

🎥 Video link will be shared by here — stay tuned.

We had yet another phenomenal year at Aksha Moneyworks4u. Our AUM grew by 38%, the SIP book group grew by 1.53 Crs & we got 104 Crs of net new inflow in a challenging year like FY 25-26. We added 170+ new families and over 150+ family members of existing clients.

The Aksha Moneyworks4u team is also shaping up well as they pursue professional certifications and gain invaluable experience in managing client relationships across market cycle. We recently hired an experienced Research Analyst to deepen the quality of our investment thinking.

We are grateful to our clients for putting their trust in us in such a difficult year and for being our brand ambassador while referring us to their friends and family.

@SD_7242@_RAJAT_2@PKoltepatil@sanketr_7121@Aditya_Tilekar_@kakbhushundii

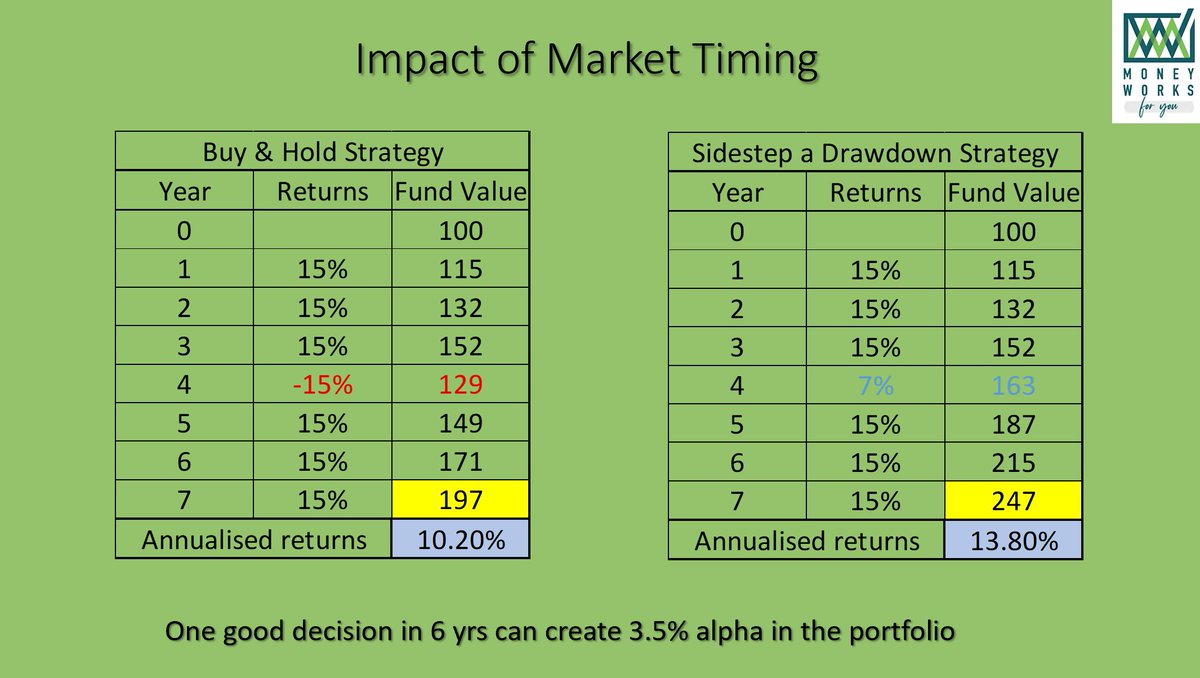

They say "Time in the market beats timing the market." Usually, they’re right. But when the Smallcap index goes sideways for 2 years, tactical allocation becomes the ultimate superpower.

Here’s how we ensured our clients are poised to make beat the market over the medium term with less stress. 👇

In Feb 2024, we reduced mid/smallcap exposure by half. We didn't sit in cash. We rotated into:

Arbitrage & BAFs

Gold Mining & US Value

China & Banking/Financials

The result? While smallcaps stayed flat, the "parked" capital kept working.

The Math: By avoiding the drawdown and reinvesting lower, a hypothetical 60% recovery in smallcaps over the next 3 yrs leads to a 13.8% CAGR vs. 9.8% for Buy & Hold. That’s a 30% excess return over 5 years—all while sleeping better at night.

The kicker? That 6% total portfolio alpha covers roughly 7 years of management fees. Good advice doesn't just grow wealth; it pays for itself by managing the "volatility tax" most investors pay blindly. 📈

Fill up the enquiry form to setup an meeting with us

https://t.co/bVieUu6rhs

If a MFD/RIAs can get just one market call right in 5-7 yrs it can add much more value than the fees you pay to hire an advisor. No one knows the precise top or bottom, but we have had a pretty decent track record of evaluating market's risk-reward and taking timely action in our client's portfolios.

DIY investors can reach out to @stableinvestor for fee-based advisory or they can reach out to us for MFD services by filling up the enquiry form 👇

https://t.co/WOGdRf1Hzf

The NAV difference after nearly 13 years and 9x gains in the fund NAV is just about 9%. This flies in the face of ridiculous claims made by finfluencers to downplay the role of an advisor.

A good MFD will add value that is multiple time this over 13 yrs and multiple bull-bear cycles.

What a year 2025 has been! It was the year of "the pivot." We started by aggressively buying the correction and trusting our gut on the Indian equity markets when the sentiment was low. Aside from selling gold a bit too soon (my biggest lesson this year!), it felt like we had the Midas touch.

The growth metrics reflect the deep trust our clients place in us:

AUM Growth: 57% (vs. an industry average of 17%).

Inflows: ₹100 Cr+ in new capital.

Scale: Our client base expanded by 33%, and our SIP book nearly doubled.

Interestingly, most of our new growth came from DIY investors seeking professional management as their portfolios grew in complexity or their professional lives grew more demanding.

Between travelling across India to meet the new and old clients, moving into our beautiful new office, and being featured in The Economic Times, it’s been a whirlwind. I’m incredibly proud of my team—we’ve upskilled, evolved, and worked harder than ever.

The only thing that didn’t grow? My fitness levels! 😅 With all energy poured into the business, personal goals took a backseat. As I look back, I’m just deeply grateful. We are no longer just a local firm; we are a national team ready for what’s next.

What happens when you stop your SIP during a bear market just because the portfolio XIRR is looking low.

We analysed real SIP data from October 2017 to November 2025 — eight years, three equity funds, ₹10,000 SIP each month.

And when you look at this period, you see one clear truth: markets will keep testing you, but SIPs reward those who stay consistent.

2018 had LTCG tax, the NBFC crisis, and global tensions — the first dip.

2019 was a slow, grinding year where confidence fell.

2020 brought the Covid crash — the steepest fall on the chart.

2021 had another wobble with the second Covid wave.

2022 came with inflation, rate hikes, and the Russia–Ukraine war.

2023 saw volatility from global yields, corporate news, and FII selling.

2024 had healthy corrections because valuations were high.

2025 faced growth worries and foreign selling, leading to a long drawdown.

Through all this, XIRR jumped up and down in the early years.

This is where most people panic and doubt their SIPs.

But SIPs were never meant to perform in 6–12 months.

As more instalments go in and more cycles get absorbed, the impact of any single crash reduces.

When you zoom out, the long-term returns become strong and stable.

Short-term noise means nothing.

Long-term compounding means everything.

Stay consistent — that’s how wealth is built.