Leading provider of management services for maritime investors, including investment structuring, sale and purchase, operational and financial management.

Our view is that the probability of a spike in spot Capesize rates is real, but the curve is overly optimistic about the extend and sustainability of such potential higher rates.

#drybulk#markets

See the most important parts of the report on the video here below ⬇

For the full report click here: https://t.co/9zxPGk3t7D

SGM dry sentiment index (-5 to +5):

Capesize +5, Panamax +4, Supramax +3, Handy +2, Short Sea +2

Views: Despite current momentum, 2025 fundamentals remain challenging and could disappoint.

To all our clients, partners, and friends in the industry, we sincerely thank you for your support and collaboration in 2024.

We wish you a happy and prosperous 2025, filled with successes and opportunities.

May we all continue working diligently in facilitating maritime transport for the benefit of all.

Happy New Year!

Carbon capture technology is currently the most viable option for decarbonizing the shipping industry, as alternative green fuels won’t be available at scale for decades. While not a silver bullet, it offers achievable capture rates of 82%-90% and can be implemented immediately to significantly reduce CO2 emissions, buying time for the development of sustainable fuel alternatives. #Decarbonization #CarbonCapture

#Shipping

BV: Carbon capture is not a silver-bullet solution, it must be used with other decarbonization strategies

https://t.co/IB37Z4qxOt

#carbon#maritime#shipping#decarbonization

An interesting view expressed below is the (possible) long-term decrease in trade volumes due to decarbonisation concerns. This would risk impoverishing the entire world if we follow the trade theory of David Ricardo and many subsequent economists. We should rather believe in technological improvements than in global impoverishment.

From the sheer number of visit requests we have received from companies globally coinciding with the upcoming Geneva Dry conference on the 2nd & 3rd May, this could be one of the most important events centred around drybulk worldwide.

It also reminds us why Geneva, and Switzerland in general, remains a major hub for shipping and commodities.

Throughout the Cold War, Geneva held an important role as a diplomatic center in a neutral country and became a ‘safe space’ to do business. Merchants from both American and Soviet companies established a presence in the late ‘60s SGM's former offices, located Place Jean-Marteau, were previously those of a well-known Soviet shipping group.

More and more traders moved to Geneva, leading to a complete ecosystem underpinned by commodity trade finance.

Building on this legacy, we have today:

- A very competitive—and compliant—corporate tax system

- Excellent living standards for expats (especially those with families)

- A safe and stable environment

- A strong ecosystem in finance and legal support for commodity traders

- A huge local network of professionals

- Qualified personnel and an attractive destination for expats

Hope to see many of you next week in town!

#drybulk #shipping

Introducing the new 38k index-type handysize has complicated rate assessments for smaller handies, even though they remain the biggest part of the handysize fleet. This table shows the spot implied rates for main (smaller) specs, based on our correlation formulas. #drybulk

After a tough FH 2023 due to rising interest rates & low Chinese activity, rates may have hit a floor. Limited supply-side growth hints at a recovery, but its pace hinges on China's actions. Now more than ever, China's role will be crucial. 🌏💹 #drybulk#maritime

Just a reminder: EU, USA and Australia account for roughly 42% of the world's GDP combined. This makes two competing currency reserves a more probable scenario than the USD fully losing its reserve status. #economics

Today's word of the day: de-dollarisation. Talks of USD losing its reserve currency status are increasing, but is there a reasonable alternative in sight? Could the Yuan be the answer? The BRICS+, representing over 1/3rd of the world economy, seem to think so. #BRICS+#USD

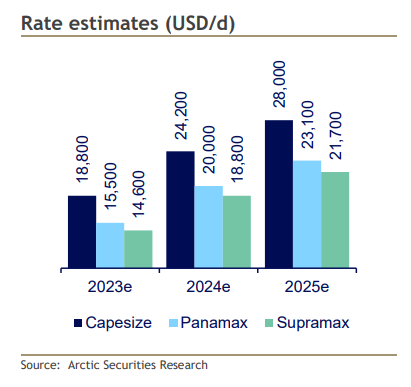

Arctic: What expected to be a H2 recovery story appears to materialise now. We raise 2023 rate est by 10-12%, 2024 by 10-18%, and introduce 2025. Asset values troughed in Dec, are now on the rise, which, combined with rising rates, should lift NAVs. We upgrade to BUY #drybulk

Bulk freight market sees firm lift. Whether the strength can be maintained or is a short-term correction remains to be seen, but 𝗶𝗻𝗱𝗶𝗰𝗮𝘁𝗼𝗿𝘀 𝗮𝗿𝗲 𝗽𝗼𝗶𝗻𝘁𝗶𝗻𝗴 𝘁𝗼𝘄𝗮𝗿𝗱𝘀 𝗽𝗼𝘀𝗶𝘁𝗶𝘃𝗲 𝗺𝗼𝗺𝗲𝗻𝘁𝘂𝗺 (Lloyd's List).

#drybulk#shipping $BDRY

Shipping markets sluggish post-holiday season as activity resumes gradually. Operators trying to take advantage, but 2023 fundamentals not bad with expected upswing in demand from China following COVID. Lack of newbuilding orders a positive long-term indicator. #shipping#drybulk

By February 5, 2023, or about 5 weeks from now, China is likely to speed up, coming out of covid and Holidays around Chinese year.

That date is also the date of planned price cap on Russian product export.

To Me, it is a given to be positioned in tankers now.