@MithunSarkari Did you open any new position or increase position on any stocks recently? Not seeing any updates so curious. I know it's not buy/sell recommendations. Just to research on your higher conviction stocks after recent earnings

Sharing some thoughts on $FICO 👇🏽

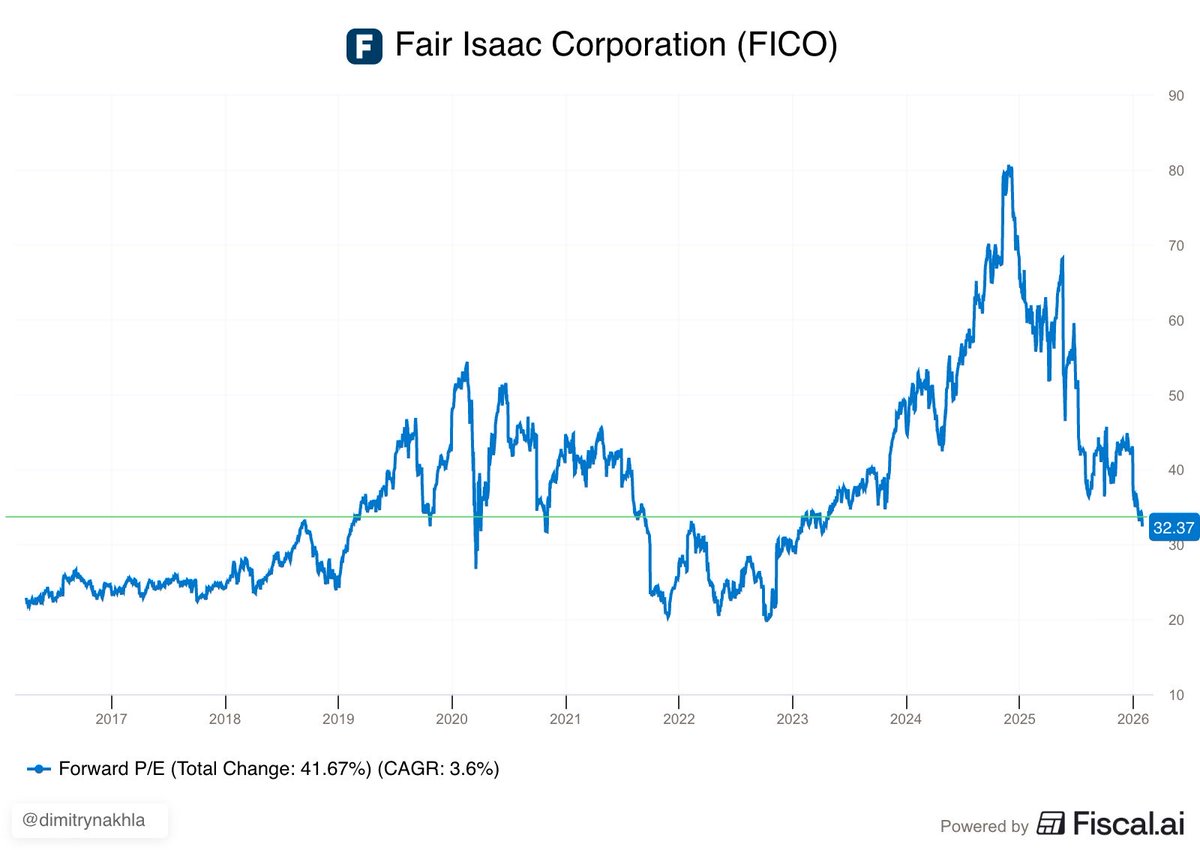

Photo 1: $FICO now trades 32x NTM earnings estimates. Just four days ago, ahead of its Q1 2026 report, it traded 39x. $FICO is down ~5% in the past 5 days, so most of that multiple contraction (~18%) is due to aggressive growth in earnings.

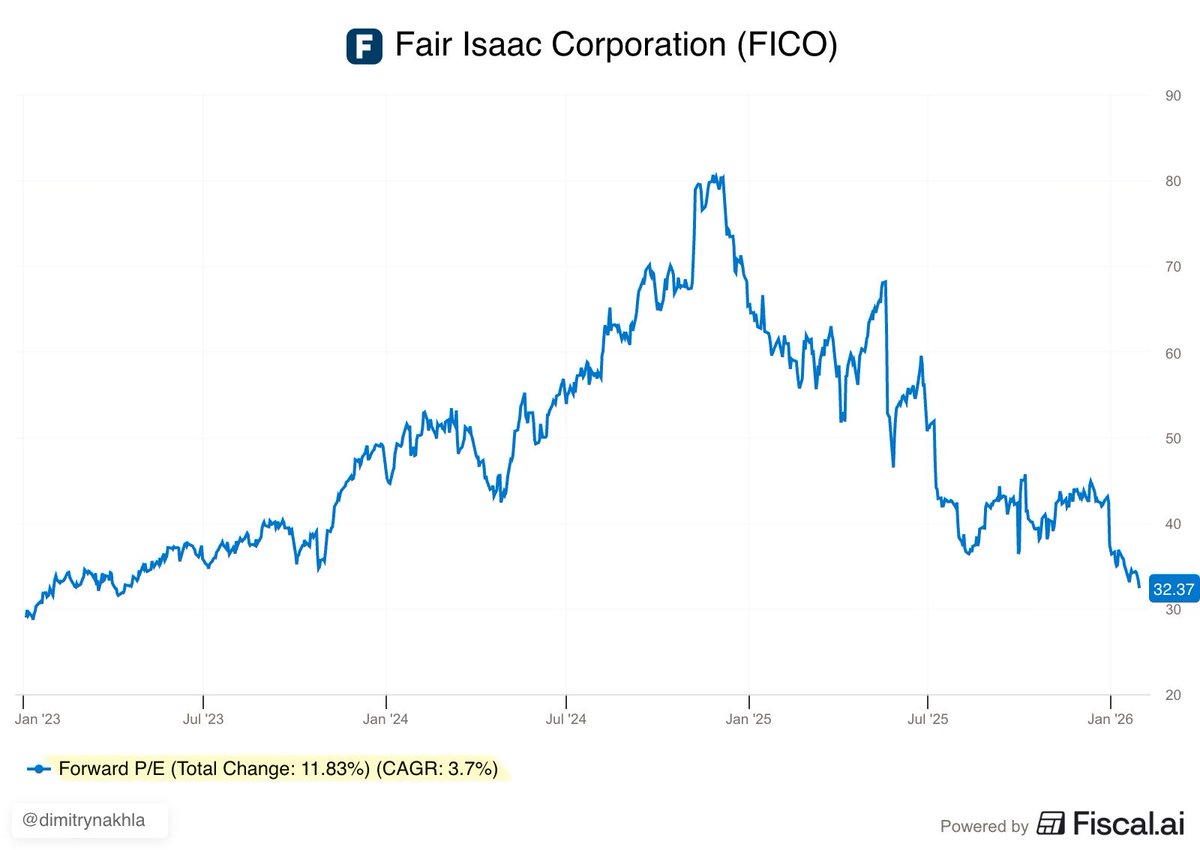

Photo 2: Since January 2023, $FICO has a total return of 147.50% or a 34.3% CAGR despite the multiple expanding only 11.83% since then. In other words, nearly all of the return over that time period has been driven by strong earnings growth.

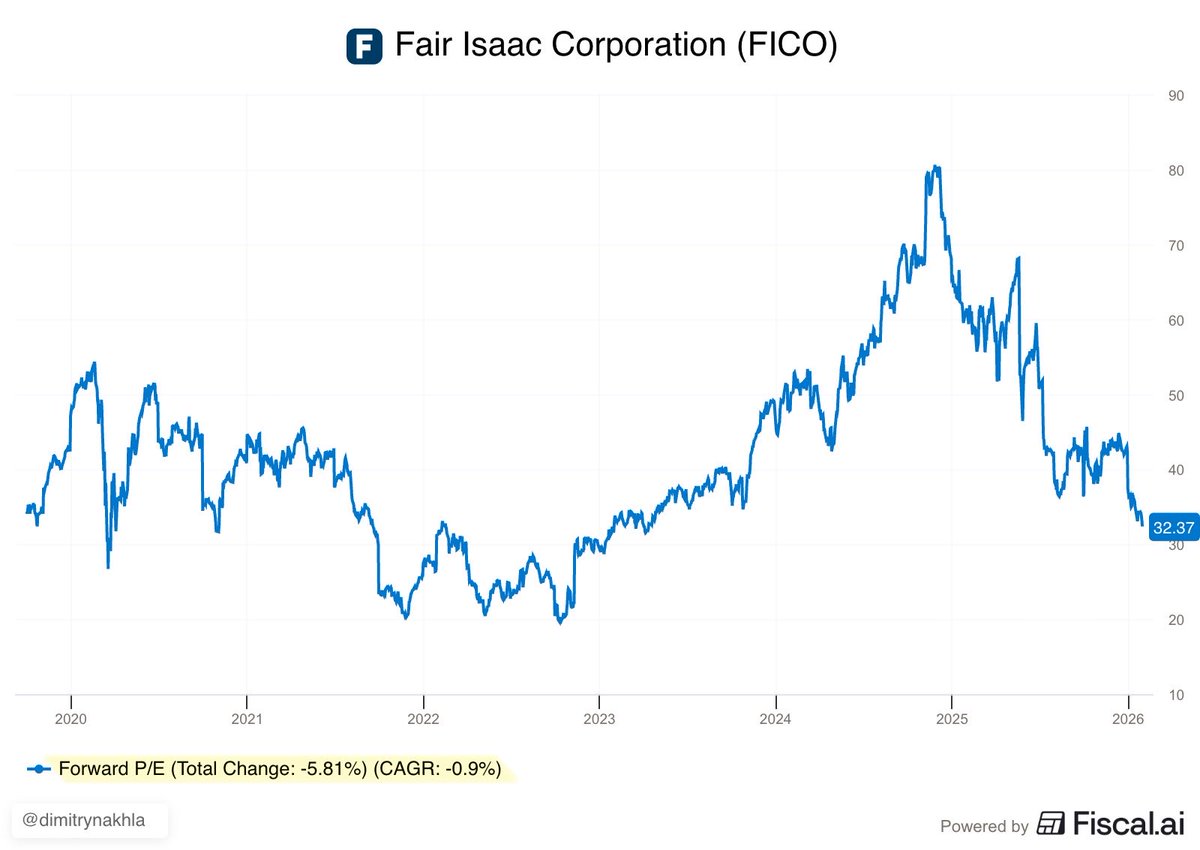

Photo 3: Since September 2019, $FICO has a total return of 355.80% or a 26.9% CAGR despite the multiple contracting -5.81% since then. Again, an incredible return in the face of slight multiple compression due to strong earnings growth.

Photo 4: Since September 2024, $FICO is down -24.20% while its multiple was halved, contracting -50.78%. While $FICO dropped during that period, again you see the impact strong earnings growth can have even in the face of severe multiple compression.

𝘉𝘳𝘪𝘯𝘨𝘪𝘯𝘨 𝘵𝘩𝘪𝘴 𝘵𝘰𝘨𝘦𝘵𝘩𝘦𝘳, 𝘩𝘦𝘳𝘦’𝘴 𝘢 𝘭𝘰𝘰𝘴𝘦 𝘱𝘢𝘳𝘢𝘱𝘩𝘳𝘢𝘴𝘦 𝘰𝘧 𝘴𝘦𝘷𝘦𝘳𝘢𝘭 𝘪𝘥𝘦𝘢𝘴 𝘋𝘦𝘷 𝘒𝘢𝘯𝘵𝘦𝘴𝘢𝘳𝘪𝘢 𝘩𝘢𝘴 𝘴𝘩𝘢𝘳𝘦𝘥 𝘢𝘤𝘳𝘰𝘴𝘴 𝘱𝘰𝘥𝘤𝘢𝘴��𝘴:

💬 The biggest mistake investors make is focusing on the nominal P/E ratio of a high-quality company today. If you have a business that can grow its free cash flow at 15% or 20% for a decade or two, the ‘expensive’ 30x or 40x multiple you are paying today is actually a significantly lower multiple on the earnings power just a few years out. The market consistently underestimates the duration of growth for these ‘toll-bridge’ monopolies.

___

Today, $FICO trades at a more than reasonable PEG of ~1.41x.

My research also leads me to believe $FICO could have an $ASML moment within the next five years.

Here’s what I mean by that. Those of us who have been bullish on $ASML for the last several years knew, with a high degree of certainty, that $ASML would eventually see a surge in orders as demand naturally had to increase to support the advancement of AI and chip production at an unprecedented scale.

Yes, it wasn’t linear for $ASML, and for a few years it lagged many semiconductor players. Yet, what happened? In $ASML’s latest report, Q4 net bookings came in at €13.13B (+86% YoY) versus estimates of €6.85B — nearly double. And of course the stock surged +93% in just the past year.

At some point within the next five years, I anticipate that mortgage rates (among other things) will fall meaningfully enough to drive a surge — similar to $ASML net bookings spike — in refinance demand, alongside higher origination volumes from lower rates, all coupled with price increases.

That combination creates a “twin engine” of higher volumes + higher prices, which could translate into materially higher earnings and free cash flow than what current estimates imply, especially over the long term.

Here’s the catch: nobody knows when this will happen (similar to $ASML). However, those who are patient may be rewarded.

If you deeply understood $ASML importance and the inevitable, much greater demand for its machines, you were able to hold with confidence.

$FICO rhymes.

Two different “toll booths” in two different sectors — yet potentially very similar dynamics.

Over the last five years, $MA has consistently converted ~50%–70% of incremental revenue into operating income and just posted its 𝙝𝙞𝙜𝙝𝙚𝙨𝙩 𝙞𝙣𝙘𝙧𝙚𝙢𝙚𝙣𝙩𝙖𝙡 𝙢𝙖𝙧𝙜𝙞𝙣 𝙤𝙛 72% 💳

2020→2021: 56%

2021→2022: 65%

2022→2023: 61%

2023→2024: 51%

2024→2025: 72%

A quality valuation analysis on $NOW 🧘🏽♂️

•NTM P/E Ratio: 52.28x

•3-Year Mean: 34.73x

•NTM FCF Yield: 3.61%

•10-Year Mean: 2.49%

As you can see, $NOW appears to be trading below fair value

Going forward, investors can expect to receive ~50% MORE in earnings per share & ~45% MORE in FCF per share🧠***

Before we get into valuation, let’s take a look at why $NOW is a quality business

BALANCE SHEET✅

•Cash & Equivalents: $5.41B

•Long-Term Debt: $1.49B

$NOW has a strong balance sheet, an A S&P Credit Rating & 210x FFO Interest Coverage Ratio

RETURN ON CAPITAL❌➡️✅

•2021: 4.3%

•2022: 5.2%

•2023: 8.1%

•2024: 11.8%

•LTM: 13.3%

RETURN ON EQUITY❌➡️✅

•2021: 7.0%

•2022: 7.4%

•2023: 27.3%

•2024: 16.5%

•LTM: 16.8%

$NOW return metrics are improving & trending in the right direction — a sign the business is becoming more efficient

REVENUE✅

•2020: $4.52B

•2025E: $13.24B

•CAGR: 23.97%

FREE CASH FLOW✅

•2020: $1.37B

•2025E: 26.79%

NORMALIZED EPS✅

•2020: $0.93

•2025E: $3.48

•CAGR: 30.20%

SHARE BUYBACKS❌

•2019 Shares Outstanding: 986.12M

•LTM Shares Outstanding: 1.05B

MARGINS🆗 / ✅

•LTM Gross Margins: 78.1%

•LTM Operating Margins: 14.4%

•LTM Net Income Margins: 13.7%

SGA is $NOW largest expense eating ~41% of LTM revenue, something to keep an eye on

***NOW TO VALUATION 🧠

As stated above, investors can expect to receive ~50% MORE in EPS & ~45% MORE in FCF per share

Using Benjamin Graham’s 2G rule of thumb, $NOW has to grow earnings at a 17.37% CAGR over the next several years to justify its valuation

Today, analysts anticipate 2026 - 2028 EPS growth over the next few years to be slightly less (16.84%) than the (17.37%) required growth rate:

2025E: $3.48 (25% YoY) *FY Dec

2026E: $4.08 (17% YoY)

2027E: $4.89 (20% YoY)

2028E: $5.57 (14% YoY)

$NOW has an excellent track record of meeting analyst estimates ~2 years out, so let’s assume $NOW ends 2028 with $5.57 in EPS & see its CAGR potential assuming different multiples

34x P/E: $189💵 … ~12.2% CAGR

33x P/E: $184💵 … ~11.1% CAGR

32x P/E: $178💵 … ~9.9% CAGR

31x P/E: $173💵 … ~8.8% CAGR

30x P/E: $167💵 … ~7.6% CAGR

29x P/E: $161💵 … ~6.4% CAGR

As you can see, we’d have to assume a >34x multiple for $NOW to have attractive return potential

At 32x earnings $NOW has ok CAGR potential

Given its -40% drawdown, $NOW appears to be fairly valued today at $135💵

Yes, $NOW is the workflow operating system for large enterprises, automating & governing critical work across IT, HR, security, & customer service

Once embedded, it becomes deeply integrated into how the organization runs, creating high switching costs & powerful long-term expansion

With AI layered onto these workflows, $NOW can increasingly automate & execute work end-to-end

Yet, today’s price offers little margin of safety

I consider $NOW a strong consideration with a decent margin of safety at $110💵, where I can reasonably expect ~13% CAGR while assuming a more conservative 28x

___

���𝐈𝐒𝐂𝐋𝐎𝐒𝐔𝐑𝐄‼️

𝐓𝐡𝐢𝐬 𝐜𝐨𝐧𝐭𝐞𝐧𝐭 𝐢𝐬 𝐩𝐫𝐨𝐯𝐢𝐝𝐞𝐝 𝐟𝐨𝐫 𝐢𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐚𝐧𝐝 𝐞𝐝𝐮𝐜𝐚𝐭𝐢𝐨𝐧𝐚𝐥 𝐩𝐮𝐫𝐩𝐨𝐬𝐞𝐬 𝐨𝐧𝐥𝐲 𝐚𝐧𝐝 𝐝𝐨𝐞𝐬 𝐧𝐨𝐭 𝐜𝐨𝐧𝐬𝐭𝐢𝐭𝐮𝐭𝐞 𝐢𝐧𝐯𝐞𝐬𝐭𝐦𝐞𝐧𝐭 𝐚𝐝𝐯𝐢𝐜𝐞, 𝐚𝐧 𝐨𝐟𝐟𝐞𝐫, 𝐨𝐫 𝐚 𝐬𝐨𝐥𝐢𝐜𝐢𝐭𝐚𝐭𝐢𝐨𝐧 𝐭𝐨 𝐛𝐮𝐲 𝐨𝐫 𝐬𝐞𝐥𝐥 𝐚𝐧𝐲 𝐬𝐞𝐜𝐮𝐫𝐢𝐭𝐲.

𝐁𝐚𝐛𝐲𝐥𝐨𝐧 𝐂𝐚𝐩𝐢𝐭𝐚𝐥® 𝐚𝐧𝐝 𝐢𝐭𝐬 𝐫𝐞𝐩𝐫𝐞𝐬𝐞𝐧𝐭𝐚𝐭𝐢𝐯𝐞𝐬 𝐦𝐚𝐲 𝐡𝐨𝐥𝐝 𝐩𝐨𝐬𝐢𝐭𝐢𝐨𝐧𝐬 𝐢𝐧 𝐭𝐡𝐞 𝐬𝐞𝐜𝐮𝐫𝐢𝐭𝐢𝐞𝐬 𝐝𝐢𝐬𝐜𝐮𝐬𝐬𝐞𝐝. 𝐀𝐧𝐲 𝐨𝐩𝐢𝐧𝐢𝐨𝐧𝐬 𝐞𝐱����𝐫𝐞𝐬𝐬𝐞𝐝 𝐚𝐫𝐞 𝐚𝐬 𝐨𝐟 𝐭𝐡𝐞 𝐝𝐚𝐭𝐞 𝐨𝐟 𝐩𝐮𝐛𝐥𝐢𝐜𝐚𝐭𝐢𝐨𝐧 𝐚𝐧𝐝 𝐬𝐮𝐛𝐣𝐞𝐜𝐭 𝐭𝐨 𝐜𝐡𝐚𝐧𝐠𝐞 𝐰𝐢𝐭𝐡𝐨𝐮𝐭 𝐧𝐨𝐭𝐢𝐜𝐞.

𝐈𝐧𝐟𝐨𝐫𝐦𝐚𝐭𝐢𝐨𝐧 𝐡𝐚𝐬 𝐛𝐞𝐞𝐧 𝐨𝐛𝐭𝐚𝐢𝐧𝐞𝐝 𝐟𝐫𝐨𝐦 𝐬𝐨𝐮𝐫𝐜𝐞𝐬 𝐛𝐞𝐥𝐢𝐞𝐯𝐞𝐝 𝐭𝐨 𝐛𝐞 𝐫𝐞𝐥𝐢𝐚𝐛𝐥𝐞 𝐛𝐮𝐭 𝐢𝐬 𝐧𝐨𝐭 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞𝐝 𝐚𝐬 𝐭𝐨 𝐚𝐜𝐜𝐮𝐫𝐚𝐜�� 𝐨𝐫 𝐜𝐨𝐦𝐩𝐥𝐞𝐭𝐞𝐧𝐞𝐬𝐬. 𝐏𝐚𝐬𝐭 𝐩𝐞𝐫𝐟𝐨𝐫𝐦𝐚𝐧𝐜𝐞 𝐝𝐨𝐞𝐬 𝐧𝐨𝐭 𝐠𝐮𝐚𝐫𝐚𝐧𝐭𝐞𝐞 𝐟𝐮𝐭𝐮𝐫𝐞 𝐫𝐞𝐬𝐮𝐥𝐭𝐬.

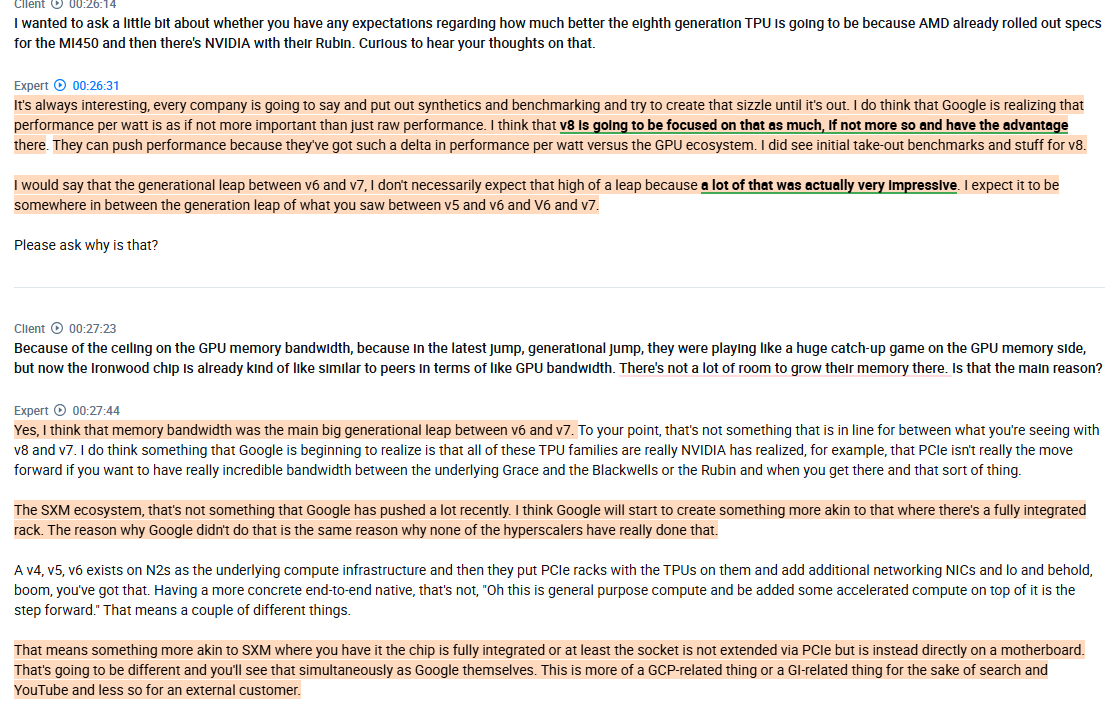

A MUST-read interview with a former $GOOGL employee who worked on TPUv5,v6, & v7 on TPUs vs GPUs. I will be posting the interview in two parts, the first one today and the second one tomorrow:

1. According to him, $GOOGL TPUs are 20-30% more cost-efficient on perf per watt vs the GPU alternative. He mentions that if you are using an Ironwood pod vs an $NVDA NVL72 B200, the TPU pod consumes 30% less power. Part of it is the smaller die, but he believes that even if the die size were the same, the power draw of an ASIC would still be smaller than a GPU.

2. Part of $GOOGL's edge with TPUs is that they were designed for liquid cooling from the start. He believes $GOOGL's data centers are currently far more efficient with liquid-cooled TPUs than any customer spinning up a Blackwell with liquid cooling.

3. He agrees that Mixture of Expert models (MOEs) are running less efficiently on TPUs than some of the denser models. He thinks that the main reason for that is that they weren't designed for that, but at the same time, MoE models have so far been optimized around GPUs with the help of the »DeepSeek moment«. TPUs are not yet available to people for experimentation.

4. In his view, $GOOGL would only need a year to change the architecture to handle MoEs better.

5. He thinks that over time, the 95% market share of $NVDA will go down to 80-75% with $GOOGL TPUs taking a significant share of 20-25%. He believes that a substantial share of the gains for $GOOGL's TPUs will also come from $AMD. He thinks $NVDA will trigger a pricing war to improve its TCO. With it, he believes the $NVDA margin will come down substantially.

6. One of the main things $GOOGL needs to do if it wants to sell TPUs externally is to improve its PyTorch support and the gaps there. He believes these gaps will be addressed. At the same time, he thinks the lack of CUDA support on TPUs is a smaller problem than it is for $AMD. The value proposition of TPUs is their greater energy efficiency, driven by their architecture; $AMD doesn't offer that.

7. When it comes to TPUv8, he thinks that $GOOGL is realizing that performance per watt is more important than raw performance and that v8 will be focused on that as much, if not more so, and have the advantage there: »They can push performance because they've got such a delta in performance per watt versus the GPU ecosystem«. At the same time, he doesn't expect the leap between v7 and v8 to be as big as the leap was between v6 and v7. The main leap from v6 to v7 was the memory bandwidth.

8. He thinks $GOOGL will move more towards an SXM ecosystem to have a chip fully integrated or at least the socket not extended via PCIe but instead directly on a motherboard.

found on @AlphaSenseInc

I will publish the second part tomorrow, where he explains the key advantage of TPUs.

I've added $CRDO on the 25.7% drop, taking advantage of CES misinformation.

1. Large drop initially was because investors spotted orange and blue cables in $AMZN DCs (implying $CRDO customer loss).

All that happened was Amazon requested a color change for internal logistics. - confirmed by Vijay Rakesh from Mizuho.

2. CES 2026 keynote - Second drop was Jensen Huang said "Cableless" design of Rubin NVL72 rack.

The "cableless" claim refers specifically to the internal copper backplane (blind-mate midplane) that connects the GPUs to the NVLink switches within a single rack.

$CRDO's main product is AEC, for outside of the racks that connect the entire server rack to the network switch. Nvidia's "Cableless" Tech only replaces internal parts Credo didn't make.

Jensen did mention Spectrum-X Ethernet Photonics, but $CRDO is operating in the photonics space too with "BlueBird" (Optical DSPs) and "ZeroFlap" optics. And then there's Top of the Rack Connectivity, which is Credo's main business (which is the most power efficient solution for the next 2-3y).

There are larger concerns over the shift to photonics (as I've pointed out with $AXTI multiple times), but industry is moving toward a hybrid model (copper + photonics) given the supply shortage.

Again as an overview, investors just did not know the nuances, not intentional disinformation.

So I ended up personally adding $CRDO since a large percent of its market cap got wiped from immaterial + incorrect news.

$META has just opened the floodgates for the AI agentic application layer. $META just acquired Manus, an AI-agentic startup, for more than $2B because Manus excels at agentic real-world tasks. It is also the startup that has reached the $100M ARR market the fastest in history (8 months).

While many might think Manus is just an LLM wrapper, a closer look at the company reveals some interesting aspects and values:

Manus, unlike ChatGPT, was built to execute tasks rather than provide text answers. The goal is to assign it a high-level task so the agent can navigate different tasks autonomously to complete the job (e.g., navigating the web, writing code). Foundation models predict the next word, while Manus predicts the next action.

The unique part about Manus is that it uses an architecture called Code-Act. Instead of just talking about a problem, it writes a Python script on the fly to solve it, executes that script in a secure »sandbox« (virtual machine), and looks at the result. The Sandbox means that Manus provides every user with a dedicated, cloud-based Linux environment. They now have more than 80M virtual computers. This means the upfront costs are higher than with ChatGPT. You pay for the virtual computers even when they are idle, but because of their specific architecture, they are cheaper per task completed. Manus is model-agnostic and uses multi-model routing. For scraping a website, it can use a low-cost model; for summarizing content, it can use a more expensive model within the same task. It also caches previous task executions, so if, for example, it has already solved how to log in to a site, it saves the script from previous tasks and, with it, the tokens. Because it runs in the background with the virtual machines and uses a 3-agent orchestration system of a planner, an executor, and a verifier, it also often doesn't need »retries« like other models need (as they often lose focus or connection to do long-hour tasks). The combination of those things makes it cheaper per solved task.

Manus at launch was higher than OpenAI Deep Research across levels 1, 2, and 3 of the GAIA benchmark. The GAIA benchmark is a reality check for AI agents on how well they perform on real-world tasks that are routine for humans but typically a challenge for AI (humans score 92% accuracy).

How does this fit into $META? Well, $META is looking to build a superintelligent AI assistant for every person, so this aligns with what they are trying to do. They are already working on the foundation model at $META (if they fail, they can use open-source or partner with an AI lab). Still, you also need to have agentic infrastructure, which is everything that Manus has done and has achieved serious traction for it (so it works).

This best fits into $META's WhatsApp as an assistant that they can offer both to consumers and businesses, and a strong play for their $META Ray-Ban Smartglasses, where you need an autonomous, agentic system to run those glasses. $META will also help Manus with its infrastructure, allowing Manus to stop renting virtual machines from cloud providers and use $META's own infrastructure.

With this move, $META also gains an extremely capable team focused on agentic workflows and building the »body« of the agent, as the »brain« is already being built by $META through its foundation model work.

In honesty, $2B-$4B doesn't seem like much given the cost of AI talent today and the traction and growth Manus has had.

Zuck is also showing you where the puck is going. $META might have opened up the floodgates for the application layer of AI with these moves. I expect others will follow, so in hindsight, this deal will look cheap.

Blue Owl walking away from financing the $10B $ORCL data center, according to FT, because "lenders pushed for stricter leasing and debt terms".

The market is starting to question the economics of many of these deals. Things are changing.

$LITE $CRDO Lumentum and Credo: Optical Versus AEC Connectivity Dynamics

The video provides a detailed comparative analysis of two companies highly leveraged to the growth of cloud and AI infrastructure: Lumentum Holdings (LITE), a vertically integrated optical and laser manufacturer, and Credo Technology Group (CRDO), a fabless company focused on Active Electrical Cables (AECs) and SerDes/DSP silicon. The comparison highlights their fundamentally different business models, with Lumentum focusing on high-margin optical components and long-haul networking but carrying substantial convertible debt, while Credo benefits from a capital-light structure and net-cash balance sheet but faces extreme customer concentration within short-reach AEC deployments. The core strategic intersection examined is the competitive zone between copper-based AECs and short-reach optical transceivers for in-rack AI networking, although Lumentum's larger opportunity resides in long-haul coherent optics and ROADM/WSS where Credo's copper solutions cannot compete. Ultimately, the sources project strong growth for both, with Lumentum targeting the optical backbone and Credo focused on the high-growth, high-margin electrical layer of large AI clusters.

Lots of people think that CPO implies that AEC is dead.

It's a lot more nuanced when you ask:

- what generation of networking?

- what levels of reach?

- scale-up or scale-out?

The real answer is that AEC is not going anywhere for now, and here is why:

https://t.co/tW56qOft83

$ORCL is down more than 40% since I sold out of my position.

Many questioned my decision back then, but the reality is that a big part of the AI ecosystem has taken on industry systemic risk with these interconnected deals, LOIs, and debt. Some companies are also willing to "risk it all" in order to gain market share.

I am a big long-term believer in AI and the effects of it, but in the short-term, the frontloading and the headless AI race fueled by too much loose capital has pushed us into a phase where we first need to consolidate, price the business models to real costs, and come "back to reality" before we continue IMO.

$MA increased its quarterly dividend by +14% to $0.87 per share & authorized a new $14B buyback program 💳

The new repurchase plan will go into effect after the remaining $4.2B under the existing authorization is completed

Mastercard $MA operating cash flow will soon exceed total debt, something we haven’t seen since 2017

But the best part... They’ve been repurchasing $2–3 billion every quarter since 2019, yet total debt has barely moved

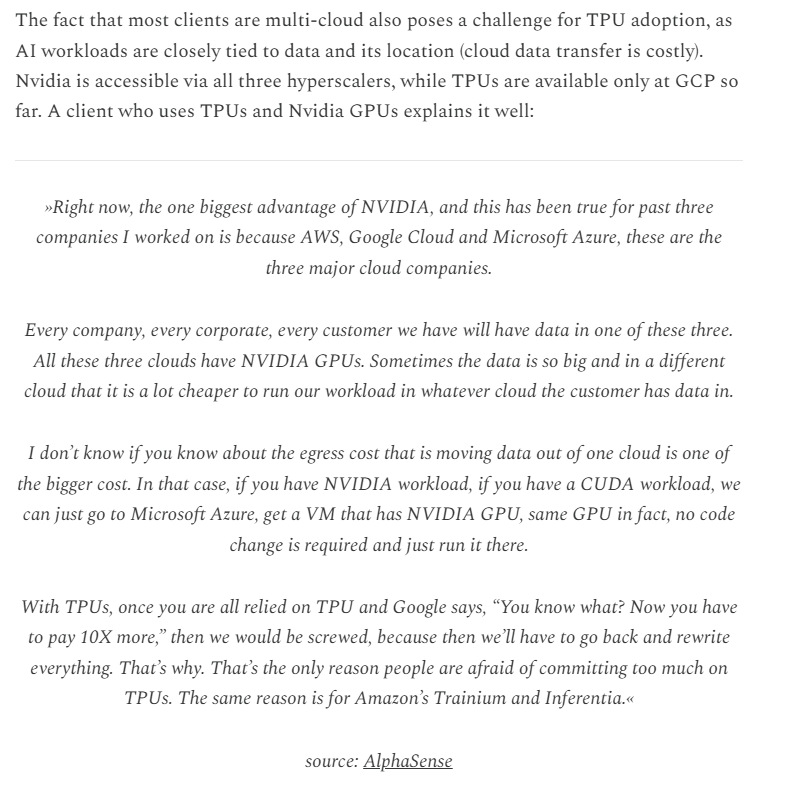

$AMZN AWS and $GOOGL Cloud just partnered on Cross-Cloud Interconnect.

This news is really huge, but most will miss it because they don't understand it.

As I wrote in my article a few days ago, one of the biggest hurdles to $GOOGL TPU adoption is the cost and hassle of moving data between cloud providers.

Morgan Stanley is flagging growing credit risk at Oracle. 5Yr CDS on $ORCL is around 1.25% a year and, per their models, could push toward the 2008 peak near 2% if the market stays uneasy about how Oracle funds its AI data center buildout.

The note cites a funding gap, a swelling balance sheet and “obsolescence risk,” after Oracle raised $18B in bonds and lined up roughly $56B in project and construction loans tied to AI infrastructure.

Analysts have now closed their long bond trade and are sticking with “buy CDS protection” instead.