bitcoin:native is down while the S&P 500 just printed its 19th record high of the year in the same week.

Most people read that split as crypto breaking... I read it as a liquidity story.

Risk capital is leaving risk assets right now, pulled out by a fearful tape, a worse macro picture with the US-Iran crisis, and an AI narrative vacuuming up every marginal dollar. It's flowing into two places: cash and AI.

That's why the S&P 500 can sit at records while almost everything else sells off. That index isn't risk-on. It's AI-on. And that will continue over the next few weeks, with the upcoming record-breaking IPOs from the big AI labs.

None of that negative price action touches the crypto fundamentals. On the contrary... adoption and integration continued to strengthen this year, while price and sentiment fell.

Even the four-year-cycle crowd reads this as a low in the pattern, not a break in the thesis.

So where does price go next? I don't know, and neither does anyone selling you a target. The question worth asking is whether the thesis still holds. I think it's stronger than it's ever been.

This gap between price and fundamentals is a big opportunity for patient investors.

The most interesting move in crypto last week came from an asset almost no advisor had on their radar.

Stellar (stellar:native ). DTCC — the clearing utility at the center of U.S. securities markets, custodying over $114 trillion — picked it as the first public blockchain to carry tokenized assets onto an open ledger. The token repriced sharply on the news.

$XLM is a small constituent of the @Nasdaq CME Crypto Index. A rounding error next to bitcoin’s weight. If you were building a crypto allocation by conviction, you almost certainly wouldn’t have owned it. Through a rules-based index, you did… without having to predict that DTCC would validate Stellar’s rails.

This is the part investors push back on. “It’s mostly bitcoin — why carry the long tail at all?” Because that’s where the asymmetry sits. Those assets are small by market cap, so their weight is small — limited drag if they fade out. But if one grows into its target market, the methodology lets it earn its way up… Winners get bigger, Losers drop out. And no one has to call it in advance.

Same week, ethereum:native is taking heat from its own community over the Foundation’s direction. Telling, for anyone who assumed smart-contract platforms were winner-take-all and Ethereum had already won. FWIW I’m optimistic Ethereum works through it… but the whole point of an index is that you don’t have to agree with me.

On June 1 the index reconstituted and added bitcoin cash. The point isn’t bitcoin-cash:native , but that the rules keep working… the set has grown from 2 assets to 8, mostly as U.S. regulatory clarity made more assets eligible. As the market matures, we think that set keeps expanding.

Boring, disciplined, rules-based. That’s the edge.

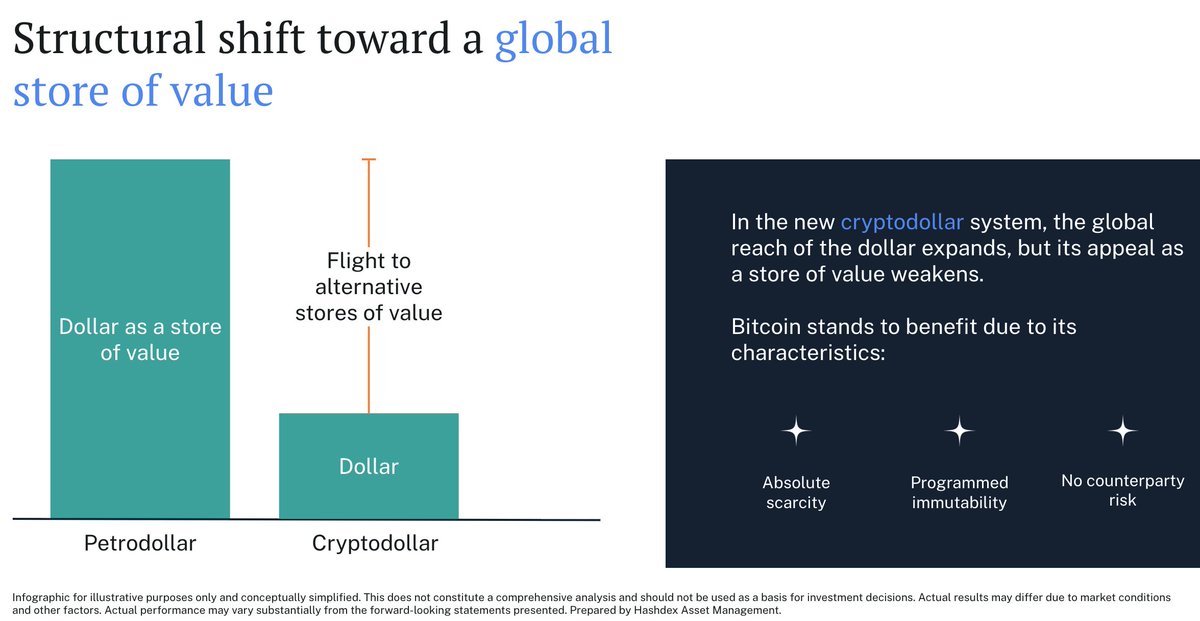

The petrodollar was oil-backed demand for U.S. treasuries. The cryptodollar is internet-backed demand for U.S. treasuries.

Same structural function, completely different rails

In our 2026 Crypto Outlook, we projected stablecoins growing from $295B to over $500B this year... with a path to $2T by 2028.

The ECB sees it — they're alarmed by the cryptodollar, but still resisting the technology instead of embracing it. That tells you where the momentum is.

Everyone says bitcoin dumps at 10AM every day.

I pulled the data, and it's not true.

Since Jan 1, IBIT's cumulative return in the 10:00–10:30 window is +0.9%, and in the 10:00–10:15 window it's –1%. Noisy, not a systematic dump.

More interesting: the performance pattern in both windows closely tracks the Nasdaq's.

The "10AM dump" is just broad risk-asset repricing. The narrative is wrong.

Not true.

When BTC drops overnight, the same hedgers buy at the open — you just don’t notice because it confirms the price direction you expected.

The pattern looks sell-only because BTC rallied more during Asia sessions than US hours through most of 2025. And even so, just 50-60% of the days open with a drop, the theoretical expected is 50%, so nothing out of the ordinary.

There’s also a subtler effect: even on flat nights, time decay (charm) shifts market makers delta. In a call-heavy market that means selling a small amount of hedge every morning just because a few hours passed.

@LarkDavis If you hedge (buy) with futures, someone needs to sell that position to you. That someone also needs to hedge, and will have to buy bitcoin. There’s no Bitcoin printing in regulated derivatives.

For every long interest there needs to be a corresponding short position.

@krugermacro@kale_abe Players need to delta-hedge their options exposure using Bitcoin ETFs at market open. If prices went up overnight, they need to sell, if prices went down, they need to buy. That’s basic price formation working, no manipulation.

No profit was “stolen.” Delta-hedging at market open is risk management, not a predatory strategy. The counterparties on perpetuals and derivatives chose to hold leveraged positions — that’s the risk they accepted.

As for spot price: in equilibrium, no — the rebalancing doesn’t suppress price structurally. It shifts demand from the open to other points in the day. The net buying/selling pressure over 24h is the same. What it does is create short-term volatility at predictable times, which hurts leveraged traders disproportionately. But that’s a leverage problem, not a manipulation problem.

If anything, the 10am rebalancing improves price discovery by transmitting overnight moves into the regulated market. The alternative — no ETF market makers adjusting positions — would mean wider spreads, worse execution, and less liquid markets for everyone.