Protect customers at every touchpoint. Banks, fintechs, and online retailers use Sardine to detect fraud patterns, stop money laundering, and prevent scams. 👇

Still buzzing from the 3 days we spent at @money2020 meeting our customers and partners.

And as I am sure many of you are, nursing a sore voice from the hundreds of conversations!

We hosted 3 events this year at our suite and are really grateful to everyone who took some time out of their busy schedules to spend some time with us:

- Faster Money Party with @FISGlobal, @airwallex, and @ActivantCapital

- Sponsor Banking Dinner with @Visa

- Fintech Nerd Fireside Chat with @sytaylor, @AlexH_Johnson and Colton Pond

Now on to the about 100 follow-up emails I have to write today

Excited to share some of the results from our work with @bunq's fraud team this year:

📉 82% reduction in fraud

🎯 4× fewer false positives

🙌 95% fewer fraud victims

When we first connected, Bunq’s fraud prevention team was running a strong program, but updating their rules was a slow and manual process. Each new pattern required specs, engineering time, and prioritization across teams. All of which made it tough to move as fast as new fraud trends.

With Sardine, that process now looks very different. When a new pattern shows up, Bunq can investigate and act in real-time. They use Sardine’s rules engine to create, test, and deploy rules in minutes (all without engineering resources).

And our device and behavior signals have helped them uncover hidden relationships between accounts, which has been a gamechanger for stopping coordinated attacks before they spread.

It’s a pleasure partnering with them to continue to raise the bar for fraud detection. Excited to see the results we achieve together next year 🙌

You can read more about our work with them here: https://t.co/zuUDz8kva8

A couple of months ago, @WarrenBuffett said fraud will be the biggest growth industry of all time, propelled by artificial intelligence. I 100% believe it - Trust is totally broken on the internet.

Is the website you’re visiting real? Did your CEO really send you that email? Is that really your board member dialing into the conference call?

Everywhere you look, AI has made it impossible to tell fraud from the real thing.

You can’t even trust your phone calls, facetime calls, or text messages.

This makes our jobs at risk professionals so challenging. Banking is built on relationships and trust. How is a “brand” anything but a consumer trusting that if they do business with you, they’re confident they’re going to receive something in return.

Security. Quality. Speed. Efficiency. Whatever it is, it’s built on trust. And now it’s broken.

So how do we bring trust back?

This is what we’ve been focused on fixing at Sardine, and what I recently gave a demo on at @nyca's Fintech Demo Day.

To win trust back from our customers, we need to evolve our fraud strategies so we’re not just playing defense. We need to go on the offensive.

If a fraudster clones your website, you need to know the moment it happens so your customer never loses a dime to that scam website.

If they try to sign up for an account, you need to be able to see what they’re doing on other platforms, how many devices or accounts they’re connected to, or whether they’re using tools to hide who they really are so you can stop them from getting through the gate.

Being able to see that data is a great start. But then we need to share our findings with other organizations, across many different industries. We need to work together so we can build herd immunity.

Data & consortiums.

Two things we spend a lot of time working on at Sardine, from our device and behavior SDK and data vendor partnerships to our work with Sonar connecting banks, fintechs, crypto, and players from every industry to benefit from each other’s data.

This is how we can actually figure out whether what we’re seeing is fake, stop it from impacting our customers, and preventing it from spreading across the ecosystem.

Because if there’s anything I’ve learned from scams it’s that it doesn’t happen on only one channel or platform. The scams work because they know we can’t see the full picture, and they know we’re not talking to each other.

The world is changing. Now is the time to start evolving the way we tackle fraud, so we can have a proper defense against today’s attacks.

If you want to see what that looks like, and how we’re helping our customers fight back, then send me a DM.

@sardine is here to help.

Nacha’s new fraud monitoring rules are coming into effect in a few months. 3 things should be thinking about:

1️⃣ 𝗖𝗮𝗻 𝘆𝗼𝘂 𝗱𝗲𝘁𝗲𝗰𝘁 𝘀𝗰𝗮𝗺𝘀?

This is one of the biggest changes. Nacha now explicitly requires monitoring for payments authorized under false pretenses.

That means banks will need to detect scams like business email compromise, payroll impersonation, and account takeovers, even when the customer approved the payment.

These scenarios have historically fallen outside Nacha’s fraud framework, but under the new rules, institutions are expected to identify behavioral and transactional red flags that suggest deception.

2️⃣ 𝗖𝗮𝗻 𝘆𝗼𝘂 𝗵𝗮𝗻𝗱𝗹𝗲 𝗶𝗻𝗱𝗲𝗽𝗲𝗻𝗱𝗲𝗻𝘁 𝗳𝗿𝗮𝘂𝗱 𝗺𝗼𝗻𝗶𝘁𝗼𝗿𝗶𝗻𝗴?

Many financial institutions have relied on their processors or upstream partners to handle fraud detection. Under Nacha’s new requirements, that won’t be enough.

Both originating and receiving institutions must have their own risk-based procedures in place to identify ACH entries that are unauthorized or authorized under false pretenses.

Nacha expects each participant to maintain documented processes and review them at least annually.

3️⃣ 𝗔𝗿𝗲 𝘆𝗼𝘂𝗿 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲 𝘁𝗲𝗮𝗺𝘀 𝗿𝗲𝗮𝗱𝘆 𝗳𝗼𝗿 𝗱𝗼𝘄𝗻𝘀𝘁𝗿𝗲𝗮𝗺 𝗶𝗺𝗽𝗮𝗰𝘁𝘀?

Traditionally, RDFIs have relied on originating banks to perform OFAC checks and have handled post-settlement screening through AML systems.

As institutions begin implementing risk-based monitoring for inbound ACH credits, they may uncover risks that weren’t visible before. This will likely increase alert volumes and false positives, adding to compliance workload.

Once AML alerts are triggered, compliance teams will need to ensure they’re reviewed and dispositioned properly.

---

We’ve broken down the new changes & what they mean for banks in our latest blog: https://t.co/A232uMmyWw

Money20/20 is around the corner, and we’re bringing the Sardine energy to Vegas.

We’ve booked out the Presidential Suite at The Palazzo again, and we’ll be hosting some VIP events you won’t want to miss, like our Faster Money Party and an exclusive fireside chat with @sytaylor and @AlexH_Johnson 👀

Schedule some time to meet our team, check out new product capabilities, and dive into some hot areas in risk & payments like:

- Deploying AI for fraud and AML

- Tackling deepfakes and AI-driven fraud

- Scaling faster payments without increasing risk

We look forward to seeing you there! https://t.co/YkxNd3uyMa

Grateful to our partners at @a16z and @GustoHQ for helping bring this SF @Techweek_ panel to life.

@snagpa, @soupsranjan, and @astrange dove deep into how AI agents are reshaping the fight against financial crime.

Happening now: a conversation on how AI is both accelerating and fighting financial crime with @soupsranjan from @sardine, Samant from @GustoHQ and @astrange from @a16z

We just launched a new AI Agent in our platform to assist in Customer Due Diligence (CDD) or Enhanced Due Diligence (EDD).

Today, compliance officers spend hours cross-referencing details:

- Business owner name vs. Company

- Company names vs. addresses

- Phone numbers vs. ownership records

- Even re-running sanctions checks against open web sources.

Our new AI CDD/EDD Agent does this instantly. It leverages LLMs and uses search as a tool to achieve the same thing that officers were doing manually. Behind the scenes, we are running all possible combinations of searches across the provided details until it finds satisfactory confidence level on Business and the Business Owner.

- Gathers company registration and ownership data

- Verifies addresses and contact info

- Screens for restricted categories (cannabis, gambling, firearms, etc.)

- Delivers a clear, compliance-ready report

This is the latest in our suite of AI Agents, against our goal to help Compliance Officers do their jobs faster and more efficiently. We’ll be launching more Agents in the coming weeks/months.

Let us know if there are other tasks where you are spending a lot of time?

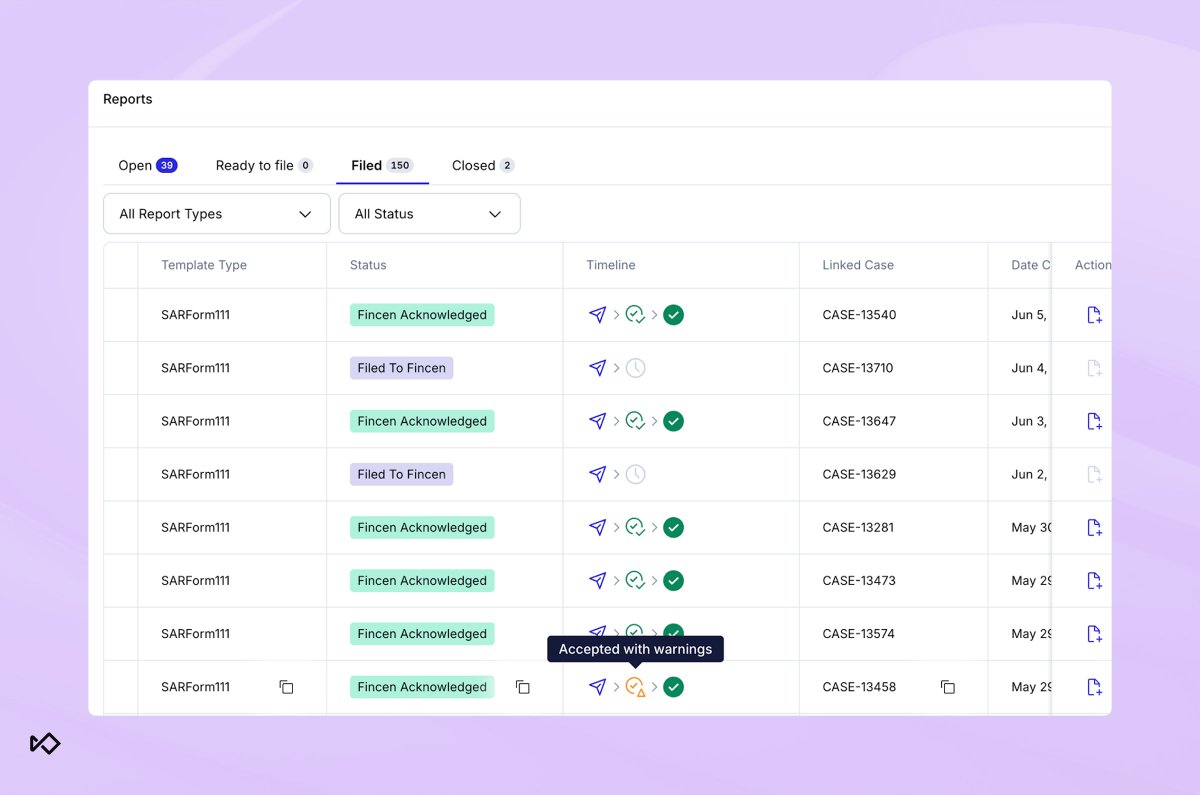

You file a SAR through BSA E-Filing and get the confirmation: received.

After that, updates live inside the portal.

If you want to know whether it was accepted, accepted with warnings, or rejected, you have to log in, search for the filing, and check the acknowledgments.

For one or two SARs a month, that is manageable.

For dozens or hundreds, it becomes a blind spot. And that blind spot can mean:

⚠️ Warnings sit unaddressed for weeks

⏳ Resubmission deadlines get missed

📂 Scramble to pull acknowledgment records

The SAR Lifecycle Tracker eliminates that manual chase.

It consolidates every FinCEN acknowledgment in one view so you can see the real-time status of each filing.

Every step is time-stamped and tied to a complete audit trail you can hand to a regulator.

From filing to follow-up, you always know exactly where things stand.

Contact us if you’d like to see our case management in action.

SMS pumping is one of the fastest growing fraud attacks in fintech today.

On the surface, it looks like new customer growth. In reality, fraudsters are exploiting OTP flows to trigger thousands of texts to premium-rate numbers they control.

The result: fake traffic, real invoices, and businesses stuck footing the bill.

The hardest part? Risk systems don’t flag it. There are no chargebacks, no customer complaints, no login failures. Everything looks clean until your SMS invoice suddenly spikes six figures.

Who gets hit the hardest:

- Fintechs and marketplaces, who absorb direct losses

- CPaaS providers, who face churn when customers push back

- Telcos, who lose trust in SMS as a channel

- Fraud and risk teams, who get blamed for a blind spot they never had tools to see

So how do you stop it?

✅ Limit velocity Block OTP requests hitting endpoints at machine speed.

✅ Spot automation Detect bot frameworks and emulators hiding behind clean traffic.

✅ Track completion ratios Real customers verify. Pumping attacks send without completing.

Full breakdown on how SMS pumping works and how to prevent it -> https://t.co/5J6WTO2Jqh

🤔 Are merchants mistaking AI agents for malicious bots?

We tried to buy a $4 tube of toothpaste online (for pickup) with ChatGPT Agent mode.

The checkout never made it past the fraud system. It wasn’t a payment issue. It wasn’t out-of-stock. The only “problem” was that the buyer was an AI agent.

Old world: Spot the bot, stop the fraud. New reality: The bot is the customer.

This is an issue most merchants are racing to figure out. The ones that update their fraud toolkit for this new world will own the next era of commerce.

But that will mean figuring out how to:

- Authenticate agents as legitimate buyers

- Bind user consent to agent actions

- Detect compromised or malicious agents

- Redesign step‑ups for non‑humans

- Adapt risk scoring to mixed human/agent journeys

We’ve laid out ways to adapt in our new whitepaper on agentic commerce.

🤔 Are merchants mistaking AI agents for malicious bots?

We tried to buy a $4 tube of toothpaste online (for pickup) with ChatGPT Agent mode.

The checkout never made it past the fraud system. It wasn’t a payment issue. It wasn’t out-of-stock. The only “problem” was that the buyer was an AI agent.

Old world: Spot the bot, stop the fraud. New reality: The bot is the customer.

This is an issue most merchants are racing to figure out. The ones that update their fraud toolkit for this new world will own the next era of commerce.

But that will mean figuring out how to:

- Authenticate agents as legitimate buyers

- Bind user consent to agent actions

- Detect compromised or malicious agents

- Redesign step‑ups for non‑humans

- Adapt risk scoring to mixed human/agent journeys

We’ve laid out ways to adapt in our new whitepaper on agentic commerce.

🐟 SardineCon 2025 is off to an incredible start.

Seeing the people who have stopped more than $100M in scams together in one room sharing their insights is a powerful reminder of why we built this event.

Your “verified” customer might not exist.

Deep-Live-Cam lets fraudsters pass video-based KYC checks using real-time deepfake faces.

They can blink, smile, turn their head, and match the photo on the ID they just uploaded. The whole session looks legitimate to an agent or automated system.

This is not Photoshop. It’s just one example of AI Fraud-as-a-Service.

These tools are sold on the dark web for anyone to use every day. In our blog, we outline 13 of these tools. But there are many more just like them.

Some of them get plugged up, but they operate like SaaS businesses and quickly ship updates, pivot to other exploits, and even offer customer support if a fraudster gets stuck.

So how do you fight back?

✅ 𝗟𝗮𝘆𝗲𝗿 𝗱𝗲𝘃𝗶𝗰𝗲 & 𝗯𝗲𝗵𝗮𝘃𝗶𝗼𝗿 𝘀𝗶𝗴𝗻𝗮𝗹𝘀 𝗶𝗻𝘁𝗼 𝗹𝗶𝘃𝗲𝗻𝗲𝘀𝘀 𝗰𝗵𝗲𝗰𝗸𝘀

Flag mobile emulators, VPNs, unusual phone movements, and copy-paste from long-term memory fields. These patterns often reveal a fake before the face does.

✅ 𝗗𝗲𝘁𝗲𝗰𝘁 𝗿𝗲𝗮𝗹-𝘁𝗶𝗺𝗲 𝗰𝗼𝗮𝗰𝗵𝗶𝗻𝗴

Watch for pauses, repeated entries, or mismatched typing patterns that suggest the user is being guided through verification by a fraudster.

✅ 𝗠𝗼𝗻𝗶𝘁𝗼𝗿 𝗮𝗰𝗿𝗼𝘀𝘀 𝘁𝗵𝗲 𝗰𝘂𝘀𝘁𝗼𝗺𝗲𝗿 𝗷𝗼𝘂𝗿𝗻𝗲𝘆

Link activity across devices, sessions, and channels so you can spot when a “verified” user is the same actor from a phishing or takeover attempt.

Full breakdown on how these scam tools work and how to stop them → https://t.co/jcHWc51zuv

Traditional KYC causes up to 30% sign-up abandonment

Why? Friction.

It starts off easy — name, DOB, tax ID… But then:

- "Please upload a photo of your passport or driver’s license."

- The user fumbles around to find it.

- Image not captured. Please re-upload.

- Crooked? Blurry? Wrong file type? Try again.

And if the customer happens to be named John Smith, good luck. Too many hits. Straight to the manual review pile.

Now an analyst has to dig through DOBs, middle initials, address history, trying to guess which out of the 150 John Smiths this is.

In the meantime, the customer’s been waiting for hours. Maybe days.

If they were signing up for a time-sensitive promo or a quick stock trade, that window has long gone and they might never come back.

So what’s the fix?

✅ eKYC that verifies identities in seconds

✅ Enriching identity with consortium data

✅ Using AI to resolves false positives instantly

✅ Passive risk scoring in the background with device & behavior

Not only does this reduce friction, it also opens the door for interesting optimizations.

Say if a user is low-risk, you can give them limited access to start transacting while your team reviews.

That could mean:

- Letting them buy up to $50 of stock

- Offering them a product walkthrough

- Showing app features without full activation

Better data = Faster UX, less friction, fewer drop offs, and shorter time to value

If you’re looking for a better way to manage global KYC, Sardine can help 👋🏼

👇 Link to breakdown in the replies