The dollar’s dominance may be slipping — and Europe might have an opening.

Our Chief DM, ex. US Strategist, @SavaryMathieu, explains how a Eurobond could help turn the euro into a true global reserve asset.

Okay, fine, let's be a little more like Sweden.

🇸🇪 1/3 of high schools are privately run

🇸🇪 taxes cut three years in a row

🇸🇪 public social spending has fallen as a % of GDP

🇸🇪 debt-to-GDP is 36%

🇸🇪 inflation-adjusted household income 2x since the '90s

Of course memory chip makers are making too much money. It’s called the capex boom-bust cycle.

Every infrastructure mania looks structurally justified at the peak because the underlying demand is usually real. Railroads, fiber, shale, LNG carriers, offshore rigs, vaccines, solar, lithium batteries & miners, and now DRAM, all had genuine fundamental stories underneath.

The mistake is rarely the demand thesis itself. The mistake is extrapolating scarcity economics and peak margins forever.

From the WSJ today:

“Sandisk and Micron are now generating around 80 cents of gross profit for every dollar of revenue. That compares with a wide range historically, from single digits to around 60 cents on the dollar. That seems unsustainably high for companies in the very expensive business of physically manufacturing chips.

But the unique nature of chip making also speaks to why the market conditions driving such profits won’t be changing anytime soon. Memory demand is growing sharply now, but new production facilities take years to build.”

That is exactly how every capex cycle feels near the top.

Phase 1: genuine bottleneck.

Phase 2: extraordinary margins.

Phase 3: capital markets fund massive expansion because everyone annualizes peak returns.

Phase 4: overcapacity, price wars, collapsing ROIC.

Phase 5: survivors consolidate and the industry becomes rational again.

The internet traffic forecasts in 1999 were ultimately correct, if not too conservative. The investment outcomes for many suppliers were catastrophic anyway.

Huge AI demand may absolutely be real and durable. The harder question is whether today’s scarcity economics survive innovation, efficiency gains and the inevitable capex race.

My view? They won’t. We are watching yet another textbook capex boom-bust cycle unfold in real time. As I said many times now, the bubble is usually in the “E” of the P/E. Always was.

Cisco, Corning, JDS Uniphase, Qualcomm, Intel, US Silica, Hi-Crush, Transocean, Seadrill, First Solar, SunPower, Moderna, BioNTech, Golar LNG, ZIM and now Micron, Broadcom, Nvidia & Sandisk.

Same movie. Different costumes.

As a European who left the “old continent”, that response by prof. @lugaricano rings true, sadly. There’s a reason why I feel better raising kids on the Western shores of the Atlantic: opportunities for their future.

We stopped everything to write an answer (link below) to Paul Krugman's two posts of today (one informal, one with a simple model) arguing that Europe is broadly not falling behind the United States.

The change measured by the Draghi report, he argues, is mostly due to growth in the technology industry, which has distorted GDP numbers without actually leading to higher standards of living. We should believe our eyes when we walk around France and walk around Mississippi.

Krugman is wrong. The measures he uses understate European stagnation. This matters enormously. Divergence with the United States is the strongest evidence for reform in Europe.

1. The growth numbers

Krugman compares the United States, France, and Germany at purchasing power parity in current prices. On that measure, France's and Germany's position relative to America has been roughly constant since 2000.

But current price comparisons miss productivity gains in sectors where prices fall. If America produces twice as much software while the price of each unit halves, the value of American software output looks unchanged even though the volume has doubled.

Most economists therefore use constant prices, which fix the base-year PPP level and apply each country's real output growth on top of it. American output growth has concentrated in tech, where prices have fallen tremendously as productivity rises. In terms of the volume of things produced, America has pulled away from Europe.

2. Is it all the tech industry?

Krugman concedes this tech divergence but says it is not welfare-relevant. The American growth lead is an accounting artefact of measuring more iPhones at base-year prices, not a sign that Americans are actually richer, because Europeans buy the same iPhones at the same world prices.

This is not the right way to think about the world today, as an earlier Paul Krugman would have argued.

His model assumes tradable goods, interchangeable workers, marginal-cost pricing, and no profits. Each assumption fails.

Most of what households buy is non-tradable: housing, healthcare, childcare, education. When American tech firms bid workers from haircutting to coding, American haircut wages rise. Germany has no growing tech sector to do the bidding, so German wages stay flat.

Technology is not priced at marginal cost. Apple's margins are around 40 percent. Anthropic's inference margins are at 70 percent. The major platforms enjoy network effects, switching costs, and lock-in that hold prices well above what a competitive market would deliver. A large share of the productivity gains in technology stays as profit.

A lot of the value of American technology dominance shows up in equity, not in wages. Apple, Microsoft, Nvidia, Alphabet, Meta, and Amazon together are worth $21 trillion, more than the entire combined stock market value of all European stock markets. Around 60 percent of US equity is held by American households. The median French or Spanish household holds almost no equity.

The median employee at Meta, a company with almost 80,000 employees, earned $388,000 in 2025.

This advantage is not going to go away. Krugman's own 1991 paper, cited in his Nobel prize, showed that comparative advantage in modern industries is produced by increasing returns to scale, specialized labor markets, supplier networks and the agglomeration of suppliers, workers, and ideas in particular places. Once an industry concentrates somewhere, the concentration is self-reinforcing. Europe is being pushed away from the next round of technology industries (AI!).

3. What about inequality?

Another retort is that GDP per capita hides substantial inequality, and so even if America is rich on average, this is mostly due to the super wealthy.

But despite the US's high pre-tax income inequality, it also achieves higher median incomes than Europe, in part because of such a high base, and in part because it actually redistributes more than many European countries.

The cleanest comparison is median equivalised disposable household income: income after cash taxes and transfers, adjusted for household size and purchasing power. According to the OECD's 2021 numbers, the median American earns 30 percent more than the median Dutchman, about 31 percent more than the median German, and about 52 percent more than the median Frenchman.

4. What about hours worked?

Krugman points out that while American GDP per person is higher, most of this is because Americans work more. For this divergence to be an hours worked story, Americans must work more relative to Europeans now than they did in 2000.

The opposite has happened. Birinci, Karabarbounis, and See in a 2026 NBER paper show that about half of the American-European hours gap that existed in the 1990s has reversed by the end of the 2010s. Americans work fewer hours per person than they did in 2000, while most Europeans work more.

5. Is America not a bad place to live?

Walk around Alabama and France: surely the former cannot be substantially richer than the latter?

American cities often have poorer centres and richer suburbs or exurbs. European cities preserve richer and more attractive historic cores. A visit to a city as a tourist in America compared with a city in France will leave one having seen different spots on the income distribution. Americans in Europe go to the nicest and richest European cities.

Rather than a walking around test, do a driving around test. Go to the periphery of any modern American city and see a level of new-built material wealth that is extremely uncommon in Europe, with thousands of enormous four- or five-bedroom homes. In the South, in places like Nashville and Austin, drive around the downtowns to see hundreds of luxury apartment buildings springing from the ground. This construction boom is replicated virtually nowhere in Europe today.

The other question is generational. Housing often costs more in Europe than in the United States, despite the quality of the housing stock generally being much better. Europe has nice city cores but these are inaccessible to young Europeans.

Consider the salaries available to entry-level workers. The starting pay for a London police officer is $57,000. In Washington, DC, $75,000. The entry-level Deloitte consultant job in Madrid pays around €28,000, roughly $33,000 per year. In Charlotte, the entry-level Deloitte job pays $63,000.

There are many things to dislike about life in America. But relative to 25 years ago, the gap in material wealth has shifted dramatically in America's favor.

https://t.co/VOpQ32R5tg

The Bond Market Is Forcing Washington To Choose

The U.S. bond market is not selling off because investors forgot about AI or overreacted to Iran.

It is selling off because fiscal dominance is colliding with an energy driven inflation shock.

That is the message behind the 30 year moving back above 5% and the 10 year pushing toward 4.50%. The long end is demanding more compensation for inflation risk, Treasury supply, fiscal stress, and policy uncertainty.

The Spark Is Oil

The immediate trigger is the Iran and Strait of Hormuz crisis.

Oil above $100 changes the Fed calculus. It keeps headline inflation sticky and pushes gasoline, diesel, freight, food distribution, utilities, insurance, and transportation costs higher.

The April CPI report already showed the pressure. Headline CPI rose 0.6% in one month. Energy rose 3.8%. Gasoline rose 5.4%. Energy was up 17.9% over the year. This is not clean disinflation. It is a supply shock moving through the cost structure of the real economy.

The Fire Is Fiscal

The deeper problem is that this oil shock is hitting a country already running huge deficits and issuing massive amounts of debt.

The U.S. is asking investors to absorb more Treasury supply while inflation volatility is rising and fiscal credibility is weakening. Investors are no longer willing to lock up capital for 10 to 30 years at low real yields just because Washington says everything is under control.

That is the return of term premium.

The Fed can control the front end. It can set the overnight rate. But it cannot force investors to buy long duration Treasuries at yields they no longer believe compensate them for inflation, deficits, and currency risk.

The 30 year above 5% is the bond market saying the fiscal path is no longer free.

The Fed May Need Demand Destruction

This is where it gets darker.

The Fed would never openly say it wants global demand destruction. But functionally, a controlled growth scare solves several problems at once.

If global demand weakens, oil demand cools. Commodity pressure eases. Inflation expectations soften. Long duration Treasuries catch a bid. Mortgage rates can fall. The dollar funding system stabilizes. And the Fed gets cover to cut without looking like it is surrendering to inflation.

That means the Fed may tolerate tighter financial conditions until demand destruction does part of the disinflationary work for them.

Not because they want pain.

Because the bond market will not give them an easy cut while oil is high, deficits are huge, and inflation is reaccelerating.

The Real Economy Is Already Weakening

This is dangerous because yields are not rising into a clean boom.

Real wages are already being squeezed. The April Real Earnings report showed nominal hourly earnings rose 0.2%, but CPI rose 0.6%, so real average hourly earnings fell 0.5%.

The paycheck got bigger.

The worker got poorer.

Housing is already strained. Mortgage rates near 7% freeze affordability.

Credit is tightening.

CRE is still rolling through refinancing stress.

Small businesses are under pressure.

Consumers are paying more for necessities while discretionary demand weakens underneath.

That is demand destruction in its early form.

Not a crash yet.

A squeeze.

My Take

The Fed is trapped.

If it cuts too soon, the bond market worries inflation and fiscal policy are not under control.

If it waits too long, higher oil, higher yields, falling real wages, frozen housing, and tighter credit turn the inflation shock into recession.

So the bond market is forcing Washington to choose.

Lower energy pressure.

Fiscal discipline.

Liquidity support.

Or a growth scare large enough to bring back the Treasury bid.

This is not an apocalyptic bond collapse yet.

But it is a serious warning shot.

The danger is not just that yields rise.

The danger is that yields rise while the economy is already losing its ability to carry them.

De Guindos is damn right to call out Merz. Germany has no issue when German firms buy foreign ones. UniCredit is a solid bank, blocking this transaction is ridiculous, given the need to consolidate Europe’s banking system. Consolidation is a necessary step to move toward the SIU supported by all the European institutions. An SIU is key to help revive European risk taking and trend growth. Shame.

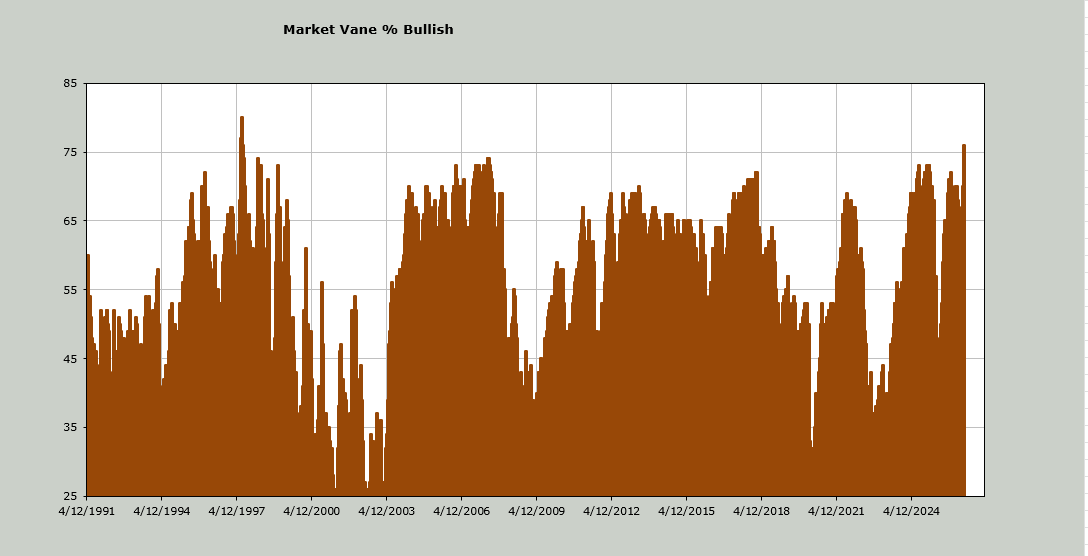

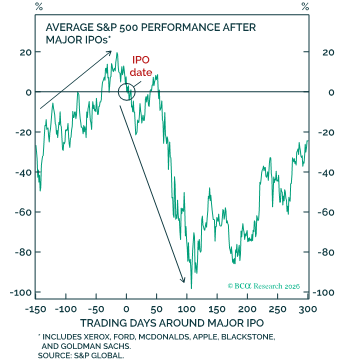

It's tough to throw me off my current bullish bias, even with Hormuz still closed. But a Monster IPO might do the trick. Beware the coming IPO-Palooza.

Great article by prof @lugaricano

First, very creative way to look at the impact of the Ukraine war on economic policy in the EU. Second, very worrisome conclusion for the implementations of the reforms needed at the core, such as the SIU and the modernization of the EU economy. As long as Europe’s pension problem remains politically unaddressable, Europe will trail.

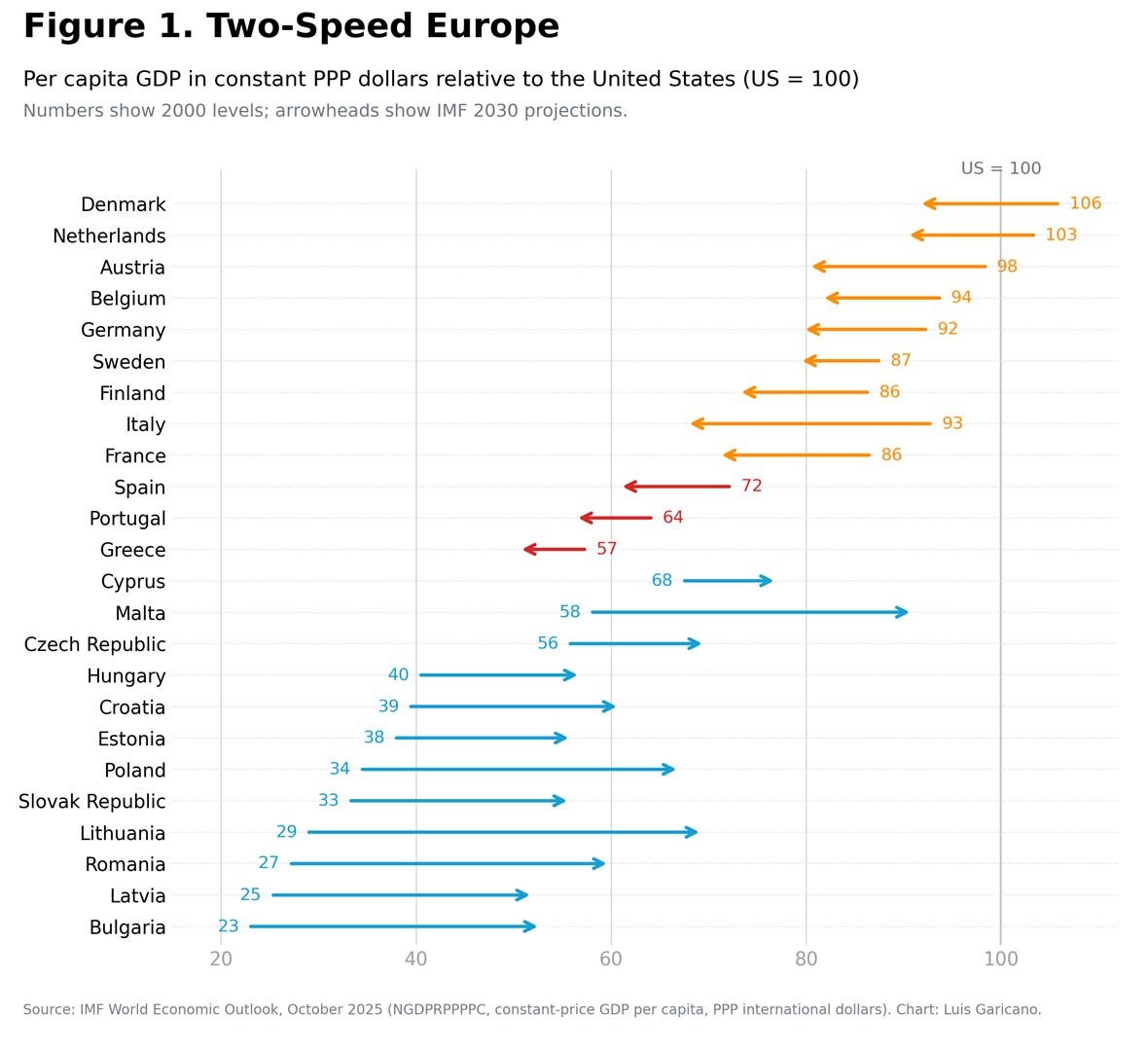

New post out!: The two Europes: why the security shock is deepening Europe's economic divide.

Europe is divided in two: the chart shows a positive convergence story and a divergence story. Poland went from 34% of US per capita GDP in 2000 to a projected 67% by 2030. Romania from 27% to 60%. France dropped from 86% to 71%. Italy from 93% to 68%.

The EU is not one economy moving slowly. It is two economies moving in opposite directions.

The hope after Draghi was that the Russian threat would supply the political urgency the rear of Europe lacks. The correlation is the wrong one. Our analysis shows the shock is mobilising the countries where the Draghi problem is not most severe, and leaving the rest largely untouched. War is reforming Europe's frontier. It is not reforming its rear.

New post with @OlivierKooi.

https://t.co/U04xw4aVOr

Could not agree more with @Globalflows. Liquidity is ample nearly everywhere around the globe. From China, to the US, Europe and Japan. No wonder stocks barely responded to the SoH closure. That will last until inflation comes back, potentially next year. Until then, let them cook.

Equities are just going to keep melting up

I don't make the rules, I just follow the flows

Everything on the credit cycle was laid out

Liquidity is NOT contracting

My expectation is that commodity currencies are the ones with most upside. the SoH closure, after supply chains chocks during covid and during the Ukraine war, has put supply security front and center. Hence, I expected exposure to those currencies, with comparatively lower turnover, to have the largest impact.

"The dollar isn't disappearing, but its dominance is."

Our Chief DM ex-US Strategist @SavaryMathieu breaks down why the global monetary system is shifting from a dollar-dominated framework to a multi-anchor regime, and what that means for investors.

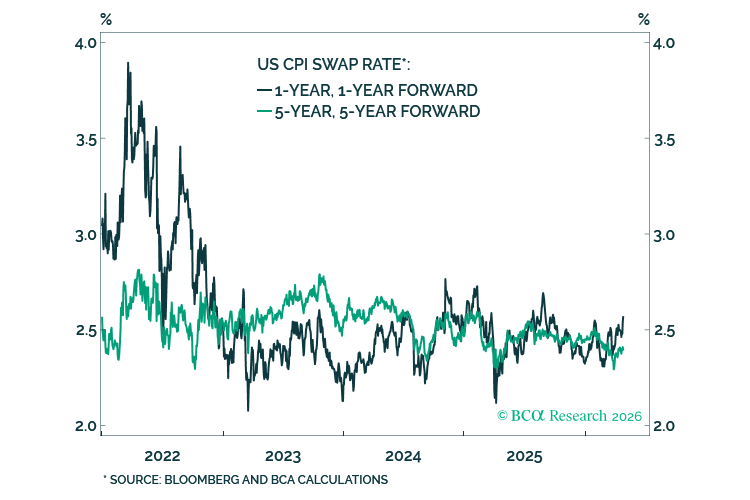

Although they remain very far from 2022 levels, it is notable that 1-year/1-year forward US CPI swap rates are picking up. US gasoline prices remain above $4/gallon going into the summer driving season. If the White House wants to salvage their midterms odds, they must act soon.

@ManuelSamuel is absolutely right. The immediate dynamics in Europe are vastly different from 2022. And yes, the real risk is that policymakers continue to do nothing on integration, rules harmonization, energy policy and so forth, extending the past lost decade into another one.

The Recession Debate Misses Europe’s Bigger Problem

Robin Brooks is right to worry: Europe is at stall speed. But this is not simply 2022 redux. Gas dependence on Russia is far lower, labour markets remain resilient and policy buffers exist. The bigger danger is not a sudden recession — it is Europe normalising near-zero growth as a geoeconomic condition.