📢 Call for Papers — 2 days left

The 2nd International Conference of the Georgian Economic Association will take place in Tbilisi 🇬🇪 on June 26–27, 2026.

Join us in the beautiful city of Tbilisi for two days of academic exchange and collaboration.

We are honored to welcome Ruben Enikolopov and Joseph Kaboski as plenary speakers.

⏳ Submission deadline: April 10

📄 Submit your paper:

https://t.co/qGSMZgnOUL

More information: https://t.co/nJPtmCH8xU

#EconTwitter #CallForPapers #GEA #Tbilisi #AcademicConference

In their OxREP response to @benbernanke’s analysis of the BoE, @laxton_douglas, Haykaz Igityan, and @ShalvaMk call for a rethinking of monetary policy. They emphasise the interplay between credibility, risk management, and macroeconomic stability. https://t.co/f2znjpiH22

A closer look at banks’ business models from the International Monetary Fund promises an improvement to traditional macroeconomic models https://t.co/hWome0orKu

@NBGeorgia welcomes paper submissions for the NBG Research Conference 2024 in December: "Shaping the Future of Monetary Policy".

Our keynote speakers: Robert Tetlow (@federalreserve), Athanasios Orphanides (@MIT), and Tobias Adrian (@IMFNews).

Details: https://t.co/UT0CFdCY08

Economics students who want to understand how MONEY CREATION works from a practitioner’s perspective, here are my two long lectures for @PolicyBetter summer school:

(1) Central Bank Liquidity and Money Creation in the Real World. https://t.co/BYigVZOnC2

(2) Monetary Policy Transmission and Operational Framework https://t.co/xmX6N8HiG8

Hosted a panel on current economic challenges & opportunities in 🇬🇪 with top economists from Tbilisi & Brussels: Eva Bochorishvili, Galt & Taggart, Miguel Sanchez Martin, World Bank, @AkhvledianiTina, CEPS, @ShalvaMk, NBG, @DavitKeshelava & @tamar_sulukhia , ISET

Being conscious of those potential "side effects" of FXI (on liquidity risk premia and broad money) may better inform EMDE policy-making.

Last but not least, thanks to Már Guðmundsson, Martin Galstyan and @christiano3 for a great discussion, moderated by @JonSteinsson.

15/15

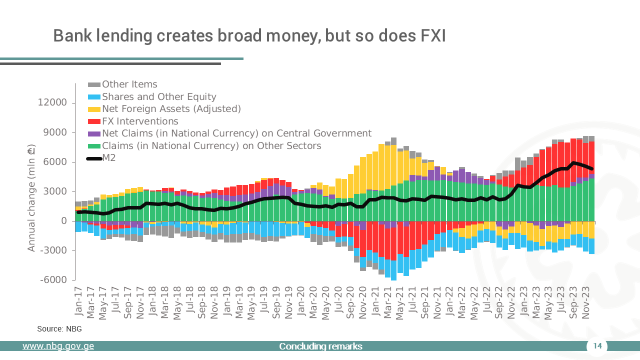

Is this consideration of FXI quantitatively large?

Decomposition of M2 broad money change shown below, based on accounting identities:

In Georgia FXI (red bars) sometimes has generated as much broad money as bank lending, key source of money creation, has (green bars).

13/15

My remarks on FXI were based on our recent paper, forthcoming in the International Journal of Central Banking (#IJCB).

Available here: https://t.co/3AvVWvxmCQ

14/15

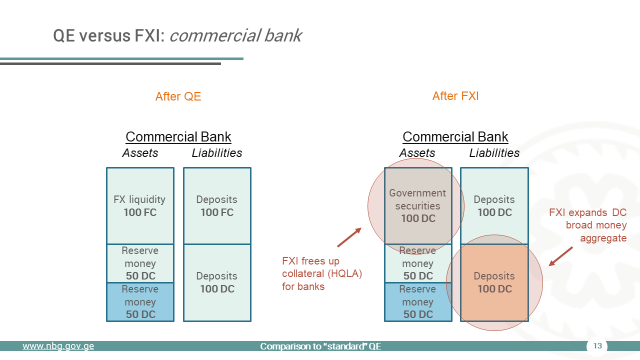

1) after FXI the bank has securities AND additional reserves: ₾ HQLA, relative to ₾100 after QE, increases to ₾200 after FXI = ₾ liquidity risk premia decline.

2) ₾ broad money expands as the bank's forced to issue more of ₾ deposits to "buy FX" / close FX position.

12/15

Not much of a difference when it comes to the CB reserve (liquidity) supply.

Hence, short-term money market rates may indeed NOT be different (i.e. sterilization can easily achieve its objective).

But there are two significant difference in the bank's balance sheet.

11/15

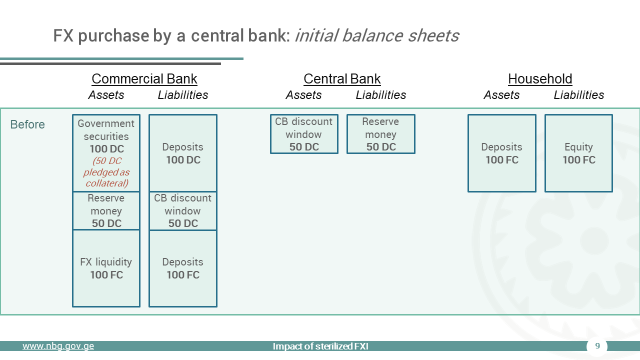

Below is how balance sheets look like after FXI.

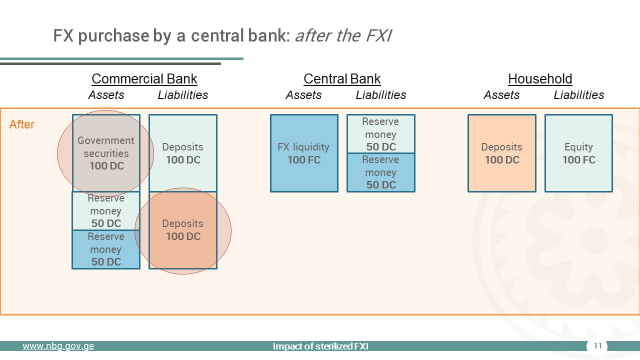

In a nutshell, a difference between FXI and QE is that when the CB buys FX, indirectly, it is buying it from a non-financial sector, because they are the ones that usually have open FX positions.

What are the implications?

10/15

What's different here is that when the CB buys FX from the bank, the bank opens an FX position, which it is required by regulation to close again. How?

The usual way of closing it would be for the bank to issue ₾ deposits and buy back $ deposits of households/corporates.

9/15

Last week I participated in a panel discussion within a high-level economic conference exceptionally organized by @centralbank_is and @NorthwesternU in Reykjavík, Iceland.

Despite my subject-specific topic (FXI), given the current situation in #Georgia, the only place I could start off my discussion from was a genuine thank you to the #EU, represented by my EU peers at the conference, and to show an appreciation for their continued support to Georgia in these challenging times.

The rest of my talk was about potential, usually under-looked, "side effects" of sterilized FX interventions (#FXI):

1/15

Is the effect of FXI similar? After all, it is also a type of an asset purchase. Well, it's not exactly similar.

Let's assume the balance sheets before FXI are the same as in our QE example right before QE. But here the CB will exchange $ liquidity instead from the bank.

8/15

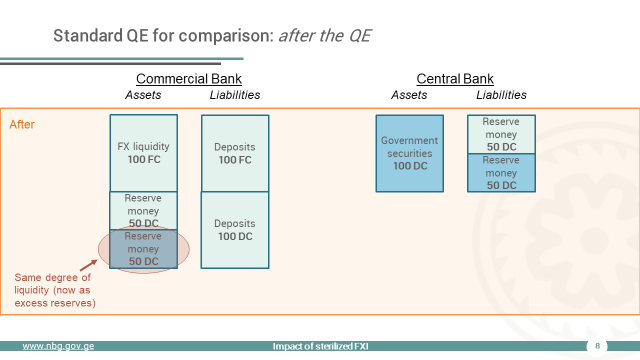

After QE the bank has the same amount of HQLA (₾100), only its composition's changed:

it was getting longer-term yield on securities; now it's earning short-term rate on excess reserves.

This just changes the term premium (the bank's compensation for interest rate risk).

7/15

Then the CB buys ₾100 securities (QE), funded by creating the same amount of new reserves. This involves the bank paying off the CB discount borrowing.

What are the effects of such an operation from the CB? It's mostly just about the term premium.

6/15

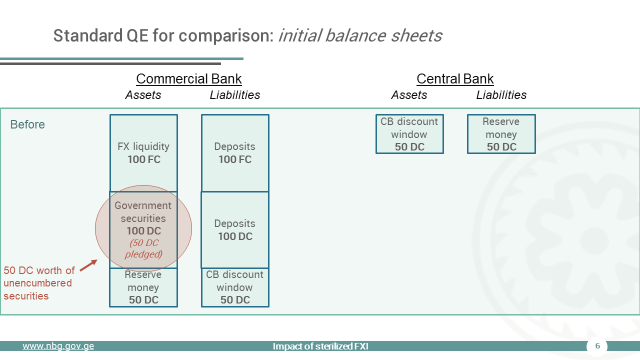

The bank has DC (₾) and FC ($) deposits, and liquidity in the same currencies.

It has ₾100 worth of securities, but ₾50 is pledged at the CB to get ₾50 reserves. ₾ high quality liquid assets (HQLA) is ₾100 for the bank (₾50 reserves + ₾50 unencumbered securities).

5/15

To drive those two points home, I first showed how standard QE affects the central bank (the CB) and a commercial bank (the bank) balance sheets, later to be contrasted with FXI.

Let's assume the initial balance sheets look like the following:

4/15

These two were my main "novel"/under-looked points:

1) long-term domestic currency interest rates may still be affected by even sterilized FXI.

2) domestic currency broad money may still be affected by even by sterilized FXI.

3/15

It's widely believed that when FXI is sterilized, it has NO impact on domestic currency interest rates. Is that always the case?

It depends on which interest rate you are looking at: short-term rates may indeed not change (as in the graph below), but long-term ones may do!

2/15