Thoughts on $TSLA

$TSLA is clearly no longer just a car company and this report makes that obvious. Musk is basically walking on water right now. The fact that he’s building autos, energy, AI, robotics, and a Robotaxi network all at once while still producing serious free cash flow is something you almost never see in business. And yeah, people are going to point to the PE and say it’s expensive, but that completely misses what’s actually going on here. Quite frankly, that argument is moronic and shows a lack of understanding of what’s being built.

Most companies struggle to do one thing well. $TSLA is trying to solve manufacturing, energy, autonomy, AI infrastructure, robotics, and fleet economics all at once. And somehow it’s still generating billions in free cash flow. That’s not normal, it’s not even comparable.

They’re scaling the core auto business, building energy, and at the same time pouring capital into AI and autonomy. This is an entirely different economic model. The bet is simple, give up near term margins to build something that looks more like software later.

Revenue was $22b, up 16%. That came from more deliveries, services up 42%, better pricing, and more FSD revenue. But not all of it was perfect. Energy was down and regulatory credits fell, so the growth was still good, but mixed.

Profitability improved, but let’s not pretend this looks like a software company yet. Operating income was about $900m with a 4.2% margin and $500m in net income. Margins are moving up, but they’re still low relative to what this business could become.

The reason is obvious. They’re spending heavily on AI, R&D, and infrastructure, and SBC is still elevated. That’s their strategy, and they’re deliberately compressing margins today to build something much bigger over time.

Cash flow is what matters most because they generated roughly $4b in operating cash flow and $1.4b in free cash flow. That’s very impressive, but they’re also spending $2.5b on capex and invested $2b into SpaceX. This is still a capital heavy business today, even if the long term goal is to become asset light.

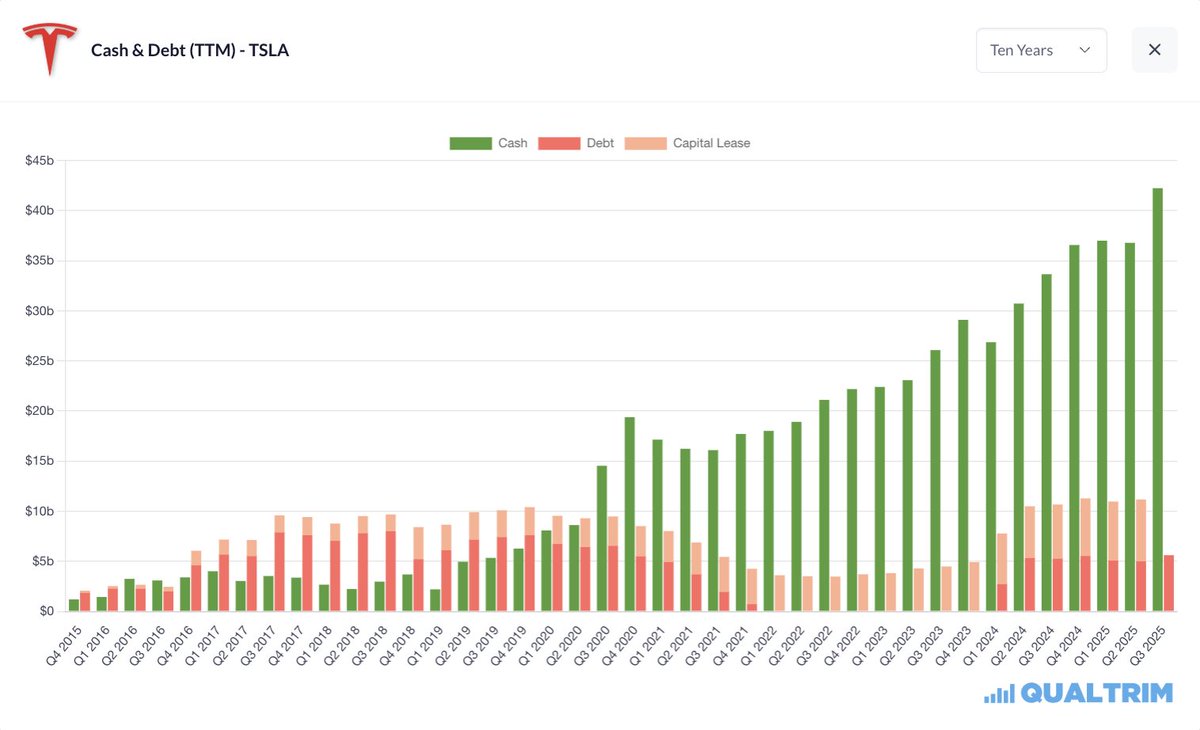

The balance sheet is what makes all of this possible. Around $45b in cash and a massive asset base. That gives them time, and time is everything when you’re trying to build something this ambitious.

Every dollar $TSLA generates isn’t being returned, it’s being redeployed into AI compute, factories, and vertical integration. This isn’t a company optimizing earnings, it’s a company allocating capital into optionality. The question isn’t margins today, it’s what those dollars earn over the next decade.

This quarter, operations were a bit more mixed. Deliveries were 358k, up 6%, while production was 408k, up 13%. Inventory moved up to 27 days. That’s not alarming, but it tells you demand isn’t running away from them anymore. They are no longer supply constrained.

FSD is my favorite part of the report. Subscriptions hit 1.28m, up 51%. That’s a huge deal because it is an early signal of the shift from selling a car once to monetizing it over time. If that works, the entire model changes drastically.

At 1.28m subscribers, even modest pricing starts to matter big time. At $100 a month, that’s roughly $1.5b a year. Scale that across tens of millions of vehicles and the numbers start to get enormous. This is how a car company slowly becomes a software company.

Energy had a weak quarter with storage down 15%, but I wouldn’t overreact. This business is lumpy and new capacity is coming online. Longer term, it’s still a meaningful growth driver.

Meanwhile, the infrastructure keeps getting stronger. The Supercharger network is growing close to 20% with over 8,400 stations and roughly 80,000 connectors. People don’t talk about this enough, but it’s a huge advantage.

1/2 👇

Optimus will be the biggest product ever made.

A general-purpose humanoid robot that can do useful work at scale will change the economics of labor & manufacturing.

Goal is to get Optimus to high-volume production as fast as possible.

If you’re great at AI, engineering, or manufacturing & want to build this, join us!

→ https://t.co/s3YW8Z6tZO

Q4 Shareholder Update → https://t.co/u0UcDOuMNa

— Highlights

2025 marked a critical year for Tesla as we further expanded our mission & continued our transition from a hardware-centric business to a physical AI company.

We also laid the foundation for the future of Tesla by further advancing FSD Supervised, launching our Robotaxi service, beginning to install production lines for Cybercab & fine-tuned our production-primed Optimus design while expanding our AI training infrastructure.

In 2026, we will further invest in the infrastructure needed to support clean energy + transport as well as autonomous robots.

This includes the ramp of 6 new production lines across vehicle, robots, energy storage & battery manufacturing.

We're building a world of amazing abundance. LFG!

Automotive

– APAC region continues to show strength across multiple markets & set a record for deliveries this quarter

– Preparations in North America continue for the production ramps of Tesla Semi & Cybercab, both commencing in the first half of 2026 & production of the next gen Roadster

Energy generation + storage

– Highest quarterly energy storage deployments, driven by record Megapack deployments

– Total gross profit = $1.1 billion, marking our 5th consecutive record quarter!

– Megapack 3 & Megablock production starting at Megafactory Houston this year

– In 2025, Powerwall network supported more than 89k Virtual Power Plant events across >1 million installed units, saving homeowners >$1 billion in electricity bills

Robotics

– Planning to unveil Optimus Gen 3 in Q1 this year, our first design meant for mass production

– Start of production planned by end of 2026, with eventual planned capacity of 1 million robots/year

AI Training Compute

– Currently building Cortex 2 at Giga Texas to further increase our AI training compute capacity

– In the first half of 2026, we're planning to more than double the size of onsite compute in Texas (in terms of H100 equivalents)

Battery

– Our lithium refinery started pilot production. It is the first spodumene to lithium hydroxide refinery in North America, with a simpler, cheaper & more environmentally friendly process

– Started producing battery packs for certain Model Ys with our 4680 cells, unlocking an additional vector of supply

– We now produce dry electrode for 4680 cells with both anode + cathode made in Austin

– We expect both domestic cathode material in Austin & LFP lines in Nevada to begin production this year

AI Software

– Shipped latest version of FSD Supervised (V14), which will drive you to your destination, find a free spot & park

AI Inference Compute

– Development of our in-house, custom designed AI5 & AI6 inference chips for autonomy progressed during Q4, with production planned for 2027 & 2028 respectively

– Targeting a 50x improvement for AI5 compared to AI4, thanks to 10x raw compute, 9x memory capacity & 5x hardened block quantization & softmax function (= enabling efficient low precision computing without sacrificing model accuracy)

Automotive + Other Software

– Robotaxi app no longer has a waitlist in the areas we serve

– Our vehicles keep getting better with over-the-air software updates: Grok w/ navigation commands, Photobooth, Supercharger Site Maps, Automatic HOV Routing, & more

Robotaxi

– Began testing driverless Robotaxis in Austin in December & began removing safety monitor from customer rides in January

– Our Bay Area ridehailing service now serves SJC, with plans to expand to other Bay Area airports upon receiving required permitting

– Cumulative paid Robotaxi miles have now exceeded 600k

FSD Supervised

– Launched in Korea, where customers drove >1 million kilometers in just one month

– We continue to pursue regulatory approval in China & Europe

– FSD Supervised subscriptions more than doubled in 2025

BREAKING: Tesla has officially started FSD Unsupervised Robotaxi rides for the general public in Austin with no safety monitors in the car, marking a historic milestone for the company.

Congrats @Tesla team!

🚨 Tesla has brought the largest lithium refinery in the U.S. online.

This is vertical integration at its finest!

Fewer middlemen, tighter margins, and more control over the EV supply chain.

Big long-term advantage for $TSLA 🚀

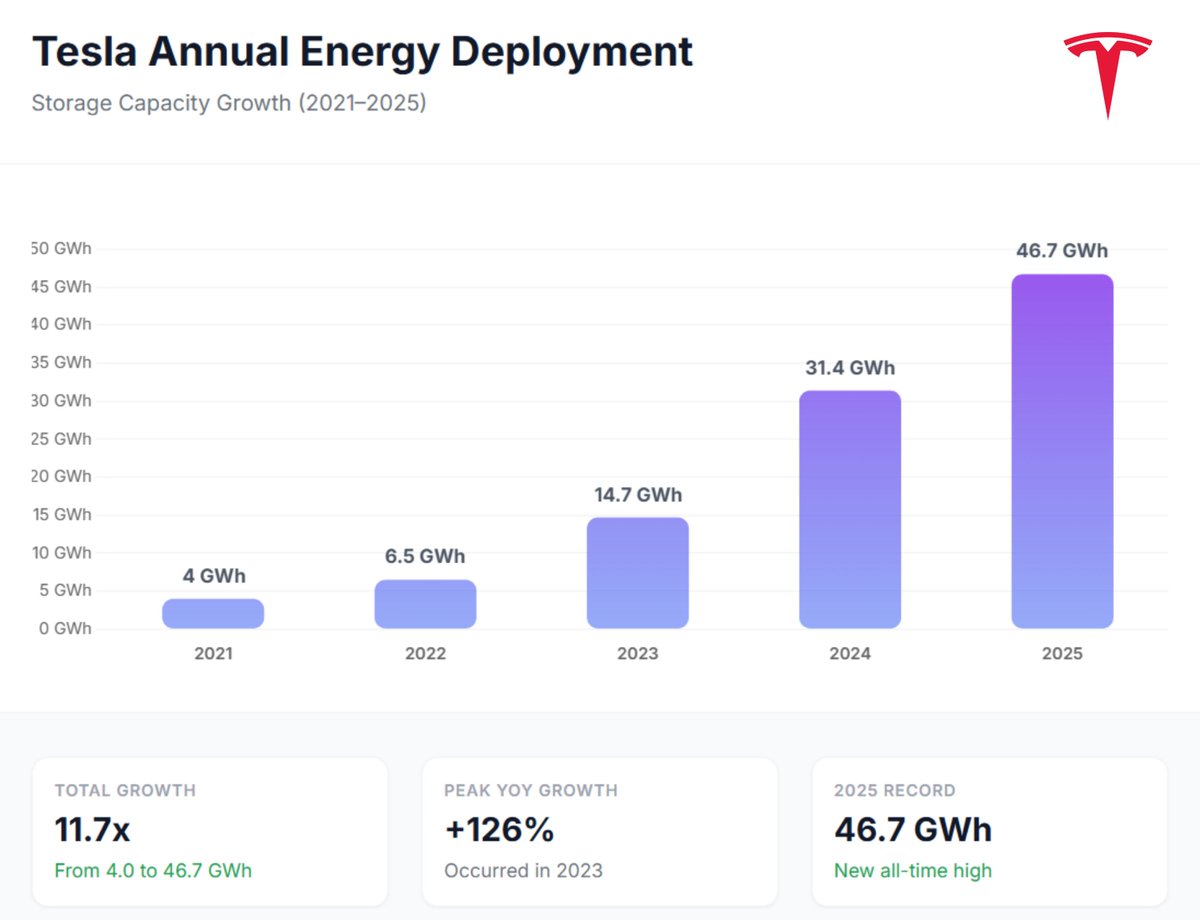

Tesla Energy is now the largest energy storage provider in the world

~46.7 GWh deployed in 2025 alone, powered by Megafactories in Lathrop and Shanghai

From ~4 GWh in 2021 to ~47 GWh in 2025

Nearly 12× growth in four years

Tesla now holds ~15–20% of global grid-scale battery storage

That’s enough energy to power Las Vegas for about 5 days straight

Grid-scale storage is scaling fast

TW-scale energy storage is getting closer to reality

The only reason $TSLA was at this price in 2025 is because people were selling at this price...

...in 2025.

...just prior to Robotaxi launch.

...which Tesla told us would happen.

...and which we could see was inevitable by watching what FSD was capable of & rate of progress.

Just think about that.

Every day, we're working towards making sure everyone can get any good or service they want without sacrificing our resources.

This is sustainable abundance.

To achieve this, our products must be accessible to all

Tesla has all the pieces: AI tech + electrical-mechanical engineering + scalable production lines. No one else has that.

Tesla autonomous driving might spread faster than any technology ever.

The hardware foundations have been laid for such a long time that a software update enables self-driving for millions of pre-existing cars in a short period of time.