I get the frustration — no one wants prime farmland turned into industrial estates, or households subsidising hyperscalers’ power & water while bills rise. Local campaigns have valid points on landscapes.

But data centres aren’t optional luxuries. They’re the new electricity grid, ports & motorways for the 21st century economy. UK already gets ~£4.7bn GVA/year from them, with potential +£44bn by 2035 + tens of thousands of jobs. Without domestic compute, we offshore sovereignty, AI innovation & security to US/China clouds.

Better path:

• Prioritise brownfield/industrial sites & AI Growth Zones (e.g. Culham with nuclear pairing via SMRs). https://t.co/T3PPeDfpDQ

• Force efficiency (advanced cooling, waste heat reuse, full cost recovery on grid).

• Pair with new nuclear/renewables so it’s not robbing Peter (households) to pay Paul (AI).

Stagnation isn’t sovereignty — it’s managed decline. Compete smartly, or fall behind while still using the tech. Power for the people includes building the infrastructure that keeps Britain competitive.

What alternative do you see for UK data sovereignty & growth?

@NoFarmsNoFoods It would also further damage the population’s health! The CCC works against the interests of the British people in many ways - they are what needs decimating

@AutismCapital@Simon_Breezer I go in a lot of houses and can generalise as follows: people who want shoes off are uptight and have no joy in their lives; people who don’t mind shoes are well adjusted, happy, and possibly have a dog.

Whether you are from the left or the right, watch this. @LiamHalligan is brilliant and entirely right.

If you are not for a massive slashing of the state, you should be nowhere near politics because you are for the economic destruction of our country.

Which political party is awake to this in the UK? If we wait until the next elections we’re going to be so far behind that we’ll never catch up. What do you think @RestoreBritain_

Tell me more about this global market price, and how it allows for massive differences in prices around the globe: Wholesale (spot or front-month futures) natural gas prices vary significantly around the world due to regional supply-demand dynamics, infrastructure constraints, and geopolitical factors. As of mid-March 2026 (around March 13-15), prices reflect ongoing volatility from Middle East tensions (e.g., impacts on Qatar LNG and Hormuz flows), which have driven European and Asian benchmarks higher while the U.S. remains low due to abundant domestic production.

The most common unit for comparison is **USD per million British thermal units (MMBtu)**, though some benchmarks quote in local currencies or per MWh. Here's a sample list of key wholesale benchmarks (primarily front-month or spot prices, approximate as of early-mid March 2026):

- **United States (Henry Hub)**: ~$3.13–3.25/MMBtu (NYMEX futures settlement around $3.13 on March 13; spot similar at ~$3.13–3.25). This remains the lowest major benchmark, supported by high shale output and storage levels, with limited export pull despite global disruptions.

- **Europe (Dutch TTF benchmark, Netherlands/continental Europe)**: ~$18–20/MMBtu (equivalent to ~€50–52/MWh; front-month around €50.12/MWh on March 13, or roughly $18–19/MMBtu using approximate conversion and exchange rates). Prices surged earlier in March (up to ~$18.5/MMBtu) due to supply concerns from Qatar stoppages and Middle East escalation, but eased slightly by mid-month.

- **United Kingdom (NBP - National Balancing Point)**: ~$18–20/MMBtu (front-month around 127–129 GBp/therm on March 13; equivalent to roughly $18–19/MMBtu). NBP closely tracks TTF but can show slight premiums or discounts due to UK-specific interconnectors, LNG access, and domestic factors; recent levels reflect similar volatility to Europe, with a monthly surge of over 76% amid global supply risks.

- **Asia (JKM - Japan Korea Marker, spot LNG benchmark)**: Low-$20s/MMBtu (April delivery assessed in early March; surged from high-teens to low-20s/MMBtu by March 6 amid Middle East tensions and competition for Atlantic Basin cargoes). This premium over Europe reflects strong Asian demand pull and higher shipping costs for LNG.

### Key Observations

- The U.S. (Henry Hub) trades at roughly 1/5–1/6 the level of European/Asian benchmarks, highlighting the regional nature of gas markets.

- Europe (TTF) and the UK (NBP) are closely aligned (~$18–20/MMBtu), benefiting from interconnected pipelines but vulnerable to import disruptions.

- Asia (JKM) often commands the highest prices due to heavy LNG reliance and no major pipeline alternatives.

- Conversions: 1 MMBtu ≈ 293 kWh; €1/MWh ≈ $0.35–0.37/MMBtu (varies with FX); GBp/therm ≈ specific conversion to MMBtu (~1 therm ≈ 0.1 MMBtu, adjusted for pence to dollars).

These are snapshots—prices fluctuate daily (e.g., intraday swings from weather, news, or storage reports). The stark differences (U.S. low vs. Europe/Asia elevated) underscore why claims of a uniform "global price" are misleading for natural gas, unlike more fungible oil.

@ZoeJardiniere@labourpress@paulmasonnews What is their fair share? Can you quantify it, or do you just use it as a sound bite? Do you know what share they pay already?

Because it will force people to sell their cars and buy a bike instead. We’ll then be able to invest the savings in a pension, through which the government will spaff the money on windmills - part of a strategy that will lead to rolling blackouts within 5 years. This will lead to a further cost of living reduction, as they can’t charge for electricity that has been turned off! He’s really thought this through, you know!

@mgshanks Subsidising a sector that can’t otherwise make a profit, in order to create economically unproductive jobs, is theft from the taxpayer, inflationary and making the poor and middle class poorer

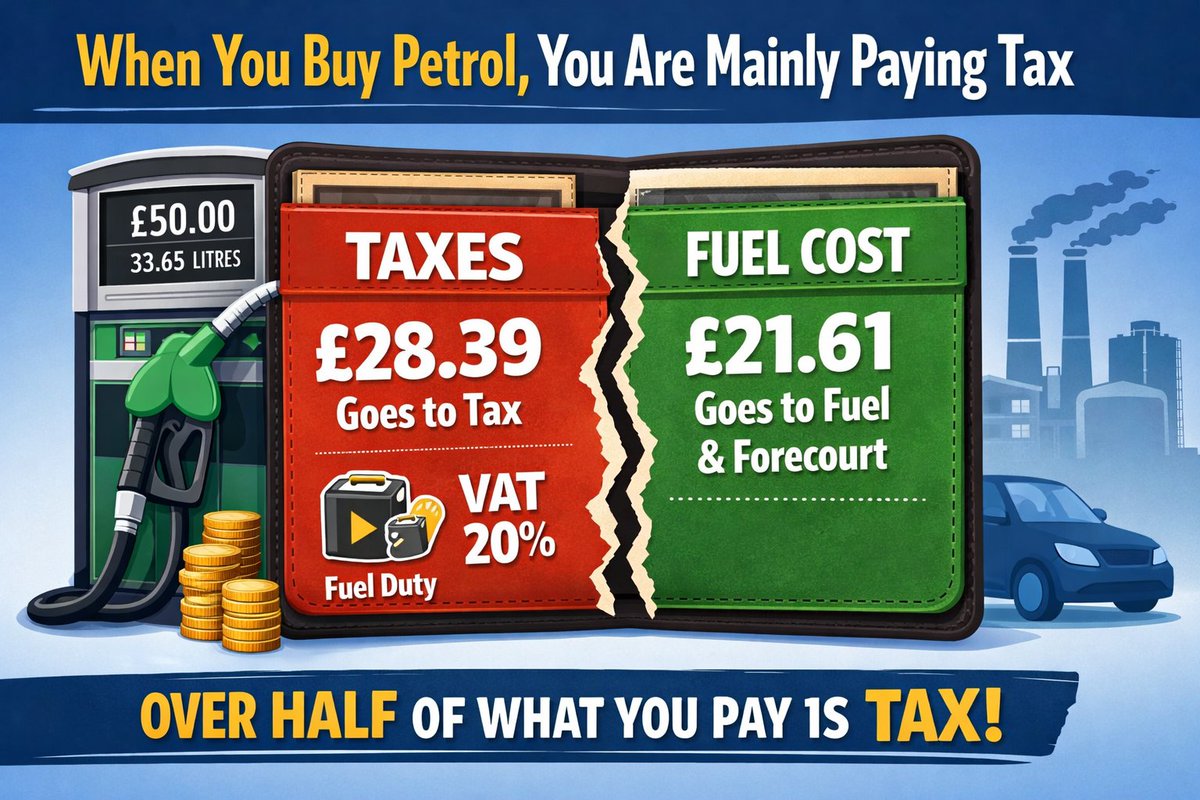

Spend £50 on petrol & £27.16 (54.3%) is taken by Rachel Reeves & the remaining £22.84 is the underlying fuel/retail cost before tax

After Labour's 8p per litre tax increase by next April, £28.39 (56.8%) will go to tax & £21.61 to the underlying fuel/retail cost.

Fuel in Britain is mainly a tax payment. If Labour is serious about reducing the cost of fuel, they need to cut tax on fuel. A lot.

@JeremyClarkson@DeAthCardiff A cabinet member for climate change must perpetuate climate alarmism, otherwise he’d have no reason to claim taxpayer money for his self promotion

“Everything worked” in the 70s!!! You weren’t there, were you! Reality of the decade is:

The 1970s saw the UK grappling with **stagflation** — a toxic mix of high inflation, stagnant or negative economic growth, and rising unemployment — something largely unprecedented in the post-war era. Inflation was a major problem:

- It averaged over 13% annually across the decade.

- It peaked at around **24-27%** in 1975 (depending on the measure, like RPI).

- Other spikes occurred in the early 1970s and around 1980, driven by factors like the 1973 oil crisis (OPEC embargo tripling oil prices), wage-price spirals, loose monetary policy earlier in the decade, and sterling devaluations.

This led to repeated government attempts at incomes policies (voluntary or imposed wage controls) to curb inflation, but these often broke down amid union resistance.

Unemployment also rose sharply compared to the 1950s-1960s "golden age" of near-full employment (~2-3%). It climbed above 1 million for the first time since the 1930s by the early 1970s, reaching 5-6% by the late decade — high for the time.

The economy experienced recessions, notably in 1973-1975 (with GDP declining significantly in places), and required an **IMF bailout** in 1976 under Labour PM James Callaghan to stabilize the pound and public finances amid a balance-of-payments crisis.

The most infamous episode was the **Winter of Discontent** (late 1978 to early 1979): widespread public and private sector strikes over pay limits imposed to fight inflation. This caused major disruptions, including uncollected rubbish piling up on streets, hospital closures or limited services, limited burials, and power issues in some areas. It contributed heavily to the fall of the Callaghan government and Margaret Thatcher's 1979 election victory.

Regarding **state-run institutions** (nationalized industries like British Rail, British Leyland, coal, steel, etc.), performance was often poor:

- Many were loss-making and required heavy subsidies or bailouts.

- British Leyland (cars) was effectively nationalized in 1975 amid near-collapse, plagued by industrial disputes, poor productivity, falling market share, and low-quality output.

- British Rail faced chronic underinvestment, declining ridership on some lines, and inefficiencies (leading to later Beeching-style cuts in the 1960s, but problems persisted).

- Strikes and over-manning were common complaints, contributing to perceptions of inefficiency and unreliability compared to private-sector counterparts.

Not everything was disastrous — real wages rose for many in parts of the decade, consumer goods became more accessible, and some social progress occurred — but the decade is remembered for economic instability, industrial strife, and a sense of decline ("the sick man of Europe"). Nostalgia for aspects like stronger unions or public ownership often overlooks these failures, which many historians and economists view as key drivers behind the Thatcher-era reforms.

In short, no — "everything" did not work in the 1970s. The economy and many state institutions faced widespread, well-documented crises.