Identifying best practices in portfolio management using our proprietary quantitative strategies and technology. Check out our portfolio performances. DMs open!

We'll be launching our product suite soon but in the meantime head on to https://t.co/w9h8qMG2V1 and join to avail attractive discounts and get free priority access to our toolkit. Check out the website now!

#stockmarkets#stocks#StockMarket#Nifty#investing#Investment

About 1.25 years ago, I started learning about quantitative finance and building software to dabble with it, with a college senior. I started with quantitative factors and this is what they are : (🧵 Thread time!)

This optionality does not appear to generally be reflected in the prices of the past losers. Consequently, the expected returns of the past losers are very high, and the momentum effect is reversed during these times.

In bear markets, and when market volatility is high, the down-market betas of the past losers are low, but the up-market betas are very large. This makes such equities much like long options - limited downside risk and a much greater upside potential.

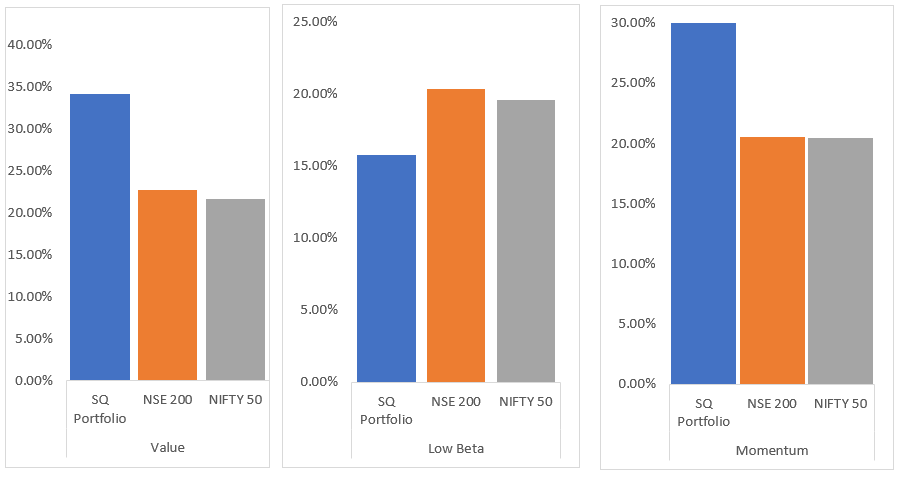

The chart below shows the performance of our 3 model portfolios since inception. While the momentum and value portfolios have generated outstanding alpha, the low beta portfolio somewhat lags the market.

#investing#StockMarketindia#stockmarkets#stockmarkets#investments

Everyone loves a gamble, especially a long shot!

Nick Barberis, in his paper "A Model of Casino Gambling," addresses why people go to casinos and how they behave once they get there.

The lottery characteristics associated with high beta stocks is a key driver of these stocks' poor performance. Investors are often willing to pay a higher than normal price for such high beta bets, which in turn leads to their underperformance on a risk adjusted basis.