Sharing the latest investment ideas sourced from the smartest analysts/investors (not traders) we know. Of course we are invested in most names covered here!

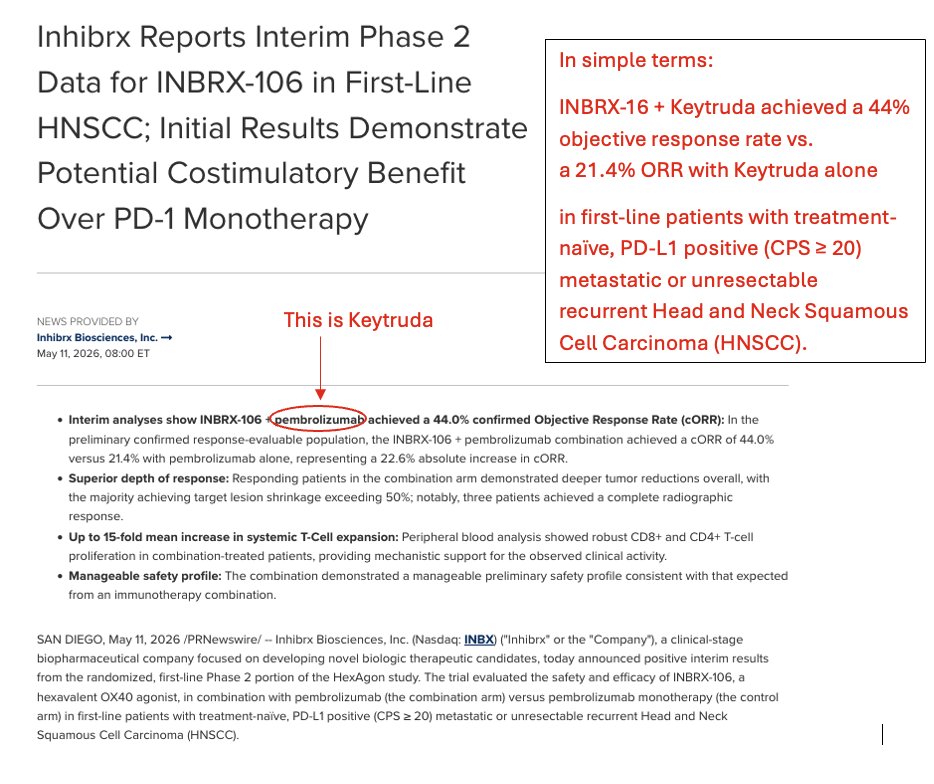

HUGE Phase 2 result for $INBX drug that turbocharges performance of Keytruda (pembrolizumab) - $MRK's biggest drug going off patent in 2028.

$2B market cap provides plenty of upside as $INBX advances development

https://t.co/jjQwpoochT

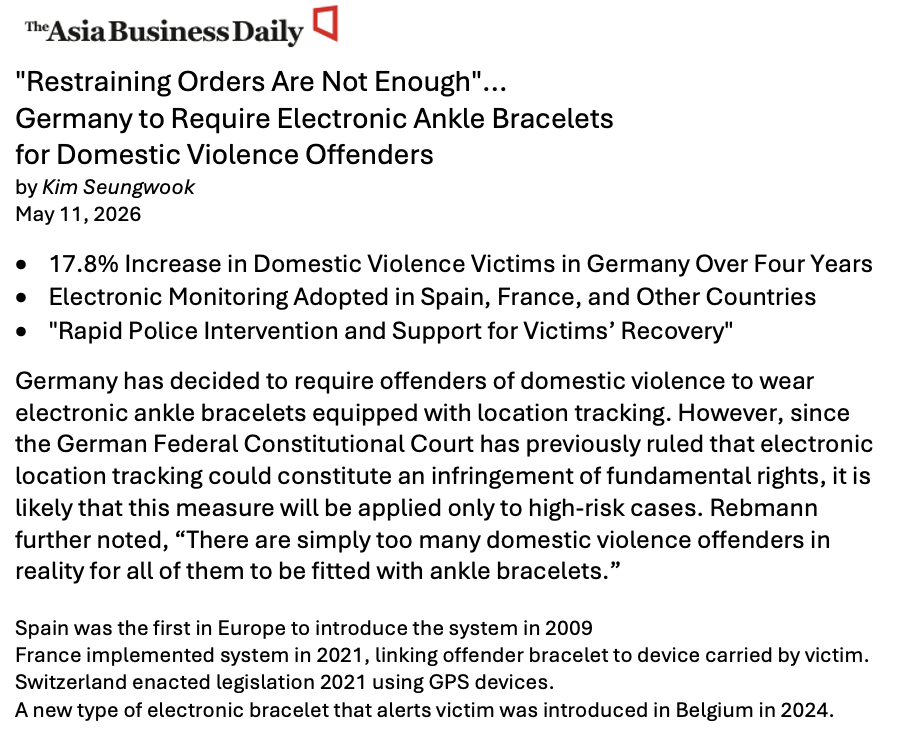

Kudos to @j16425646 for ferreting out this article on rising use of electronic monitoring for domestic violence applications in Europe. $SPCB https://t.co/TsFJVkfZ5H via @asiabus_daily

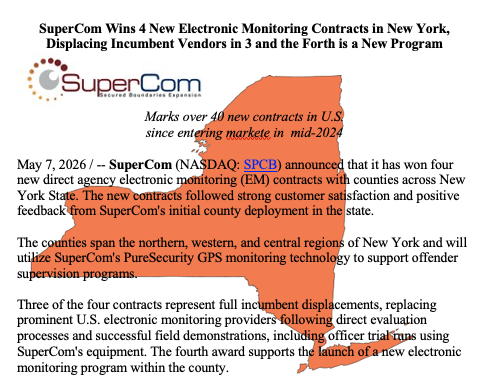

SuperCom $SPCB Wins 4 New Electronic Monitoring Contracts in New York, Displacing Incumbent Vendors in 3 and 1 new Program Launch

Brings SuperCom's US market wins to over 40 since entering market in mid-2024

https://t.co/FcOcoKuIoI

@j16425646 Love the story and your enthusiasm - but the Swedish contract that could be worth up to $76M is over a 9 year period - so I don't think $76M + $21M lets you add $50M to 2026!! $SPCB's credibility is already low - so lets stick to the facts - which are already very good!

Solid report by $SPCB despite the noise of some charges and a material financial gain that impacts reported EPS

Call today at 10:00 am

https://t.co/N1my974BtM

@InvestSpecial@HalvioCapital Wow - looks cheap and like it could say that way for years... looking at past few years posts on the name.

What's the catalyst to change the valuation?

$FTAI is a GREAT co that has been acting like💩recently

Smart investor got us in in the teens a few years ago & story keeps getting better as jet engines require maintenance. Guessing weakness relates to fuel price impacts on travel & possible near-term slowing of maintenance?

@test8612 $SPCB - seems it could easily sell for 20x trailing EPS of $0.80 (our guess) they have $0.70 of untaxed EPS (excluding financial gains) for the 9Months. Q4 report coming by April 30th.

So that's $16 - and if they can restore some credibility with investors - even higher!

$SPCB 2-year chart suggests there's more to go on the upside as we await year-end results due April 30th. A quick look at the 5-year chart helps explain why impressive electronic monitoring contract wins and rev ramp have been largely ignored ... so far.

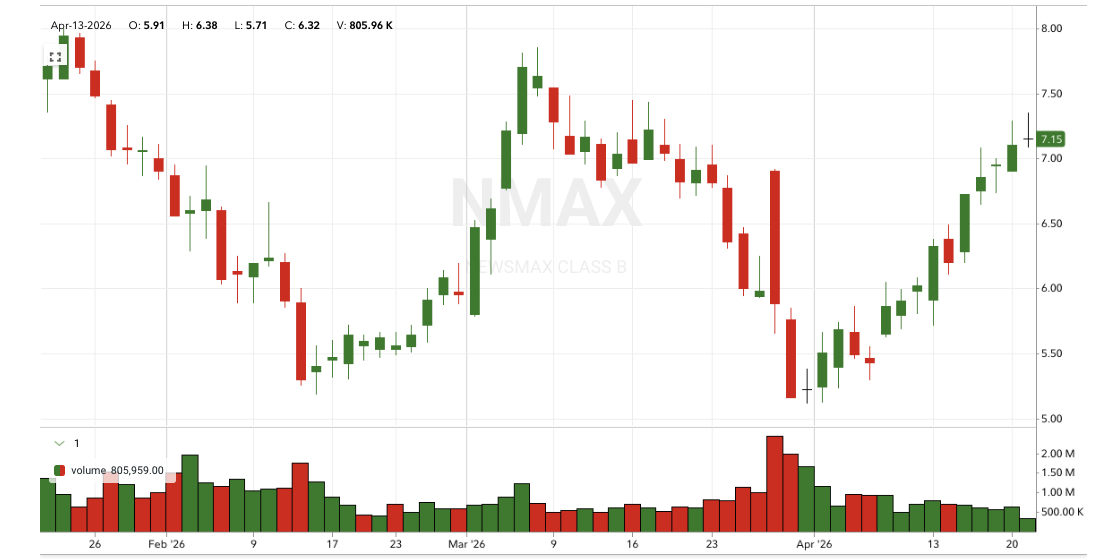

$NMAX has been rebounding nicely - making us feel better about violating the falling knives rule in averaging down. LT story seems very compelling as they work to raise their affiliate fees which are well below average

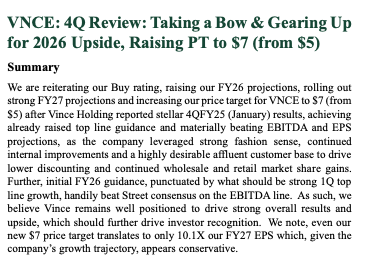

Nice Q4 & 2025 report from specialty retailer Vince Holdings $VNCE trading $3.12/share; 7x 2025 EPS of $0.44 for a $37.5M mkt cap

Veteran retail analyst Eric Beder @SCC_Research raised '26 estimate to $0.55 & PT to $7 or 10x his FY'27 EPS estimate of $0.66