Hello everyone, going ahead from March month I am going to track the below Mutual funds monthly portfolio.

We would discuss the changes each MF has made in the March month plus on which sectors the money is flowing.

If you have any other MFs which I should consider analysing, then please DM or put a comment so that I can give a look and post here in X.

Please consider all the tweet as educational purposes and not a Buy/sell recommendation.

Cheers. Let's go and Happy investing.👍

The company faces zero domestic competition in India. Management notes that no other company in India possesses the capability to perform this complex EB welding for these sub-assemblies. Unless a foreign competitor manufactures the entire complicated assembly abroad and ships it to India, it holds a monopoly in the domestic market for this specific niche. In the broader shunt segment, the company does compete globally, notably against a major competitor with a production unit in China. However, recent US-China trade volatility has prompted customers to diversify, bringing new business inquiries and RFQs to Shivalik.

@vishan_29@Anvith_@GingerInvest44@InvestmentVeda@suryachaudhary1@Saurabh_TyagiX

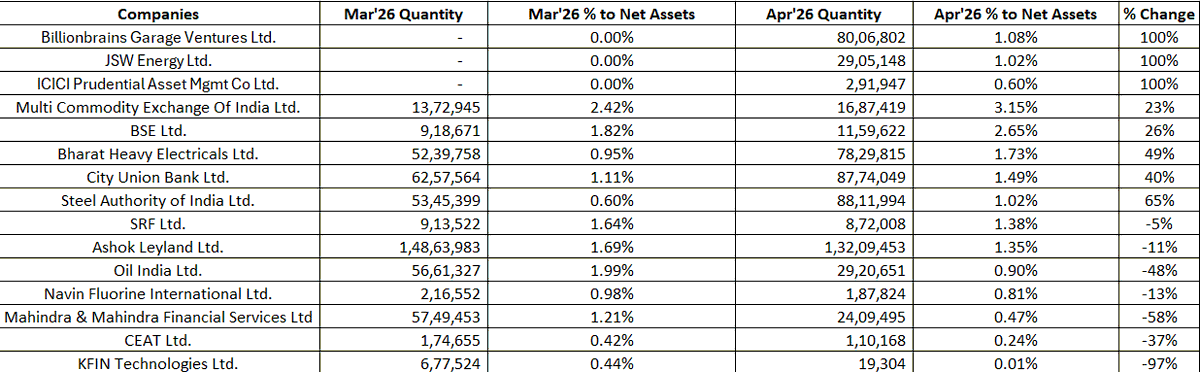

Edelweiss Midcap Fund Apr'26 Portfolio Updates -

Let's see where the Edelweiss Midcap Fund @iRadhikaGupta has increased allocation in April.

▶️3 New Additions

🔹Billionbrains Garage Ventures - 1.08%

🔹JSW Energy - 1.02%

🔹ICICI Prudential AMC - 0.60%

▶️Increased Allocation -

🔹Steel Authority of India: ↑65%

🔹Bharat Heavy Electricals: ↑49%

🔹City Union Bank: ↑40%

🔹BSE Ltd: ↑26%

🔹MCX India: ↑23%

▶️Decreased Allocation -

🔹KFIN Technologies: -97%

🔹M&M Financial Services: -58%

🔹Oil India: -48%

🔹CEAT Ltd: -37%

🔹Navin Fluorine International: -13%

���Ashok Leyland: -11%

🔹SRF Ltd: -5%

=> Added 3 new companies indicating clear exposure towards capital market participation, India financialization and power demand & energy transition

=> Edelweiss Midcap Fund has increased allocation in companies with a focus on key themes like infra & steel demand, power capex & demand growth, banking & financialization, and defence + mining

=> Reduced allocation companies where fund has either done profit booking or there are concerns related to crude volatility, chemical slowdown and CV cycle moderation.

Investor Takeaway -

=> Aggressive play on power & infra capex

=> Financialization theme gaining importance

=> Diversified industrial exposure

=> Focus on scalable midcap compounders

=> Reduced exposure to weak export-oriented sectors

Edelweiss Midcap Fund is aggressively positioning for India’s next domestic capex and financialization cycle through power, industrials, exchanges, and mid-sized financials, while reducing exposure to chemicals, commodity cyclicals, and select auto names.

@vishan_29 @Anvith_ @BaluGorade @InvestNifty_ETF @AnkitFinAlpha @TrendSpark420 @Dynamicinvstr @viralbshah @InvestmentVeda @ThetaVegaCap @AshishMeher7

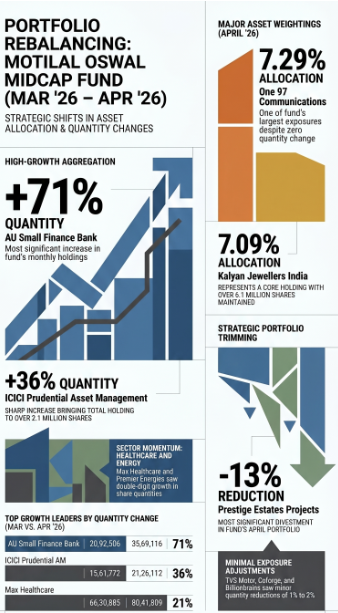

Motilal Oswal Mid Cap — Mar'26 → Apr'26 Portfolio Update 🧵

🟢New Addition✖️

🔴Zero Exits✖️

🟡Increased Allocation -

Motilal Oswal Midcap Fund has increased allocation in 8 companies - AU Small Finance Bank - 71%, ICICI Prudential AMC - 36%, Max healthcare - 21%, Premier Energies - 18%, PB Fintech - 13%, Waaree Energies - 10%, IDFC First Bank - 7% and Tube investments - 3%

🔴Decreased Holdings -

The fund has decreased allocation Prestige Estates, Groww, Coforge Limited, MCX India, TVS Motor Company.

Investor Takeaways

✔ Strong exposure to long-duration India growth themes

✔ Conviction-led concentrated strategy

✔ Renewable + financialization themes can compound for years

✔ Healthcare addition improves quality mix

Motilal Oswal Midcap Fund continues to aggressively position for India’s domestic growth cycle through financials, renewable energy, healthcare, and manufacturing, while trimming exposure to IT and selective cyclicals.

If this was useful, RT the thread🔁

⚠️For educational purposes only. Not investment advice. Consult your financial advisor.

@Dynamicinvstr@vini546@Anvith_@AshishMeher7

Websol Energy System - (W) Chart - CMP - Rs. 122

During correction period, stock made a low of Rs. 50 levels and took support.

After correction, stock has already given a move of more than 2x.

Yesterday, company posted solid results and today stock is up by 5%.

Next Resistance: 138 - 159 - 186 levels to watch out for in coming days.

Disclaimer: This is not a Buy/Sell recommendation.

Quant Flexi Cap Fund Breakdown of holdings from Feb’26 → Mar’26

🔸New Entries

The fund has added ICICI Prudential AMC with 4.38% allocation and LG Electronics India with 0.27% which clearly signals strong capital market play added aggressively and selective consumer durable exposure

🔸Complete Exits

Quant has completely exited from Wipro as IT is currently out of favour in the market currently.

🔸Increased allocation

They have increased allocation in Adani Green Energy and Adani Enterprises. Clear focus on Adani companies with the likes of Adani power, Adani energy solutions as well.

✅Investor Takeaways

✔ Strong conviction → potential alpha generation

✔ Positioned for power + infra multi-year cycle

✔ Early bet on AMC / capital market's theme

⚠ High dependence on Adani group

⚠ Momentum strategy → volatile drawdowns

If this was useful, RT the thread🔁

⚠️For educational purposes only. Not investment advice. Consult your financial advisor.

@Dynamicinvstr

HDFC Small Cap Fund - Feb → Mar 2026 Portfolio Dissected

🔹Complete Exit

HDFC Small Cap exited TCPL Packaging Ltd in March'26 as the company's export segment has been a persistent dry. Revenue dipped YoY in Q3FY26, stocks fell ~41% over the past year. Fund likely rotated out of a weak story in a mature, low-growth packaging sub-segment.

🔹Trimmed Allocation

KEI Industries - Cables & electricals sector. Stock has stretched to 50-55x PE — significantly above industry average of ~18x. Multiple analysts downgraded from Strong Buy → Hold between Feb & Mar. Fund trimmed aggressively into the valuation stretch.

Greenlam Industries - Decorative laminates player. Net profit declined due to forex headwinds, higher depreciation & rising interest costs from new capacity. A cautious partial trim.

🔹Increase in Allocation

▲ Wakefit Innovations - Largest D2C home & sleep solutions brand, aggressively high conviction bet

▲ Vishal Mega Mart - Value retail play. Budget consumer spending theme gaining traction

▲ Indigo Paints +9.81%

▲ JK Tyre & Industries +9.11%

▲ Mastek Ltd +8.65%

▲ PVR Ltd +6.16%

📊The Macro Read

This portfolio reshuffle sends 3 clear signals:

🔹Domestic consumption is the core thesis

Wakefit, Vishal Mega Mart, Dodla, PVR — all bet on India's middle class spending up.

🔹IT/BPO love hasn't faded

eClerx (post-bonus), Mastek, Zensar maintained/added. Small cap IT remains a conviction sector.

🔹Valuation discipline is real

KEI at 50x+ PE? Trim. TCPL with falling exports? Exit. No sentiment, just math.

If this was useful, RT the thread🔁

⚠️For educational purposes only. Not investment advice. Consult your financial advisor.

@Dynamicinvstr@vini546

India’s Power Grid Is Entering a High-Voltage Capex Supercycle—Where HVDC and 765 kV Will Drive the Next Decade of Value Creation

HVDC = The Real Structural Theme

=> Bi-pole capacity doubles (~102%)

=> Back-to-back remains flat → focus is inter-regional transmission, not grid synchronization

👉 Implication:

- Large ticket projects

- Higher complexity → limited competition

- Better margins vs conventional EPC

✔ This is similar to what roads saw with expressways vs rural roads

765 kV substations → Hidden compounding engine

=> +53% growth in substation capacity

=> Substations scale alongside transmission lines

👉 Why this matters:

- Substations = high-margin + repeat orders + less commoditized

- Requires transformers, GIS, switchgear, reactors

✔ This is where ancillary players make serious money

Capex intensity will stay elevated till FY32

Transmission lines + substations + HVDC = multi-layer capex cycle

Driven by:

=> 500+ GW RE target by 2030

=> Green Hydrogen + storage

=> Industrial electrification

✅Sectoral Winners

1⃣Transmission EPC / Infra Developers

🔹Power Grid Corporation of India

→ Core beneficiary; owns majority HVDC & 765 kV network expansion

🔹Adani Energy Solutions

→ Aggressively bidding for TBCB projects; key private HVDC/765 kV play

2⃣ EPC (Transmission + Substation Builders)

🔹Larsen & Toubro

→ End-to-end EPC giant; key player in complex HVDC & GIS substations

🔹Kalpataru Projects International

→ Global T&D EPC leader; strong order inflow visibility

🔹KEC International

→ Core transmission EPC play; levered to domestic + exports

🔹Techno Electric & Engineering

→ High-margin substation EPC specialist; operating leverage story

🔹Transrail Lighting

→ Emerging EPC player in transmission with improving order book

🔹Skipper Limited

→ Towers + EPC; backward integrated transmission play

3⃣ Transformers, Reactors & Heavy Electricals

🔹CG Power and Industrial Solutions

→ Direct play on transformers + reactors for 765 kV/HVDC

🔹Hitachi Energy India

→ Pure-play HVDC tech leader; high-margin opportunity

🔹Siemens India

→ GIS, automation, grid tech; benefits from high-voltage shift

🔹Bharat Heavy Electricals Limited

→ Revival via transformers + HVDC participation

🔹Transformers and Rectifiers India

→ Direct beneficiary of substation capacity expansion

🔹Voltamp Transformers

→ Niche high-quality transformer player with strong margins

🔹Star Delta Transformers

→ Smaller player; levered to distribution + substation demand

4⃣Cables & Conductors

🔹Polycab India

→ Strong in power cables; benefits from transmission + distribution

🔹KEI Industries

→ High-voltage cable opportunity + exports

🔹Finolex Cables

→ Retail-heavy but indirect beneficiary of power capex

🔹Sterlite Technologies

→ Conductors + grid solutions via Sterlite Power ecosystem

🔹Diamond Power Infrastructure

→ Turnaround play; direct T&D exposure

5⃣Towers, Structures & EPC Backward Integration

🔹Skipper Limited

→ Leading tower manufacturer; benefits from transmission line expansion

🔹Salasar Techno Engineering

→ Towers + structures; operating leverage with order inflow

6⃣Switchgear, GIS & Grid Automation

🔹ABB India

→ Switchgear + automation; key to smart grids & substations

🔹Schneider Electric Infrastructure

→ Substation equipment + automation; steady growth play

🔹GE Vernova T&D India

→ HVDC + grid tech; global tech spillover into India

Ancillary / Component Suppliers

🔹Apar Industries

→ Global leader in conductors + transformer oils; direct HVDC play

🔹Kritika Wires

→ Niche conductor supplier; volume-led growth

🔹Ram Ratna Wires

→ Copper winding wires; indirect transformer demand play

✅Investor Takeaway

👉 This is a “High Voltage Capex Supercycle”, not generic power growth

✔ HVDC + 765 kV = premium segment → higher margins, lower competition

✔ Substations = silent compounders (repeat + sticky business)

✔ EPC + Equipment combo players win disproportionately

India’s power grid is upgrading from “wires” to “power highways”—and HVDC + 765 kV players will capture the maximum economic value.

To know more about India's Power T&D outlook, please check the below post by @vishan_29 🔽

Disclaimer: This is not a Buy/Sell recommendation.

@Anvith_@Dynamicinvstr@TrendSpark420@ABCI_Invest@investor_sr33@vini546@InvestmentVeda

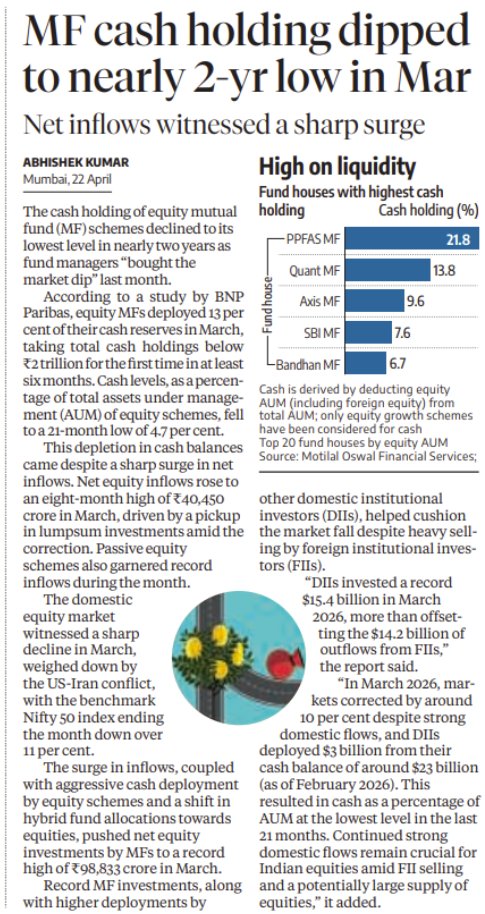

Mutual Funds Burn Cash Reserves, Betting Big on Market Dips

Equity MF cash holdings fell to ~4.7% of AUM, the lowest in ~21–24 months.

In absolute terms, equity MF cash fell below ₹2 trillion for the first time in about six months. This signals that fund managers actively deployed cash instead of staying defensive.

Net equity inflows jumped to ₹40,450 crore in March (8‑month high). Lump‑sum investing increased sharply during the market dip.

Passive equity schemes (index funds & ETFs) saw record inflows, which must be invested, reducing cash further.

March saw heavy FII selling, triggered by:

- US‑Iran geopolitical tensions

- Global risk‑off sentiment

Domestic institutional investors (DIIs) invested a record ~$15.4 bn, more than offsetting $14.2 bn FII outflows.

Cash holdings by fund house:

- PPFAS MF – 21.8% (highly conservative and known for higher cash in hand)

- Quant MF – 13.8%

- Axis MF – 9.6%

- SBI MF – 7.6%

- Bandhan MF – 6.7%

Hybrid funds reduced cash and shifted allocations toward equities. SIP + lump‑sum behavior shows dip‑buying mentality is becoming entrenched.

��Strategy takeaway

🔹SIP investors: Stay the course; volatility works in your favor.

🔹Lump‑sum investors: Prefer staggered deployment rather than all‑at‑once.

🔹Active fund selection: Check cash stance + valuation discipline of the fund house.

@Dynamicinvstr @vini546 @Anvith_ @TrendSpark420 @viralbshah @InvestRepeat

HDFC Flexi Cap Fund - March '26 Portfolio Decoded

2 new entries. 1 full exit. Cash slashed from 15.56% → 4.52%.

The fund is turning aggressive. Here's everything that moved 👇

🔹New Additions (Feb → Mar)

Reliance Industries - Added 1.27 CR shares (1.88% of net assets). Zero holding in Feb. Full new bet on India's largest conglomerate across energy, retail & telecom.

Anthem Biosciences - Added 75.75L shares (0.54%). Fresh pharma CDMO play post-IPO. Fund sees CDMO opportunity in India's biopharma export story.

🔹Complete Exits

Sundram Fasteners - Fully sold. Held 34L shares (0.3%) in Feb '26.

Why? Export revenue fell 12% YoY. Profit dipped 7.4% despite revenue growth — margin erosion is real. Weak truck demand + geopolitical headwinds + GST penalty added pressure.

Rs. 358CR offloaded via bulk deals on Mar 3. Stock hit 52-week lows after.

🔹Top Movers - Increased Allocation

Metropolis Healthcare: +300% qty ↑

Aster DM Healthcare: +203.8% qty ↑

Max Healthcare: +149.9% qty ↑

Dixon Technologies: +87.9% qty ↑

Eternal (Zomato): +37.4% qty ↑

Divis Laboratories: +32.2% qty ↑

InterGlobe Aviation: +28.7% qty ↑

🔹Reduced Positions

ONGC: -20.7% qty ↓ (5.5Cr → 4.36Cr shares)

Tata Steel: -4.46% qty ↓ (7.9Cr → 7.54Cr shares)

ONGC trimmed on weak crude realizations + PSU capex uncertainty.

Tata Steel cut on China oversupply pressures dragging steel margins.

🔹Sector Watch - Where the fund is loading up

Healthcare (massive conviction): Metropolis (+300%), Aster DM (+204%), Max Healthcare (+150%), Divis Labs (+32%)

Fund is building a broad healthcare bet - diagnostics, hospitals, pharma CDMO all accumulated together.

Consumer Tech: Eternal/Zomato (+37%) - quick commerce thesis intact.

🔹Sector Watch - Where the Fund is Pulling Back

Auto Components (EXIT): Sundram Fasteners fully out. Export weakness + margin compression. No near-term reversal expected.

Metals (TRIM): Tata Steel cut - global steel pricing under pressure.

PSU Energy (TRIM): ONGC reduced - low crude upside + policy overhang.

🎯The Big Picture

HDFC Flexi Cap's March '26 move is clear:

→ Rotating INTO healthcare, CDMO, consumer tech, aviation

→ Rotating OUT OF auto components, PSU energy, metals

→ Cash deployed aggressively (15.56% → 4.52%)

This is a fund betting on domestic consumption + India's pharma export story

If this was useful, RT the thread🔁

@Dynamicinvstr@vini546

Bank of Maharashtra - Chart

Bank has given solid Q4 results recently and stock has rewarded its investors as well.

Taking Trendline support and making higher highs.

Currently trading around 81 levels; need to break 84 levels and sustain.

Then move ahead for bigger multi-year breakout of 96 levels which was reached in 2007.

Two Multi-year breakouts -

1st - Rs. 84

2nd - Rs. 96

Keep in watchlist 👀

Disclaimer: Invested around 42 levels. No Buy/Sell recommendation.

@Anvith_

🧵Edelweiss Mid Cap Fund - March '26 Portfolio Dissection

New entry. Partial exits. Sector rotation signals.

Here's everything the fund did between Feb & Mar 2026 — decoded.

🆕Fresh position added: Bharat Heavy Electricals (BHEL)

BHEL (Capital Goods / Power Equipment) — +100% new

52.39L shares acquired. Weight: 0.95% of portfolio.

Why now?

BHEL's FY26 order inflows crossed ₹75,000 Cr, PAT up ~190% YoY in Q3FY26. India's power capex super-cycle is just beginning - the fund is getting in early.

📈Significant stake increases this month:

Ashok Leyland (Auto / Commercial Vehicles) - +28%

Supreme Industries (Plastics / Pipes) - +66%

Astral Ltd (Pipes / Adhesives) - +47%

Federal Bank (Private Sector Bank) - +38%

Bharat Forge (Forging / Auto Ancillary) - +24%

Cyclical conviction building. Auto, infra-materials, and private banking getting renewed attention.

📈More positions beefed up:

AU Small Finance Bank (NBFC-Bank) - +18%

Karur Vysya Bank (Mid-size Private Bank) - +20%

City Union Bank (South India Banking) - +15%

Polycab India (Cables & Wires) - +15%

Blue Star (Cooling / HVAC) - +17%

Financial sector & infra-linked plays dominate the buying list. Clear vote of confidence in India's domestic capex + credit cycle.

✂️Stakes trimmed (partial profit-booking or rebalancing):

APL Apollo Tubes (Steel Tubes): -1%

CEAT Ltd (Tyres): -2%

Bharti Hexacom (Telecom): -22%

Bharat Dynamics (Defence / Missiles): -43%

Telecom & defence names being quietly de-risked. Hexacom's share has underperformed its parent Airtel, and BDL faces near-term order execution delays. Smart rotation signal?

🚪Complete exits — fund walked away entirely:

HDB Financial Services (NBFC (HDFC Group)): -100%

Escorts Kubota (Tractors / Agri): -100%

HDB Financial: Post-IPO valuation rich. Fund likely locked in listing gains and moved on. No margin of safety at current prices.

Escorts Kubota: Tractor volumes remain sluggish. Agri sector uncertainty + rural income pressures making a weak near-term case.

🏭Where did Edelweiss MF add conviction?

⚡Capital Goods & Power Equipment

BHEL entry. India's power infra capex cycle heating up. BHEL's order book at multi-year high. Long-duration tailwind play.

🏦Mid-size Private Banks & SFBs

Federal Bank, AU SFB, Karur Vysya, City Union - all increased. Valuations still reasonable vs. large private banks. Credit growth re-accelerating.

🔧Industrials & Auto

Ashok Leyland (+28%), Bharat Forge (+24%). CV upcycle + defence exports from Bharat Forge making it a dual beneficiary.

🏗️Building Materials & Pipes

Astral (+47%), Supreme (+66%), Polycab (+15%). Housing + infra demand driving multi-year growth for pipe & cable makers.

🔻Where did Edelweiss MF reduce or exit?

📡Telecom (Bharti Hexacom -22%)

Tariff hike cycle priced in. Hexacom's coverage circles (Rajasthan, NE) have limited ARPU expansion potential vs. pan-India operators. Regulatory penalty overhangs added risk.

🚀Defence PSU (Bharat Dynamics -43%)

BDL order execution delays and stretched valuations post-2024 rally. The fund seems to prefer booking gains at peak defence euphoria.

🚜Agri / Tractors (Escorts Kubota -100%)

Sluggish tractor volumes, rural distress, and elevated inventory across dealerships made the risk-reward unattractive.

💳NBFC (HDB Financial -100%)

Post-IPO valuation re-rating complete. Microfinance stress across the NBFC space makes further holding unappealing at premium multiples.

📌The big picture from this month's moves:

✅Rotating INTO: Power infra, mid-tier private banks, building materials, auto cyclicals

🔴Rotating OUT OF: Telecom, defence PSUs, agri, post-IPO NBFCs

Edelweiss is making a clear bet on domestic capex + credit recovery while trimming sectors where valuations ran ahead of fundamentals.

If this was useful, RT the thread🔁

@Anvith_@TrendSpark420@Dynamicinvstr