I’ve held off on posting my $DTIL thoughts pending the release of additional competitor data at EASL 2026 (more on that below). This has given me time to digest the data, evaluate the field, and form what I express below.

$DTIL EASL update:

Earlier this week, Precision BioSciences stood before the Hepatitis B community and stated that the field is at a turning point. Moving from lifelong suppression toward finite, biomarker-guided viral cure.

The tool that has been developed by $DTIL was designed to target the direct viral source of Hepatitis B, cccDNA — the factory that produces infectious virus, HBV DNA. All drug development to date has targeted things that are downstream from the viral source. This is largely due to there not being a tool (like gene editing with ARCUS in this case) that could get to cccDNA.

As such, the FDA has previously stated in 2022 that sustained suppression (6 months or longer) of HBV DNA (less than LLOQ, TD or TND) off-treatment after a finite duration of therapy is an approval endpoint.

$DTIL declared to the world this week that pgRNA is the appropriate blood biomarker to watch because it comes directly from cccDNA and is the necessary precursor of HBV DNA replication. Note: HBV DNA is undetectable for patients on NAs — all patients in this trial are also on NAs currently.

100% (6/6) patients enrolled in the ELIMINATE-B trial to date who had detectable pgRNA in the blood had pgRNA fully undetectable (eliminated) following the administration of PBGENE-HBV. The fascinating part to me is that it took a varying number of doses of PBGENE-HBV to achieve pgRNA undetectability. In two patients — it took one dose, in three patients — it took two doses, and in one patient it took three doses. Obviously across varying dose levels.

The challenge: if $DTIL is eliminating cccDNA, that will lead to loss of pgRNA in the blood. However, pgRNA is not always detected in the blood. HBV DNA undetectable is an FDA approvable endpoint and so is HBV DNA + HBsAg undetectable. So, what if a patient demonstrates complete pgRNA loss that translates to stopping NUCs with HBV DNA remaining undetectable but HbsAg is still present from iDNA? Does the HBsAg (that has been drastically reduced) still being expressed from iDNA hurt the patient? Billion dollar question right there.

Who better to answer that question than Dr. MF Yuen?

I reached out to Dr. Yuen via email and asked “In your professional opinion, can HBsAg produced from iDNA in a Hepatitis B patient harm them if their cccDNA is eliminated?”

Dr. Yuen responded: “Theoretically, HBsAg produced from iDNA should exert no harm to the liver.”

First & foremost, big thank you to Dr. Yuen for being willing to respond to an email inquiry. The answer received from Dr. Yuen is obviously hedged by “theoretically” because no previously studied tool has been able to eliminate cccDNA like this, therefore this question has not been answered in humans. It seems that Precision will be able to paint that picture at their AASLD update later this year. If indeed this theory translates to practice, this could be groundbreaking.

What about the other patients who did not have pgRNA detectable in the blood at baseline? Another question that must be answered with more research. Dr. Yuen noted during the Q&A session that he “guaranteed” that these patients had pgRNA detectable in the liver at baseline, meaning a biopsy would have had to be the method of detection and measurement here. Is that clinically feasible long-term? No. However, $DTIL will need to get biopsies on patients who are pgRNA- in the blood at baseline and also prove that they are eliminating the pgRNA via cccDNA elimination and correlate that to HBV DNA loss after NA stoppage — exactly what they’ll have to do in the patients with the blood biomarker just with a biopsy.

pgRNA outperforms other biomarkers (e.g., HBsAg) in predicting the effective and safe withdraw of NAs (Terrault NA, et al. J Infect Dis. 2025;231(5):1290-1298.).

The biopsy data:

Two patients (both in cohort 2) have consented to a liver biopsy thus far. Patient 5 (previously disclosed at a high-level) had a pre and post treatment biopsy and patient 6 had a post treatment only biopsy.

The effect of cumulative, repeat administrations were clear. PBGENE-HBV potently eliminates cccDNA which results in loss of viral transcripts. Furthermore, as a secondary mechanism — PBGENE-HBV turns off the polymerase function which results in complete viral inactivation. In plain language, it stops the packaging of pgRNA and shuts down the ability for pgRNA to create new HBV DNA.

Patient 6 (blood detectable pgRNA at baseline) showed full pgRNA elimination in both the blood and the liver which further supports using blood pgRNA as an indication of pgRNA levels and cccDNA in the liver.

Safety:

In vivo gene editing is inherently subject to higher scrutiny because it is designed to alter a human’s DNA. It’s very good to see the LNP related ALT / AST spikes not also increase bilirubin. We certainly do not want a Hy’s Law situation with this program. It was also encouraging to hear Dr. Yuen verbally express that there weren’t any abnormal effects that were out-of-line with LNP delivery noting that the safety profile was “quite OK”.

Despite Cohort 3 having idiosyncratic grade 3/4 AEs, the new simple and mechanism related safety measures have mitigated hypotension and liver lab abnormalities moving forward — this seems that it should continue. Not having to make a “chemistry change” is key here. Some may recall Verve needing to shelve VERVE-101 and move to VERVE-102 to use a different ionizable lipid in their LNP — not the case here.

Next steps:

In summary, liver biopsies in combination with key blood biomarkers reflect cccDNA elimination

and support increased probability of cure after treatment with PBGENE-HBV. I look forward to $DTIL stopping NAs and testing for a cure in the patients with blood pgRNA eliminated first. Although these patients will have to prove 6 months of sustained HBV DNA elimination after stopping the background therapy (NAs), imo, if a patient sustains HBV DNA suppression 1-2 months after NA discontinuation — that is a very good sign because the NA washout period is fairly quick and NAs would be the only other possible suppressor of HBV DNA.

Concurrently, $DTIL will expand the number of participants in cohorts 4 & 5 to try to nail down the best dose combination to take this forward (seemingly as a monotherapy).

The Q&A section, in combination with what a competitor is doing also makes me wonder if $DTIL will explore adding HBeAg+ patients. As a reminder, they are only enrolling HBeAg- patients today. On slide 19 of their presentation, $DTIL also mentions that HBeAg+ patients have higher cccDNA, pgRNA, % of sAg from iDNA, and they verbally mention that it’s an earlier line population that their treatment could potentially benefit earlier and further reduce the change of long-term negative impacts from Hepatitis B. I am fully supportive of starting to enroll people from the HBeAg+ population to continue to PROVE the emerging trend that pgRNA loss in the blood = cccDNA elimination which means that you’ve suppressed HBV DNA.

The partnership piece. $DTIL has stated that they can take this clinical study through phase 2 without a partner. However, I would imagine that there are ongoing partnership discussions in this space. $GSK, $GILD, $RHHBY all natural domestic fits. I am admittedly less familiar with the Asian landscape but would also imagine there are partners based in China that could have interest given the heavy population of Hepatitis B patients in China. $DTIL also including the $GILD logo is no accident.

The readout from $GSK this week vastly beat other currently approved HBV therapies with a functional cure rate of ~19% (still short of the global goal of 30% by 2030). GSK has already submitted Bepirovirsen for approval in the U.S., Japan, Europe and China, with the FDA set to make a decision by October.

Could a Bepirovirsen + PBGENE-HBV be studied as a combination therapy? Bepirovirsen stops DNA replication because it breaks down (doesn’t eliminate) pgRNA, then stops the production of HBsAg, and acts as an innate immune stimulation mechanism. PBGENE-HBV could eliminate the cccDNA while Bepirovirsen takes down the HBsAG — especially if PBGENE-HBV ultimately needs to drive further HBsAg levels. IMO, the reality is multiple treatments working in tandem to cure the disease.

Finally, I have my eye on AASLD TLM in November for a significant update from $DTIL regarding the ELIMINATE-B trial.

Asymmetric competition:

The epigenetic silencing group. Tune Therapeutics had a late breaking oral presentation today at #EASL26. For those who don’t know, Derek Jantz (former $DTIL co-founder & CSO) is now the CSO at Tune after exiting Precision shortly after the Amoroso administration began. Topic for another day but imo he wanted to boil the ocean (they were in food, ex-vivo, many in-vivo research programs, etc.). Say what you want about Amoroso but he has focused the company. I haven’t always agreed with his means of raising capital but the company is now singularly focused on in-vivo gene editing (what they feel they do best) and I respect that. I also digressed a bit.

I’m not going to deep-dive Tune’s data as much as I did for $DTIL.

The approach that Tune is taking to Hepatitis B is a targeted epigenetic silencer that is delivered via LNP (using a guideRNA versus protein recognition like ARCUS). In essence, it is designed to silence cccDNA without cutting the underlying DNA. $DTIL cuts and completely eliminates, Tune silences. When I say that Tune silences it doesn’t remove the cccDNA, it just dresses it in repressive marks (methylation + compaction) The template is still physically sitting in the hepatocyte nucleus, intact, transcriptionally silent but reactivatable in principle. Whereas, gene editing (the $DTIL approach), destroys the template — nothing left to reactivate in the future.

TL;DR on the Tune data: fairly in-line with Precision’s IMO. Though they didn’t achieve the 100% threshold on patients achieving pgRNA undetectability. On the other hand, some of their cohorts only had one dose. Their safety profile is relatively in-line with Precision’s. Durability is a long-term question given the silencing approach versus fully cutting cccDNA. Time will tell. I could see a path where patients select the non-DNA-editing approach if these patients are able to take the next step and discontinue NAs and successfully achieve sustained HBV DNA undetectability. That said, I don’t see Tune talking enough about how this program aligns with FDA guidelines for an approvable endpoint. Time will tell. It’s still early — something to watch.

Before wrapping up the epigenetic silencing topic — Tune has a direct competitor in that space, nChroma, who dosed first patient in January using a similar, if not the exact same, approach as Tune. I believe this company also has ties to the famed David Liu.

I already talked about Bepirovirsen from $GSK. Again something that patients could choose over a gene editing approach. That said, I don’t necessarily view this as competition — rather something that could be used in tandem to achieve a viral cure if $DTIL is unable to get across the finish line as a monotherapy.

Aligos Therapeutics just sold its China rights to their phase 2 HBV treatment. It’s supposed to prevent HBV DNA integration and reduce cccDNA. I just don’t see this as a threat at this time. Good for them getting $25MM from Amoytop in exchange for China rights.

Cash position:

$DTIL had ~$125MM in cash & cash equivalents as of the end of 1Q26. The first quarter of 2026 also saw an earned $7.5MM milestone payment from $TGTX resulting from an azer-cel partnership that $TGTX is using to treat MS and now more.

In speaking to $DTIL leadership late last year, their cash burn is going to be ~$15MM/quarter at the moment.

As we all know, biotechs can be penalized by the market when cash position is too low. I hope this is not the case but I could see a path where $DTIL raises on the back of AASLD data later this year. Let me be clear, I can swallow a raise of $75-100MM @ a $1B valuation, versus a $75MM raise at a ~$75MM valuation (almost precisely what took place last November).

I would hope that $DTIL is actively pursuing mid to late-stage business development discussions to help with the cash position.

DMD program:

Unlike many other DMD gene editing / therapy approaches, $DTIL targets exons 45-55, which account for ~60% of DMD patients. It is one and done and is in-vivo. The best part is that they use a small amount of AAV to deliver relative to competitors and their full capsid ratio is largely higher, they’ve also shown evidence of satellite cell editing in pre-clinical models — driving permanence.

Micro-dystrophin programs have been mediocre to disappointing at best. $DTIL is aiming to create a Becker like phenotype which is ~85%+ of a full length dystrophin. There is an abundance of data to show this type of dystrophin offers functional benefit for humans.

$DTIL has an approved IND and is actively recruiting at Arkansas children’s with a world class expert leading the study from a clinic standpoint.

Where $DTIL goes from here:

The back half of this year remains catalyst rich for $DTIL. They continue to commit to a year end DMD update and we can all pencil in a AASLD TLM update in November for the HBV program imo.

I’ll be honest, I struggle to see the long-term path to independence for $DTIL without going through a series of additional dilutive events. I believe there is a path there for a big HBV partnership that provides sustainable cash to fund DMD to completion. However, I see a path to an exit via M&A starting to form potentially as early as 2027. Build the data story for HBV and DMD, exit to big pharma and use their balance sheet to expand the ARCUS platform to indications that aren’t currently accessible due to capital constraints. Clear path to $GSK, $GILD. $RHHBY would be one of the cleanest fits, imo — they’ve been active in DMD and HBV over the years. $NVS dark horse with past partnerships and a current undisclosed research program.

I’d like to hear thoughts from others as well, don’t hesitate to comment or reach out directly. This is going to be interesting at a minimum.

These thoughts are my own and I state my opinion. I own $DTIL stock. There is a lot of AI slop out there these days — I used AI in research but wrote this myself. I used em-dashes before they were cool.

I’ve held off on posting my $DTIL thoughts pending the release of additional competitor data at EASL 2026 (more on that below). This has given me time to digest the data, evaluate the field, and form what I express below.

$DTIL EASL update:

Earlier this week, Precision BioSciences stood before the Hepatitis B community and stated that the field is at a turning point. Moving from lifelong suppression toward finite, biomarker-guided viral cure.

The tool that has been developed by $DTIL was designed to target the direct viral source of Hepatitis B, cccDNA — the factory that produces infectious virus, HBV DNA. All drug development to date has targeted things that are downstream from the viral source. This is largely due to there not being a tool (like gene editing with ARCUS in this case) that could get to cccDNA.

As such, the FDA has previously stated in 2022 that sustained suppression (6 months or longer) of HBV DNA (less than LLOQ, TD or TND) off-treatment after a finite duration of therapy is an approval endpoint.

$DTIL declared to the world this week that pgRNA is the appropriate blood biomarker to watch because it comes directly from cccDNA and is the necessary precursor of HBV DNA replication. Note: HBV DNA is undetectable for patients on NAs — all patients in this trial are also on NAs currently.

100% (6/6) patients enrolled in the ELIMINATE-B trial to date who had detectable pgRNA in the blood had pgRNA fully undetectable (eliminated) following the administration of PBGENE-HBV. The fascinating part to me is that it took a varying number of doses of PBGENE-HBV to achieve pgRNA undetectability. In two patients — it took one dose, in three patients — it took two doses, and in one patient it took three doses. Obviously across varying dose levels.

The challenge: if $DTIL is eliminating cccDNA, that will lead to loss of pgRNA in the blood. However, pgRNA is not always detected in the blood. HBV DNA undetectable is an FDA approvable endpoint and so is HBV DNA + HBsAg undetectable. So, what if a patient demonstrates complete pgRNA loss that translates to stopping NUCs with HBV DNA remaining undetectable but HbsAg is still present from iDNA? Does the HBsAg (that has been drastically reduced) still being expressed from iDNA hurt the patient? Billion dollar question right there.

Who better to answer that question than Dr. MF Yuen?

I reached out to Dr. Yuen via email and asked “In your professional opinion, can HBsAg produced from iDNA in a Hepatitis B patient harm them if their cccDNA is eliminated?”

Dr. Yuen responded: “Theoretically, HBsAg produced from iDNA should exert no harm to the liver.”

First & foremost, big thank you to Dr. Yuen for being willing to respond to an email inquiry. The answer received from Dr. Yuen is obviously hedged by “theoretically” because no previously studied tool has been able to eliminate cccDNA like this, therefore this question has not been answered in humans. It seems that Precision will be able to paint that picture at their AASLD update later this year. If indeed this theory translates to practice, this could be groundbreaking.

What about the other patients who did not have pgRNA detectable in the blood at baseline? Another question that must be answered with more research. Dr. Yuen noted during the Q&A session that he “guaranteed” that these patients had pgRNA detectable in the liver at baseline, meaning a biopsy would have had to be the method of detection and measurement here. Is that clinically feasible long-term? No. However, $DTIL will need to get biopsies on patients who are pgRNA- in the blood at baseline and also prove that they are eliminating the pgRNA via cccDNA elimination and correlate that to HBV DNA loss after NA stoppage — exactly what they’ll have to do in the patients with the blood biomarker just with a biopsy.

pgRNA outperforms other biomarkers (e.g., HBsAg) in predicting the effective and safe withdraw of NAs (Terrault NA, et al. J Infect Dis. 2025;231(5):1290-1298.).

The biopsy data:

Two patients (both in cohort 2) have consented to a liver biopsy thus far. Patient 5 (previously disclosed at a high-level) had a pre and post treatment biopsy and patient 6 had a post treatment only biopsy.

The effect of cumulative, repeat administrations were clear. PBGENE-HBV potently eliminates cccDNA which results in loss of viral transcripts. Furthermore, as a secondary mechanism — PBGENE-HBV turns off the polymerase function which results in complete viral inactivation. In plain language, it stops the packaging of pgRNA and shuts down the ability for pgRNA to create new HBV DNA.

Patient 6 (blood detectable pgRNA at baseline) showed full pgRNA elimination in both the blood and the liver which further supports using blood pgRNA as an indication of pgRNA levels and cccDNA in the liver.

Safety:

In vivo gene editing is inherently subject to higher scrutiny because it is designed to alter a human’s DNA. It’s very good to see the LNP related ALT / AST spikes not also increase bilirubin. We certainly do not want a Hy’s Law situation with this program. It was also encouraging to hear Dr. Yuen verbally express that there weren’t any abnormal effects that were out-of-line with LNP delivery noting that the safety profile was “quite OK”.

Despite Cohort 3 having idiosyncratic grade 3/4 AEs, the new simple and mechanism related safety measures have mitigated hypotension and liver lab abnormalities moving forward — this seems that it should continue. Not having to make a “chemistry change” is key here. Some may recall Verve needing to shelve VERVE-101 and move to VERVE-102 to use a different ionizable lipid in their LNP — not the case here.

Next steps:

In summary, liver biopsies in combination with key blood biomarkers reflect cccDNA elimination

and support increased probability of cure after treatment with PBGENE-HBV. I look forward to $DTIL stopping NAs and testing for a cure in the patients with blood pgRNA eliminated first. Although these patients will have to prove 6 months of sustained HBV DNA elimination after stopping the background therapy (NAs), imo, if a patient sustains HBV DNA suppression 1-2 months after NA discontinuation — that is a very good sign because the NA washout period is fairly quick and NAs would be the only other possible suppressor of HBV DNA.

Concurrently, $DTIL will expand the number of participants in cohorts 4 & 5 to try to nail down the best dose combination to take this forward (seemingly as a monotherapy).

The Q&A section, in combination with what a competitor is doing also makes me wonder if $DTIL will explore adding HBeAg+ patients. As a reminder, they are only enrolling HBeAg- patients today. On slide 19 of their presentation, $DTIL also mentions that HBeAg+ patients have higher cccDNA, pgRNA, % of sAg from iDNA, and they verbally mention that it’s an earlier line population that their treatment could potentially benefit earlier and further reduce the change of long-term negative impacts from Hepatitis B. I am fully supportive of starting to enroll people from the HBeAg+ population to continue to PROVE the emerging trend that pgRNA loss in the blood = cccDNA elimination which means that you’ve suppressed HBV DNA.

The partnership piece. $DTIL has stated that they can take this clinical study through phase 2 without a partner. However, I would imagine that there are ongoing partnership discussions in this space. $GSK, $GILD, $RHHBY all natural domestic fits. I am admittedly less familiar with the Asian landscape but would also imagine there are partners based in China that could have interest given the heavy population of Hepatitis B patients in China. $DTIL also including the $GILD logo is no accident.

The readout from $GSK this week vastly beat other currently approved HBV therapies with a functional cure rate of ~19% (still short of the global goal of 30% by 2030). GSK has already submitted Bepirovirsen for approval in the U.S., Japan, Europe and China, with the FDA set to make a decision by October.

Could a Bepirovirsen + PBGENE-HBV be studied as a combination therapy? Bepirovirsen stops DNA replication because it breaks down (doesn’t eliminate) pgRNA, then stops the production of HBsAg, and acts as an innate immune stimulation mechanism. PBGENE-HBV could eliminate the cccDNA while Bepirovirsen takes down the HBsAG — especially if PBGENE-HBV ultimately needs to drive further HBsAg levels. IMO, the reality is multiple treatments working in tandem to cure the disease.

Finally, I have my eye on AASLD TLM in November for a significant update from $DTIL regarding the ELIMINATE-B trial.

Asymmetric competition:

The epigenetic silencing group. Tune Therapeutics had a late breaking oral presentation today at #EASL26. For those who don’t know, Derek Jantz (former $DTIL co-founder & CSO) is now the CSO at Tune after exiting Precision shortly after the Amoroso administration began. Topic for another day but imo he wanted to boil the ocean (they were in food, ex-vivo, many in-vivo research programs, etc.). Say what you want about Amoroso but he has focused the company. I haven’t always agreed with his means of raising capital but the company is now singularly focused on in-vivo gene editing (what they feel they do best) and I respect that. I also digressed a bit.

I’m not going to deep-dive Tune’s data as much as I did for $DTIL.

The approach that Tune is taking to Hepatitis B is a targeted epigenetic silencer that is delivered via LNP (using a guideRNA versus protein recognition like ARCUS). In essence, it is designed to silence cccDNA without cutting the underlying DNA. $DTIL cuts and completely eliminates, Tune silences. When I say that Tune silences it doesn’t remove the cccDNA, it just dresses it in repressive marks (methylation + compaction) The template is still physically sitting in the hepatocyte nucleus, intact, transcriptionally silent but reactivatable in principle. Whereas, gene editing (the $DTIL approach), destroys the template — nothing left to reactivate in the future.

TL;DR on the Tune data: fairly in-line with Precision’s IMO. Though they didn’t achieve the 100% threshold on patients achieving pgRNA undetectability. On the other hand, some of their cohorts only had one dose. Their safety profile is relatively in-line with Precision’s. Durability is a long-term question given the silencing approach versus fully cutting cccDNA. Time will tell. I could see a path where patients select the non-DNA-editing approach if these patients are able to take the next step and discontinue NAs and successfully achieve sustained HBV DNA undetectability. That said, I don’t see Tune talking enough about how this program aligns with FDA guidelines for an approvable endpoint. Time will tell. It’s still early — something to watch.

Before wrapping up the epigenetic silencing topic — Tune has a direct competitor in that space, nChroma, who dosed first patient in January using a similar, if not the exact same, approach as Tune. I believe this company also has ties to the famed David Liu.

I already talked about Bepirovirsen from $GSK. Again something that patients could choose over a gene editing approach. That said, I don’t necessarily view this as competition — rather something that could be used in tandem to achieve a viral cure if $DTIL is unable to get across the finish line as a monotherapy.

Aligos Therapeutics just sold its China rights to their phase 2 HBV treatment. It’s supposed to prevent HBV DNA integration and reduce cccDNA. I just don’t see this as a threat at this time. Good for them getting $25MM from Amoytop in exchange for China rights.

Cash position:

$DTIL had ~$125MM in cash & cash equivalents as of the end of 1Q26. The first quarter of 2026 also saw an earned $7.5MM milestone payment from $TGTX resulting from an azer-cel partnership that $TGTX is using to treat MS and now more.

In speaking to $DTIL leadership late last year, their cash burn is going to be ~$15MM/quarter at the moment.

As we all know, biotechs can be penalized by the market when cash position is too low. I hope this is not the case but I could see a path where $DTIL raises on the back of AASLD data later this year. Let me be clear, I can swallow a raise of $75-100MM @ a $1B valuation, versus a $75MM raise at a ~$75MM valuation (almost precisely what took place last November).

I would hope that $DTIL is actively pursuing mid to late-stage business development discussions to help with the cash position.

DMD program:

Unlike many other DMD gene editing / therapy approaches, $DTIL targets exons 45-55, which account for ~60% of DMD patients. It is one and done and is in-vivo. The best part is that they use a small amount of AAV to deliver relative to competitors and their full capsid ratio is largely higher, they’ve also shown evidence of satellite cell editing in pre-clinical models — driving permanence.

Micro-dystrophin programs have been mediocre to disappointing at best. $DTIL is aiming to create a Becker like phenotype which is ~85%+ of a full length dystrophin. There is an abundance of data to show this type of dystrophin offers functional benefit for humans.

$DTIL has an approved IND and is actively recruiting at Arkansas children’s with a world class expert leading the study from a clinic standpoint.

Where $DTIL goes from here:

The back half of this year remains catalyst rich for $DTIL. They continue to commit to a year end DMD update and we can all pencil in a AASLD TLM update in November for the HBV program imo.

I’ll be honest, I struggle to see the long-term path to independence for $DTIL without going through a series of additional dilutive events. I believe there is a path there for a big HBV partnership that provides sustainable cash to fund DMD to completion. However, I see a path to an exit via M&A starting to form potentially as early as 2027. Build the data story for HBV and DMD, exit to big pharma and use their balance sheet to expand the ARCUS platform to indications that aren’t currently accessible due to capital constraints. Clear path to $GSK, $GILD. $RHHBY would be one of the cleanest fits, imo — they’ve been active in DMD and HBV over the years. $NVS dark horse with past partnerships and a current undisclosed research program.

I’d like to hear thoughts from others as well, don’t hesitate to comment or reach out directly. This is going to be interesting at a minimum.

These thoughts are my own and I state my opinion. I own $DTIL stock. There is a lot of AI slop out there these days — I used AI in research but wrote this myself. I used em-dashes before they were cool.

@Stmkrs That’s the $1B question with the small amount of remaining cccDNA. Agreed on the treatment combination. I would imagine they can continue down the monotherapy path while simultaneously teaming up with someone like GSK to use a combo therapy.

@Bernard22190947 Good point about the market undervaluing ARCUS. The approach that $DTIL is taking to DMD should further prove key traits that set it apart. Showing safety by year end will be big and it’s icing on the cake if there are initial signs of meaningful efficacy from muscle biopsies.

Agreed on both companies learning as they go. Specially for Precision, I’m interested to see if they expand to the HBsAg+ population given that they started in the broader population of HBsAG- patients and still cleaned out pgRNA.

I understand what you’re referencing from the published literature — fair point. I just don’t believe what exists today fully represents what can occur when cccDNA is eliminated.

It’s a fair point. They received a follow up question about this as well on Wednesday. To which they responded that the group has largely held HBsAg declines with an outlier or two. I would have also preferred a median chart or something similar to what they showed during AASLD last year.

My understanding is that HBsAg produced by iDNA can still go up and down even if cccDNA is eliminated.

It’s something that $DTIL and potentially Tune will have the opportunity to set precedent for given the lack of ability to eradicate cccDNA in prior HBV treatments.

Both are basically saying ~“HBsAg levels from iDNA doesn’t matter as much if we can cut out or silence cccDNA.”

$DTIL very interested in this update on Precision’s ongoing ELIMINATE-B trial — an in-vivo gene editing trial targeting Hepatitis B.

https://t.co/j87JQRybW2

Looking forward to this $DTIL late breaking poster @ the EASL Congress in May building on liver biopsy mechanistic evidence of elimination and inactivation of cccDNA, first shared in November 2025.

The fact that M.F. Yuen, a world renowned hepatologist, is presenting it is not something to gloss over either imo.

In Precision’s business update on March 12th, they noted that they expect “additional clinical biomarker and biopsy data in the first half of 2026 and expect to have completed dosing in Cohorts 3, 4, and 5. This will inform selection of an optimal dosing regimen intended to support discontinuation of nucleos(t)ide analog treatment and progression into the Part 2 expansion phase of ELIMINATE-B.”

It will be interesting to see if we get an interim update around EASL26 for Cohorts 3, 4,and 5. Based on Cohort 3 progress at AASLD, dosing should be complete at this point.

https://t.co/PzFoqLf27W

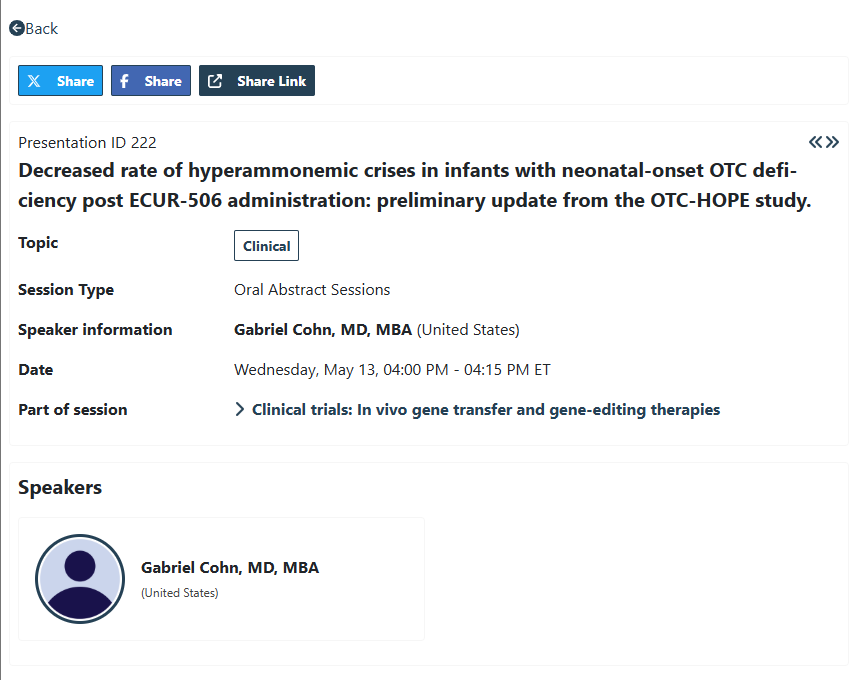

$DTIL partner iECURE shares additional data from the first 7 patients dosed in the ongoing OTC-HOPE study.

https://t.co/XR9wcP0jjc

Full disclosure, my friend @claudeai helped me with the summary of the linked presentation.

Efficacy (preliminary):

> Preliminary results continue to support advancement of ECUR-506 as a treatment for neonatal onset OTC deficiency

> 71% (5 of 7) of dosed participants have experienced zero HACs post-ECUR-506

> 60% risk reduction in the number of participants experiencing any HAC

> 52% risk reduction in annualized HAC rate (3.12 → 1.49 events/patient-year)

>Pre-dosing: 6 HACs over 701 observed days; post-dosing: 4 HACs over 981 observed days

Safety:

> Generally well tolerated; no TMA (thrombotic microangiopathy — a key concern with AAV)

> Transient Grade 2–3 transaminitis in 5 of 7 patients, non-dose-dependent, resolved with reactive immunosuppression

> One death from hypoxemic respiratory failure deemed unrelated to ECUR-506

Fairly detailed 18-month follow up data from the first patient dosed in iECURE clinical trial, OTC-Hope — using $DTIL editor, ARCUS. The complete clinical response remains ongoing in this patient.

More data in tap this week from the first 7 patients dosed in this trial. Scheduled to present at #ASGCT26 on Wednesday afternoon.

https://t.co/c9q9zuFpkT

💯. I’m making some assumptions here too:

> Assuming that 27 of the 38 doses occurred in cohorts 1-3 (3 cohorts * 3 patients per cohort * 3 doses per patient).

> As of 1/12/26, 3 patients had been enrolled in some combination of cohorts 4 & 5.

> As of 3/12, 13 patients doses across 5 cohorts; 30+ doses.

> As of 5/5, 16 patients, 38 doses.

I’m concluding (speculatively) that 2/3 patients who were enrolled between AASLD and 1/12 have completed 3 doses @ the 4 week dosing interval.

With the late breaker @ EASL, I’m confident that we’ll see additional biopsy data that builds on the data shared @ AASLD from patient 5. I’d really like to see at least 1 biopsy from cohort 3 and potentially one or two of the patients enrolled post-EASL.

Very much hoping that the data builds nicely on what was shared at AASLD last year. $DTIL

$DTIL provides a business update & 1Q26 financial results.

Takeaways at a quick glance:

> 16 patients now enrolled in the ELIMINATE-B trial across 5 cohorts with 38 doses administered. Late breaking poster to be presented @ EASL in May by MF Yuen. Curious to see if $DTIL provides an update in addition to this poster, especially given that cohort 3 dosing likely concluded in 1Q26.

> $DTIL on the cusp of dosing first patient in their first in class in-vivo gene editing trial targeting DMD.

> iECURE data on tap @ ASGCT in mid-May for the first 7 patients enrolled in this trial using ARCUS to treat babies with severe neonatal onset OTC deficiency.

> $7.5MM milestone payment from $TGTX helps control cash burn for 1Q26.

https://t.co/trevMdZ6BZ

Precision BioSciences is expanding its global Phase 1 ELIMINATE‑B trial evaluating PBGENE‑HBV following clinical trial application approval in two European countries.

“Expanding ELIMINATE-B into hepatitis sites in France and Romania is an important step in the continued development of PBGENE-HBV, the only gene editing therapy uniquely designed to eliminate cccDNA,” said Cindy Atwell, Chief Development and Business Officer of Precision BioSciences. “Given the strong investigator interest in PBGENE-HBV, especially following the late breaker oral presentation at The Liver Conference 2025, these new trial sites will build on our existing global clinical trial footprint as we advance PBGENE-HBV through the ELIMINATE-B trial.”

To learn more, visit https://t.co/Ry9jmROaJv

$DTIL