With todays pre-CPI straddle at just $45/60bps (ref 7515) its clear that the market really isn't not pricing in much risk at all.

Despite my complaining about volatility-related risks, gamma remains positive for SPX & across top single stocks. Its a shock absorber.

Equity vol is just oil vol as you see by how the relationship changed after the Iran debacle started.

CL now +104...

I think VIX "outperforms" at some point. Good luck.

$SPCX has been draped in positive gamma from essentially IPO day until Friday.

Now we see negative gamma below to the downside, with "all over" neagative gamma after Friday OPEX.

This implies volatility ahead.

Prediction markets and binary options are back in the spotlight. Join our livestream today at 1pm ET with Mat Cashman, OCC Principal, for a breakdown of how these all-or-nothing contracts work — and why you should pay attention: https://t.co/43OFo7kIua

Vols are nearing record lows right as earnings season kicks off. Check out our weekly analysis for more insight as to what this next week could have in store for traders: https://t.co/S4hBuSupXv

SPX IVs are all now 10% for next week, with Monday sporting 8%. Meanwhile, NDX shows 20%s.

Yes, "the weekend effect"...but this term structure is still the lowest its been in the last 90-days - if not longer. Plus, SPX 5-day RV is 8%. Priced for perfection.

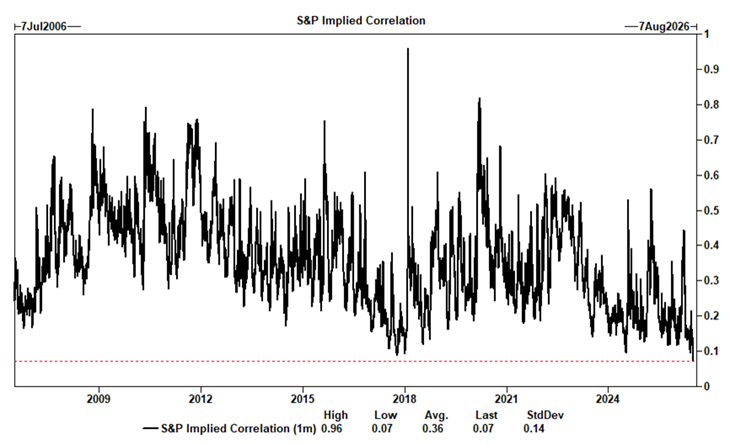

"With the VIX back to its lowest levels in more than a month, our Vol desk is focused on hedging opportunities as 1m S&P implied correlation is near its lowest level in 20yrs" - GS

In the top stocks the buyside is actually short gamma (dealers long) on net. That gives dealers positive gamma (blue)

The skew is an artifact of the right tail risk from these stocks going up 🍌s % for the last 90 days

The S&P put/call skew just collapsed to 0.71. Not a low. The lowest reading on record.

The 10-year average is 12. The 2020 panic peaked at 34. We're at 0.71.

What this measures: how much investors pay to protect against a crash versus betting on a rally. At 0.71, crash protection is essentially free. Nobody wants it.

Think about what that means. After two years of gains, at record concentration, with households at record equity exposure, the options market has priced hedging like insurance on a house that cannot burn.

History's lesson is consistent: markets don't crash when everyone fears a crash. Fear is the hedge. This chart says the hedge is gone.

Nobody buys insurance at the top.

That's what makes it the top?