Agree this is one of the more interesting underwritten parts of the $JBL story. The 1.6T LRO angle is real: mgmt said it’s entering quals, Intel transceiver assets gave them SiPh capacity, and II is scaling fast. But I’d be careful calling it ‘free Innolight’ yet. We still need evidence of hyperscaler PO / volume ramp, SIVE bottleneck economics, and margin accretion. At $38B, the stock already prices in a lot of AI infra; the next 40% likely needs qual success + FY27 estimate revisions, not just narrative discovery.

Vertiv ($VRT) is the non-optional physical layer of the AI buildout, every 100–150kW GB200/Rubin rack needs its liquid cooling and power distribution, and that demand is locked in via a record $16.5B+ backlog and 1.92x book-to-bill.

I expect shares to reach $410-500 (currently $300) as the market validates its structural story.

Don't buy here.

Stock is below both the 50MA in a clean lower-highs/lower-lows downtrend. If it falls to the $280–290 shelf and holds/bases, that's a buy; or if it reclaims the 50MA (~$314) on a green close with volume, that's the right-side confirmation buy.

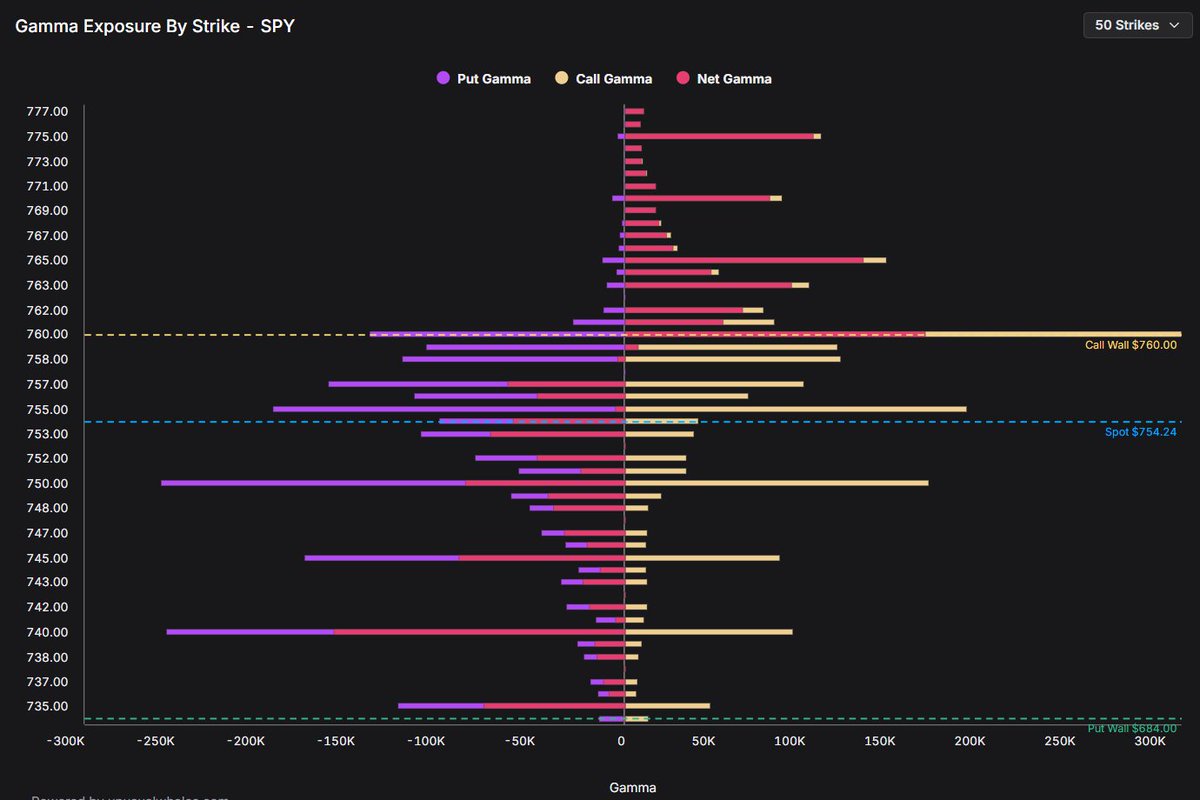

NON-ODTE CUMULATIVE NET DELTA AND NON-ODTE CUMULATIVE NET GAMMA ARE SHARPLY RISING AS WELL – THE MARKET HAS HEALED FROM FRIDAY'S SELL-OFF.

EVEN 0DTE GAMMA IS TURNING AROUND.

Updated my $COHR model.

Base case PT $460 and bull case $525.

Nvidia is running copper, NPO, and CPO in parallel. NPO and CPO are an additive new revenue layer stacked on top of the existing pluggable business, not a replacement, and $COHR 's $2B Nvidia partnership and LTA lock it into the laser content (CW lasers, ELS modules, fiber attach) inside those engines.

The real rerating catalyst is not the current quarter. It is the moment NVL576 and Rubin Ultra ramp in 2H27 and COHR's laser content revenue steps up non-linearly.

Victoria Hanrahan, Chief of Staff to the CEO, bought 44,682 shares (May 26 + 28) at a $15.81 avg, about $706K. Her first disclosed buy, confirmed in Nokia's 6-K filing.

She wasn't alone. Owczarek bought ~$1.1M, plus Fisk, Heard and others in May. Roughly $3M of cluster buying.

These buys hit near a 17-year high at $15-16, not at the lows.

$NOK

$Nokia ($NOK) Can Still Double

At $12.82, with forced repricing as the mechanism and optical allocation as the catalyst, it is a disciplined 18 to 24 month double with a credible path and a clear falsification trigger.

https://t.co/52adlUVtbn

I think my personal style of investing is a bit different, just some reflection:

It's inherently discretionary, based on stuff markets don't know yet. And a culmination of life experiences?

If you look at $AXTI, $RPI, $SIVE, $IQE and others.

Lot of it is guessing on unstructured relationships then seeing if it's right or not down the line.

$RPI is the perfect example:

1. Nobody really thought of Raspberry Pis for AI growth. Mainly people bought one or two just for class + education + hobbyist.

2. After OpenClaw, just noticed all my friends and people just buying Apple Mac Minis / RPIs for AI applications.

3. Found validation of that trend online with lot of people sharing video tutorials on AI orchestration with RPI.

4. AI was their ideal perfect growth vector, did some modeling, and thought it was compelling.

Earnings comes out and I was right.

Everyone in media was calling it a meme stock because there's nothing online that shows revenue growth from AI (was 14% forecasted revenue growth, turned out to be 58%, my projection was around 55%).

So it was a mix of guessing next industry trend (AI using lightweight hardware instead of GPU clusters), real life trends, then revenue forecasting off my guess.

For stuff like $AXTI:

1. Everyone called it a joke when I bought at ~$12. LLMs would hallucinate and say "hyperscalers/govs would have known about this by now and fixed this vulnerability with InP substrates"

2. Or would conflate very nuanced parts of InP substrate stack, where there's multiple different chokepoints in upstream processing.

3. So part of this was just discretionary based on what I've seen over InP substrate breakdowns, industry trends, etc.

4. Then also guessing the major supercycle was photonics (this was before everyone caught onto $LITE, and others). Or before you saw the $141B TAM projections from GS.

5. AXT owned 40% of InP supply chain, without them the supply chain just gets cripped).

6. All the "analysts" were forecasting steady InP substrate growth, few hundred million TAM, etc. or export controls.

7. Everyone kept trying to say $AXTI was overvalued based on TAM estimates. But if it's a few hundred million TAM you just think that's a joke and go into game theory over allocations.

8. Then I just had to guess, how much would this be worth if it were a NAND style bottleneck, what MC could it reach based on control, how much would hyperscalers price it as, etc.

A lot of the current research outputs from Goldman Sachs, or earnings reports from the Epiwafer companies, were confirmed after I published my piece on AXT. If you did research back then, lot of the same material /framing wouldn't have come up.

With stuff like $XFAB as you're seeing now, a lot of it is just pure guessing:

1. Not really any CPO materials, how much their MTP process makes in revenue, etc. Everyone online keeps saying they're not a photonics player.

2. But if you go through ASE docs or Gov websites, they all kinda cite XFAB as a major emerging player here.

3. $NVDA also evaluating them right now (maybe it's successful who knows).

4. No clear revenue around this area because their main silicon photonics process is still precommercial, but if you guess it's trying to create a EU supply chain to compete with $TSEM, once pre-commercial shifts to commercial, maybe similar but less volume contracts?

5. Then just seeing updates over the next few months to see if anything confirms this thesis guess.

_

I think a lot of information discovery still can be done with LLMs I'm seeing online. But it's also really hard to make a bunch of unstructured inferences based on unrelated material or even just trends you're seeing in real life.

So probably better to just do what's standard, eg. do valuation forecasting based on current numbers

Stuff like $AAOI, if they're projecting $471m/M h1 2027 and you see MC at $12B, probably undervalued might be a good idea to go long for next years.

Stuff like Samsung Electronics is easier, see what people are modeling for operating profits for 2027, 2028 then just seeing if it's undervalued or not at current levels.

Maybe something harder is $JBL. I haven't really seen any great volume numbers around 1.6T LRO, but you can just make a guess on how popular that might be then project how that might impact current MCs.

Or picking just good names everyone kinda agrees like $TSM, $INTC, $MRVL is also solid.

So a lot of things is just building up your life skills then applying that to markets. I don't think it's that can be taught with courses and stuff.

Of course, much of what I'm doing is just high conviction inference based on unconnected parts. Could always be wrong.

Leveraged funds are simultaneously: (1) near maximum short in S&P 500 futures, (2) at an all-time record short in SOFR (betting on higher-for-longer rates), (3) near extreme short in 30Y bonds, and (4) building short-vol positions in VIX. This is a consistent positioning profile for a market that has hedged aggressively against both equity downside and rate upside.

Everyone is bearish after Friday's bloodbath. They might be early.

Beneath the panic, the smart-money positioning data is flashing one of its most extreme readings in three years, the kind of setup that has preceded sharp reversals before.

The catch is that next week's collision of inflation data, record Treasury supply, the SpaceX IPO, and Kevin Warsh's first FOMC could either light the fuse on a face-ripping squeeze or confirm that the rate wall is here to stay.

This is the full breakdown of both scenarios, and the exact signal that tells you which one is winning.

https://t.co/xOJC7WISeK