My favorite part of $MFBP's 2026 proxy is when they tell us the Board will be paying themselves ~$2.9 million dollars this year as a special bonus. This compares to 2025 net income of $2.3 million.

"In January 2026, the Board approved the Compensation Committee’s recommendation of an aggregate special bonus equal to five percent of the ECIP Discount, payable upon the successful redemption of the ECIP." -- pg. 12

https://t.co/IAn5AQY6k5

X-Cap has requested permission from the banking regulators to increase its ownership stake in $MFBP to 14.99%.

https://t.co/zY02xgmmUl

https://t.co/gXRnQTvuBD

$MFBP's quarterly results for Q3 '25 are out and non-interest expense is down an impressive $0.5mm from $4.6mm in Q2 to $4.1mm in Q3! That's $2 million in annualized cost savings!

While there is certainly an opportunity to further optimize non-interest expense, Q3 results show great progress thus far! Great work M&F team!

$BFCC $BYFC $CBOBA $CZBS $HRBK $IBWC $MNMB $NMBF $PCB $PDLB $SFDL $UBAB #ECIP #ECIPBanks

Duane Pelkey, $GOVB's newest independent director, continues to model excellent Director leadership -- increased his ownership stake again yesterday at a price of ~$15 per share

First $GOVB Director open market purchase in years -- excluding the second-step conversion purchases (which aren't really open market), it's the first time since 2008.

Thanks Duane for setting a great example for the rest of the Board!

Caitlin Long: "... I also received two independent confirmations while in DC that the DOJ has opened an investigation into debanking"

$SI $SICP $SICPQ $SBNY $SBNYL

I CAN'T STOP THINKING ABOUT something I learned during #dcfintechweek: the Biden/Warren crew had a *strategy* of telling #crypto companies to get regulated solely as a means to gain information they could use to kill us with prosecutions, defamatory denials & enforcement actions. FOLKS, IT WAS DONE DELIBERATELY & IT WAS PLANNED😡. The social contract between the govt & the governed breaks down when the govt weaponizes regulation to entrap people who operate within the law, albeit differently than incumbents. Separately but related, I also received two independent confirmations while in DC that the DOJ has opened an investigation into #debanking. I'm glad, and hope @pmarca is glad too. It's time for *REAL* accountability.🙏

First $GOVB Director open market purchase in years -- excluding the second-step conversion purchases (which aren't really open market), it's the first time since 2008.

Thanks Duane for setting a great example for the rest of the Board!

$GOVB announces their second share repurchase program for another 5% of shares outstanding (just 7 months after their first one) -- thrilled to see it!

https://t.co/2LkZjHNN4N

$GOVB arguably has the most upset shareholder base of any thrift that's converted in the past 5 years

$NSTS $PDLB $BCOW $FSEA $CULL $CLST $AFBI $TCBS $MGYR $NECB $PBBK $BVFL $ECBK $WMPN $BLFY $MSBB $PFSB $CPBI $SRBK $TCBC $NBBK $EWSB $VWFB #thriftconversion

$FREVS annual letter to shareholders released today.

"... we are actively evaluating credible acquisition proposals for our properties and exploring all viable strategies."

As a reminder, the company attempted to voluntarily liquidate in January 2020, but the announced buyer of residential RE portfolio refused to close as COVID unfolded. The related litigation finally concluded last summer in the company's favor. Chairman (and largest shareholder) is now 76 years old.

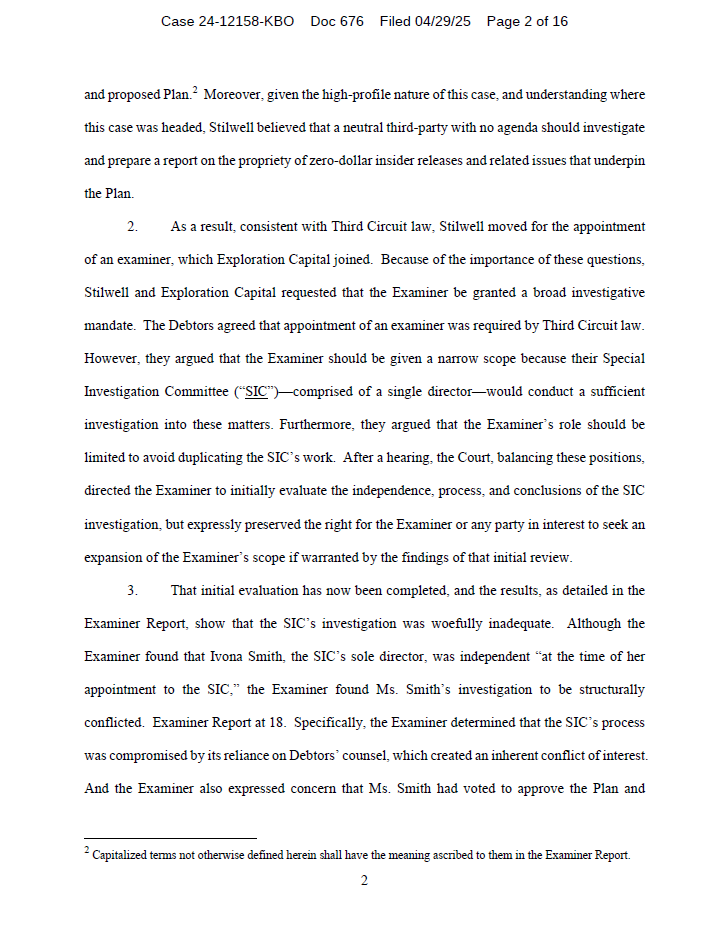

Stilwell and X-Cap filed a joint motion to expand the scope of the Silvergate Examiner's investigation given the Examiner's finding that the Company's internal investigation was not only flawed, but structurally-conflicted.

https://t.co/FNpbVv5bd0

( $SICP / $SICPQ )

$GOVB share count is down an impressive 4.4% in the first quarter of the calendar year (1,106,790 --> 1,058,399 shares). The company is aggressively executing the share repurchase program it announced in December 2024.

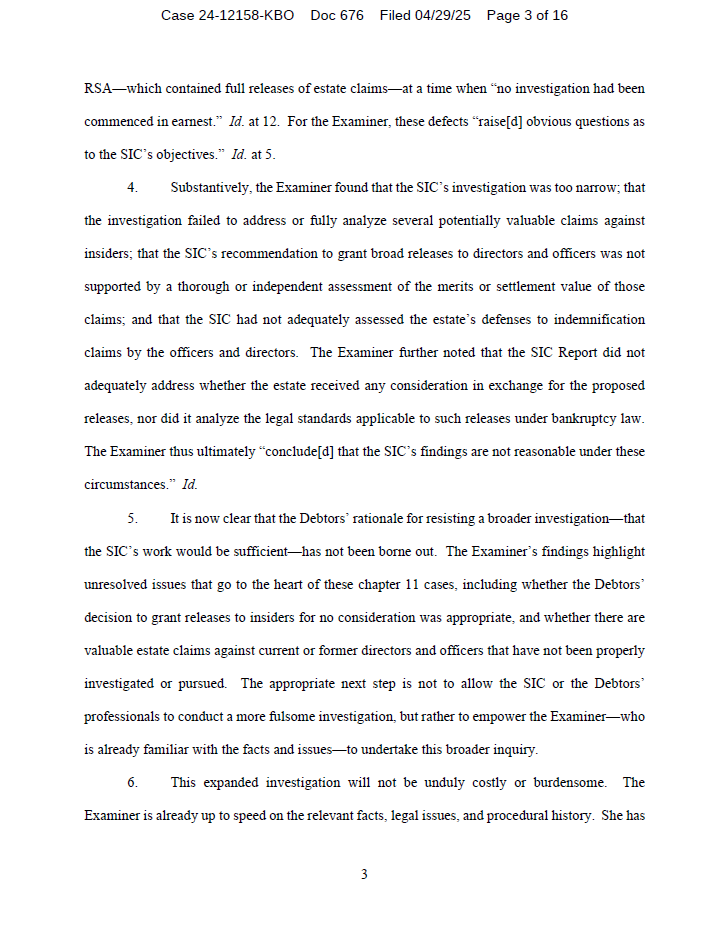

For those who may have missed it, the Silvergate Examiner Report was absolutely scathing of the Company’s purported internal investigation of the Company’s legal claims against current and former directors and officers. Moreover, the report lambasted the Company’s attempt to grant broad releases of potentially valuable claims against directors and officers FOR FREE.

Ms. Ivona Smith (the sole member of the “Special Investigations Committee”, that was handpicked by the four potentially liable directors to allegedly investigate their and the other directors’ and officers’ wrongdoing) never even formerly engaged her own legal counsel (i.e. there was no signed engagement letter). Instead, she used the company’s legal counsel Richard Layton Finger. The Examiner notes, “RLF’s simultaneous role as both Debtors’ counsel and SIC counsel presented a structural conflict.”

Perhaps most telling in my opinion, of Ivona Smith’s lack of commitment to impartiality, was the fact that she voted to approve the proposed Chapter 11 Plan which included broad releases for the potentially liable directors and officers, BEFORE she had even commenced her investigation in earnest.

Specifically, the Examiner Report states that on September 13, 2024 (four days before Silvergate Capital filed for Chapter 11), Ivona Smith voted with the rest of the Board to approve the Chapter 11 Plan, and that: “notably, the Plan provided broad releases by the Debtors and other parties of certain ‘released Parties,’ which include the Debtor’s former and current directors and officers”, and that “neither the release provisions in the Plan nor the definition of Released Parties contain any exclusion or limitation based on the outcome of any investigation or action.” The Examiner further notes that “no investigation had been commenced in earnest, much less completed, at the time the Petition and Plan were filed”

Lastly, the Examiner Report contains a few other gems worth noting:

- “The [SIC] Report’s recommendation that the Debtors release claims, especially derivative causes of action, without consideration from the parties to be released, is not reasonable.” (page 37)

- “The [SIC] Report discusses only certain potential estate causes of action, while overlooking others.” (page 5)

- “The [SIC] Report does not discuss any defenses that the estate may have to indemnification claims, or how releases might impact those defenses.” (page 6)

- “The [SIC] Report’s conclusion that Lane had no knowledge of, or was willfully blind to, the FTX intercompany transfers on the SEN is therefore not compelling.” (page 30)

- “There may be viable duty of care claims against Lane, Fraher, Sabins, and Pearson that are not subject to exculpation.” (page 37)

- “RLF’s activity largely consisted of reviewing information provided by Cravath and RLF did not seek to expand the SIC’s fact finding beyond the recycled information.” (page 17)

- “However, as of the date of this report, not all documents requested by the Examiner in the January Document Request have been produced.” (page 15)

( $SICP / $SICPQ )

https://t.co/Zuyi2fWTmg