Hey @VPrasadMDMPH if you’re so upset by drug prices, despite them being out of the purview of the FDA, maybe you shouldn’t put up more roadblocks and skyrocket the price of drug development. Just a thought $CLPT $QURE

I keep hearing people referring to "7" cases of cancer in the high dose arm for $ABVX. I get it - that's what they technically showed in the table, but in observing a lot of conversation about this I gather that people don't actually realize what really matters there. I am strongly of the opinion that there are really only 2 malignancy cases that matter for adjudication - the prostate cancer and breast cancer cases.

I initially started talking about these cases as "the 2" cases from the very beginning because I assumed that everyone would be on the same page that these were the only 2 that mattered...but I've found that people really are considering this as a case of *7* full blown malignancies in the 50mg arm...This is just not correct.

Let's break this down.

First of all, they're counting "colonic dysplasia" in this table as one of the "malignancies". I cannot stress this enough: Colonic dysplasia is, by definition, LITERALLY not cancer. This is actually an unequivocal point that I don't understand how it could even be up for debate.

"Dysplasia" is a "precancerous" lesion. Cervical dysplasia, colonic dysplasia, melanocyte dysplasia. Terms exist for these PREcancerous findings because they are, by definition NOT CANCER (otherwise, if they were cancer, we'd call them cervical cancer, colon cancer, and melanoma)...

Dysplastic lesions, not being cancer, often regress on their own or simply never evolve into cancer, staying in the "dysplastic" state until death. However, if they *do* become cancer, they do so through a process that is called "malignant transformation". Literally, something that is NOT malignant TRANSFORMS into something that is.

Why did the ABVX management team include this in the list of "malignancies"? Honestly, I don't know. I think it is an evident mistake, and a strong piece of evidence that they didn't think they'd actually have to explain away a "cancer signal" in this dataset because their analysis of the data told them that there isn't one. If they were worried that the market was going to interpret these data as a catastrophic malignancy risk (which, make no mistake, is what the current low $70s price tag is assuming), they would've likely adjudicated this more thoroughly and left the "malignancy" that is by definition NOT malignancy off of the "malignancy" table...

So that is tossed out easily IMO. 6 cases left now. 4 of those are NMSC (non-melanoma skin cancer). I gather that people are dramatically overestimating what a diagnosis of NMSC means. Far be it from me to minimize NMSC (since it is what I treat for a living as a dermatologist), but guys....this is NOT in the same category as ANY other malignancies. NMSC is a milder category of its own, and I don't mean that as a matter of opinion. Literally, "non-NMSC malignancies" is a distinct endpoint used to gauge risk of "serious" malignancies in clinical trials. NMSCs are left out of that category because they almost never are "serious" - certainly almost never life threatening.

Here's an exercise anyone can do to drive this point home. Google, or ask an LLM "what are the 10 most common cancers in the United States?". They are all going to give you the same answer: Breast & prostate will be the top 2 at slightly >300,000 cases/year.

So breast and prostate are the #1 and #2 most common cancers according to every source...except, those sources either ignore completely or footnote at the bottom that there is a type of cancer 15x more common...NMSC!!!

The point? Ubiquitously, NMSC isn't even included on the list of "most common cancers" because they're frankly in a separate category altogether from cancers like breast and prostate. It actually is controversial whether or not it is even possible for basal cell carcinoma to metastasize, and (aside from transplant patients), CSCC is almost never fatal unless left ignored/untreated for years (people ignoring a giant bleeding skin cancer is perhaps more common than you'd think, but not happening in any clinical trial patients).

These 4 50mg NMSC cases (vs 1 in the placebo group) are a not representative of serious malignancy risk even if the market is acting as if they are...they are absolutely in milder a category all their own, and lumping these all together is a mistake.

Again, if people think these 4 NMSC cases are some scary life threatening event, they're just flat out wrong. There are >15x more cases of NMSC than breast cancer in the US/year, yet >10x more breast cancer deaths occur in the US per year.

Again, not to minimize my own career too greatly, but almost *always* NMSC are removed by VERY simple, ~10 minute procedures under local anesthesia. Cutting out (or scraping away) the lesion typically takes me around 60 seconds, and the bulk of the procedure is actually spent stitching the patient back up. Drive yourself to the office, drive yourself home, local anesthesia, under an hour, you're cured. Hell, in many places in Europe it is actually standard practice to not even "treat" a basal cell carcinoma! On many body locations they are simply biopsied, and once diagnosed they are considered cured by the biopsy itself!

It has become very clear to me that people are thinking that these NMSC cases are highly relevant cases of severe, potentially fatal cancer. They simply are not. There are *millions* of these in the US per year and most are treated with <15 minute procedures. These are in a TOTALLY different, far less serious category of "cancer".

So again, why wasn't $ABVX prepared to discuss/explain this? I legitimately think they did not expect to need to. They may have overestimated the market's knowledge here and underestimated its potential for a knee-jerk reaction to the "C-Word". It's a mistake, yes, but it ultimately doesn't change the profile of the drug.

So, I think we have compelling cases to write off the colonic dysplasia (literally not cancer) and NMSC cases, as I have usually found to be standard in these situations.

That leaves the breast and prostate cancer cases. Again, the otherwise #1 and #2 most common cancer types...funny how that worked out! I sincerely do not believe that these two cases alone represent a signal against 0 in the placebo arm. This is textbook small sample statistical noise, ESPECIALLY for a drug with no mutagenic risk AND no immunosuppression (literally, HOW would this drug even be causing cancer then???).

However, clearly the market will want more info here on these two cases.

Hopefully the market will wake up to the points above (that $ABVX and I mistakenly thought were obvious) highlighting that the colonic dysplasia and NMSC cases can be almost completely written off. After that, hopefully $ABVX can give us more info on these two "legit" cancer cases (breast and prostate).

Yes, they should've been ready to do so on the call. they messed up, but let's see what the details show. Some are saying we will see updates sooner than the October conference like they initially guided for on the call (at which point they clearly did not expect the market to be freaking out at all).

After that, we also need to see the data from the 50mg "escape/placebo" arm that was not part of the primary efficacy analysis. That's is own topic of conversation, but that could significantly rewrite the narrative (now that $ABVX is aware a narrative needs to be rewritten after it got away from them).

I think the market thinks they are hiding these "escape/placebo" arm 50mg patients' data. I believe they were just totally caught off guard by the market's reaction to the "cancer signal" here and didn't think they'd need to have that dataset ready to prove there's no cancer risk (they thought the initial dataset spoke for itself...I agree, but so far the market clearly doesn't).

There should be several hundred patients worth of extra 50mg patients in that group. Ideally they can move up the release of that dataset to help qualm the market's fears and try to prove they aren't trying to hide anything there. Depending on the sample size there, we should very likely expect a few "cases" there too, but if the rate comes in lower than the original 50mg data we got, this narrative could snap back rapidly. Let's hope!

@laurencurehd@nyahphengsitthy We know $REPL had their meeting and reversal already, no melanoma organization invited either. Read through could be that $QURE had a positive type B meeting already with an alignment to be PR’ed soon

@johnarnold You wasted your political and actual capital for your cronies to all get kicked out and their awful work reversed immediately, hope you enjoy hell buddy!

Biopharma companies, investors and patient advocates have grounds for believing that @US_FDA decisions under Makary, Prasad that appeared final a few months ago may be reversed, says @steveusdin1 https://t.co/soTo7BFeU4

I have 100 shares as a tracker, covered calls have a hell of a premium with the equity being +-10% every day since IPO basically.

It’s fuckin expensive and could trade down to single digits on valuation but I view this IPO as a test on the whole space. The blowout Friday which we have few details of was the first sign cape station might be delayed hence the big selloff Friday and today. If it stays on track, generates 500 MW by 2028, capex comes down (already forecasting 6k/kWH for the phase 2 of cape) and wells decay as slowly as predicted then the market will pour money into this until they grow so fast it isn’t cheap. Don’t mind having a tiny percent of exposure until we know more in 24 months

I don’t know I don’t follow it too closely. AMT-130 1 year data taught without a doubt us that the sham group was able to improve after 12 months, which shows me that this data isn’t particularly exciting at this point. All we really know is blood mHTT levels are down but that’s not an effective assay either.

@AdamNa81@DesertDweller93@uniQure_NV 12 months is irrelevant for cUHDRS and they draw mHTT from blood+ no NHL data. Genuinely hope it works for the community but there’s not really much of a sign it does yet.

History shows it probably doesn’t

They can and should keep issuing equity and debt for a long time. Highly intensive growth capex businesses with minimal maintenance capex should pull whatever triggers they can to access capital, especially in a white space like this. Remember that their adj FCF was 6.4m this quarter.

Issuing equity isn’t a problem if they can keep expanding their fleet rapidly and slow down growth in a decade and turn on maintenance capex mode and throw out a shitload of recurring FCF

Huge H/T 2 @peter_mantas for all his biotech work. 🙏

Dude knows his shit. With a good shot a biotech bubble ahead, invaluable service w/Back of the Napkin

Recently got the conviction on $QURE from his research, and his conviction through the saga is highly impressive.

#ClearPoint Neuro Enters into 10-year Focused Ultrasound Development Partnership with Sungkyunkwan University, South Korea, Further Expanding Our Drug Delivery Ecosystem and Global Footprint - Read More Here: https://t.co/ubbC5bFV6m

#CLPT

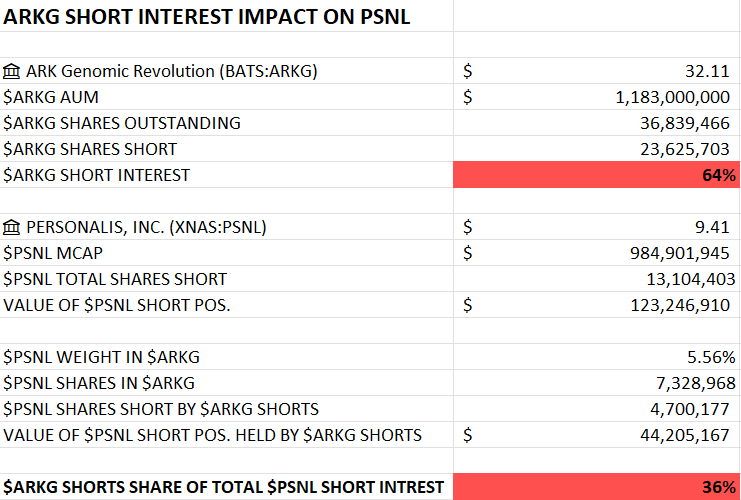

Updated with the latest data and it's quite🥜. $ARKG short interest is sitting at 64% of AUM. With $PSNL at 5.56% ETF weight, that shakes out to 4.7M shares indirectly shorted by people shorting the ETF. Combine this mechanical bid (if people should cover their $ARKG shorts) with the generally high short interest of 13M shares and genuinely great momentum for $PSNL with 4 reimbursements and more in the pipeline (beat & raise as far as the eye can see) and you are sitting on an explosive setup for the stock. Strap in fellas.