🧵 1/ The deadline for institutional reporting is TODAY.

-Track every fund's holdings

-Find the changes in their positions

-Get your notifications/alerts set up

-Filter the best performers on the quarter, and over time

-Dive deep in the details of every fund

-Create your own baskets of funds...

ALL IN ONE PLACE. DETAILS BELOW

https://t.co/JzkJjrgLtz

Here's a comprehensive breakdown of Macy's $M 's Q1 2026 report — strengths, weaknesses, and stock catalysts:

---

📊 Macy's Q1 2026: In-Depth Analysis

✅ STRENGTHS — Bullish Catalysts

1. Revenue & Comparable Sales — Beating Expectations

Total net sales: $4.7B, up +1.8% YoY (despite ~$40M headwind from closed stores)

Comparable sales: +3.0% — strongest Q1 in 4 years, 5th consecutive beat

Go-forward comp sales: +3.1% — the core, investable business is clearly accelerating

2. Bloomingdale's is a Standout

Comparable sales +10.2% — 7 consecutive quarters of growth, record Q1 sales

This luxury segment commands higher margins and stronger pricing power — a hidden gem inside M

3. Bluemercury Momentum

Comparable sales +6.4% — a high-margin beauty brand in structural growth mode

4. EPS Upside

GAAP diluted EPS: $0.23 vs. $0.13 prior year (+77% YoY) 🔥

Adjusted EPS: $0.13 vs. $0.11 — above guidance

Full-year Adjusted EPS guidance raised to $2.00–$2.20 (from $1.90–$2.10)

5. Guidance Raised Across the Board

| Metric | New FY2026 Guidance | Previous |

|---|---|---|

| Net Sales | $21.5B–$21.75B | $21.4B–$21.65B |

| Comp Sales | +0.5% to +1.2% | -0.5% to +0.5% |

| Adj. EPS | $2.00–$2.20 | $1.90–$2.10 |

6. Strong Balance Sheet & Shareholder Returns

Cash: $1.3B + $2.0B undrawn credit facility

No material debt maturities until 2030 — zero near-term refinancing risk

$50M buyback + $50M dividend in Q1 alone

$1.1B remaining buyback authorization → continued EPS accretion

7. Credit Card Revenue Surging

Credit revenues up +11.7% to $172M — strong consumer credit health, a high-margin stream

8. Technical Setup

Above both 50-day and 200-day SMA ✅

RSI at 63.3 — bullish but not yet overbought

Only -0.11% from 52-week high → price is at a breakout zone

---

⚠️ WEAKNESSES — Risk Factors

1. Gross Margin Pressure

Gross margin: 38.9%, down 30 bps YoY

Entirely attributable to tariff impact (30 bps); excluding tariffs, margins were flat

But tariff risk is not going away — H1 guidance assumes heavier tariff burden

2. Adjusted EBITDA Margin Contracting

Q1 Adj. EBITDA: $290M (5.9%) vs. $304M (6.3%) in Q1 2025

Despite revenue growth, EBITDA dollars and margin both declined — SG&A investments are eating into operating leverage

3. SG&A Creeping Up

SG&A: $2.0B, up $39M YoY — ongoing spending on Reimagine 200, digital, and luxury build-out

As a % of revenue: flat at 39.9%, but absolute cost inflation limits near-term margin expansion

4. Macro & Inventory Risk

Inventories up +3.6% YoY — management says it's "well-positioned," but in a consumer slowdown this could turn into a markdown headwind

Full-year guidance explicitly flags macro/geopolitical uncertainty on discretionary spend

5. TTM Revenue Still in Decline

TTM revenue: $22.6B, down -1.7% YoY — the store closure drag is real and will continue weighing on reported top-line

Net margin TTM: just 2.8% — razor thin for a $5.2B market cap retailer

6. Low Quick Ratio

Quick ratio: 0.28 — very tight liquidity excluding inventory; typical for retail but warrants monitoring

---

🚀 Key Stock Price Catalysts to Watch

| Catalyst | Why It Matters |

|---|---|

| Bloomingdale's & Bluemercury rerating | Luxury/beauty multiples >> department store multiples; spin-off speculation remains a value unlock |

| Buyback acceleration | $1.1B remaining on $2.0B auth; at current $5.2B market cap that's ~21% of float |

| Tariff resolution | Every 30 bps of margin recovery = ~$65M+ in gross profit |

| Comp sales sustaining above 2% | Proves the "Bold New Chapter" is structural, not cyclical |

| Real estate monetization | Hidden asset value in owned properties |

---

🔑 Bottom Line

M is executing better than it has in years. The top-line narrative is inflecting positively, Bloomingdale's is a genuine growth engine, and the balance sheet is clean. The key vulnerability is margin compression from tariffs and SG&A investment — which means the bull case depends on cost discipline and tariff relief in H2 2026.

At $21.67 with a P/E near ~9x forward earnings ($2.10 midpoint), the valuation remains deeply discounted to the S&P — suggesting the market hasn't fully priced in the turnaround yet.

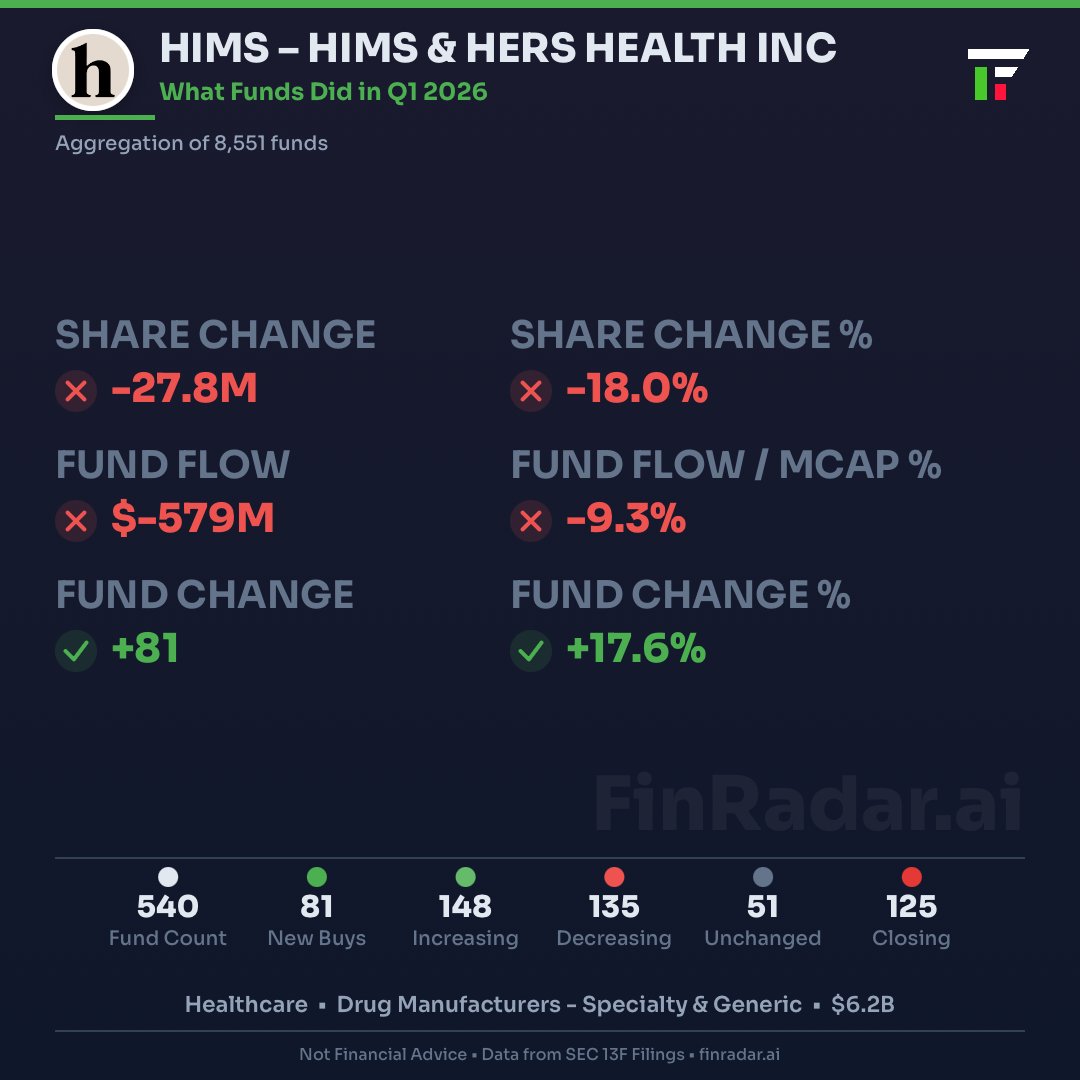

Good job! careful as many funds report their positions /1000 sometimes, and that can ruin your math or silently generate flaws in the data. Also sometimes a company CUSIP will change, you would see that the fund closed a position (untrue). Also careful with stock splits/reverse splits, they will mess the data...

A very few of the nightmares I had when I coded my platform. Fun to have though!

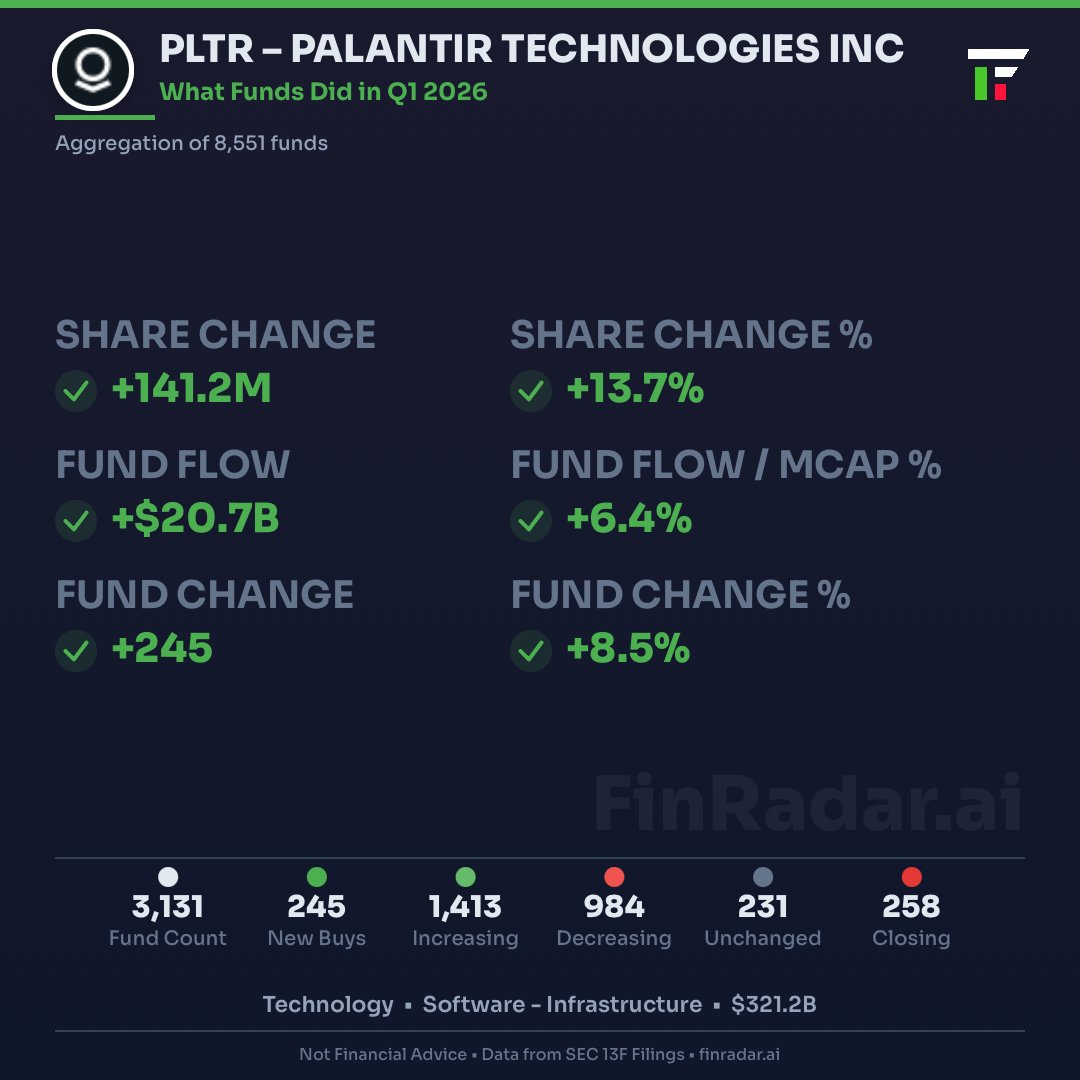

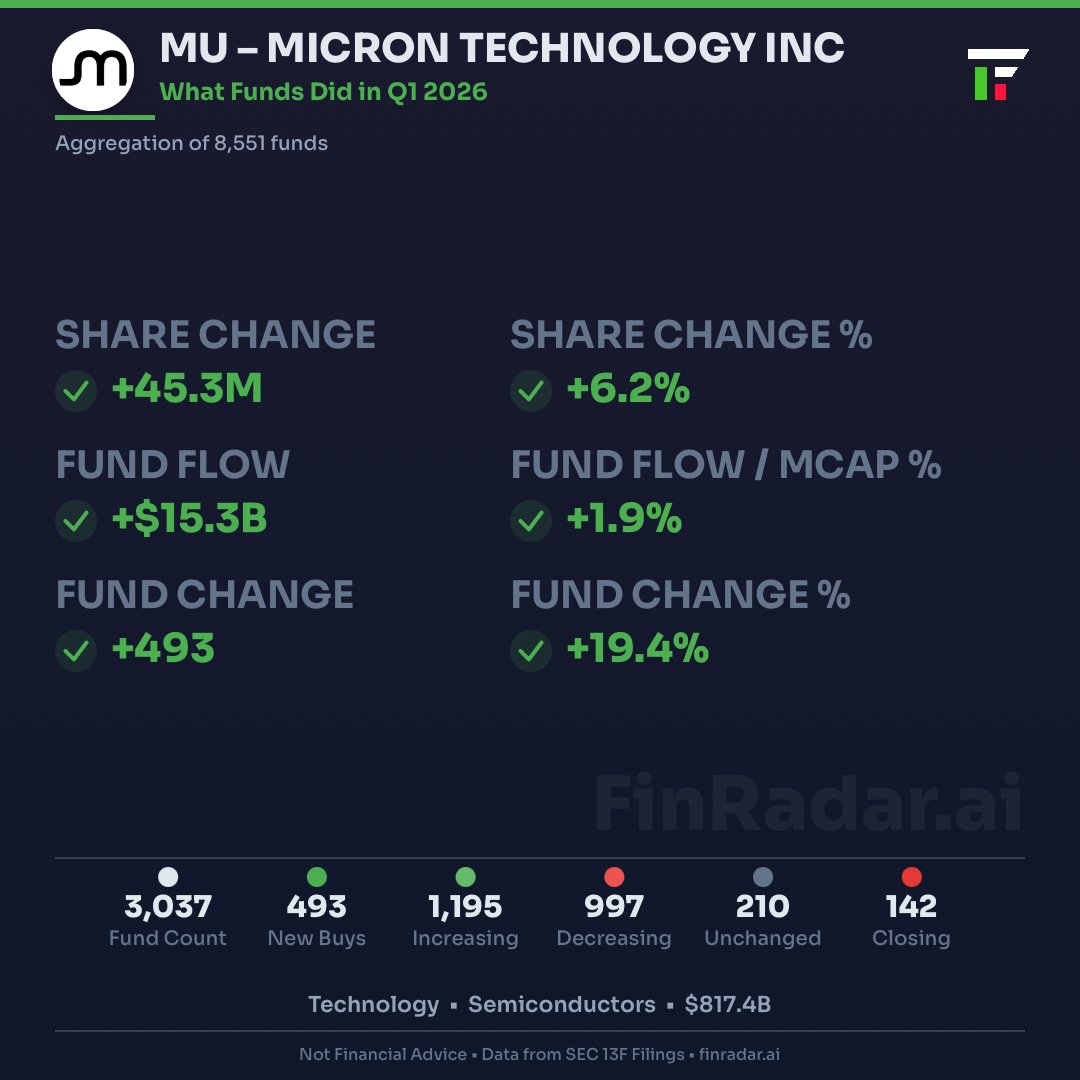

@SJosephBurns@grok Thought this would be of interest to you Steve. We aggregate all 8.5K+ institutions as they come. Also, this is where $MU for example stands.

https://t.co/wDhUuC5Lbq

Some of the healthcare stocks with the heaviest institutional loading based on total share increases, $ flows, $ flow relative to the market cap (from all filers)

$TENX $NKTR $DRUG $ALXO $ SABS $ WAT $AVTX

Full list on the website for every sector or industry

ICAHN Q4 2025 13F BREAKDOWN — $8.55B portfolio, 12 positions

---

PORTFOLIO CONCENTRATION

77.4% Energy.

Top 3 holdings ($IEP + $CVI + $UAN) = 82.7% of the book

---

MAJOR MOVES

INCREASED (2)

$CVI +1.1% (added 783K shares) — doubling down on his own refiner. Now 28% of portfolio. $2.4B position.

$SD +0.7% (added 36K shares) — small but consistent accumulation in SandRidge Energy

DECREASED (1)

$SATS -58.1% (cut 1.95M shares) — massive trim on EchoStar. Was a merger arb play after the DISH deal fell through. Icahn is walking away.

CLOSED (1)

$SWX GONE — exited Southwest Gas Holdings entirely. The activist campaign there ran its course. He got what he wanted, he's out.

---

THE THEMES

ENERGY CONSOLIDATION — $CVI, $UAN, $SD all held or added. Icahn is leaning harder into energy as a macro theme heading into 2025.

ACTIVIST EXITS — $SWX closed, $SATS slashed.

FORTRESS CORE — $IFF, $AEP, $JBLU, $CTRI, $CZR, $BLCO all unchanged. He's not rotating — he's holding and waiting.

---

BOTTOM LINE

Icahn cleaned house on two activist plays ($SWX, $SATS) and poured the proceeds back into energy. Pure conviction positioning. 77% energy exposure is a bold macro call.

PERSHING SQUARE CAPITAL MANAGEMENT, L.P. - TOP 10 HOLDINGS

New position in $MSFT , Increased position in AMZN

Q: 2026-03-31

via https://t.co/23nEFgCJhU