If Jordan Belfort wrote the $BIRD press release:

John, I need you to stay with me here, because this one is special.

The company was called Allbirds. Yes, the sneaker company. Wool shoes, soft branding, clean lifestyle, all of that. That was yesterday’s story, John. Yesterday’s market. Yesterday’s America.

Today? They’re selling the footwear assets, changing the name to NewBird AI, lining up a $50 million convertible facility, and getting into AI compute infrastructure.

Do you understand what I’m telling you right now?

This is no longer a shoe company. This is a GPU story.

They’re talking about high-performance compute assets, GPU-as-a-service, AI-native cloud solutions, enterprise demand, neocloud exposure. This thing went from insoles to infrastructure in one press release.

And John, that’s the beauty of it. Nobody cares what they used to sell. Nobody’s asking about sneakers anymore. The second you say ‘AI compute’ and ‘GPU assets,’ the whole thing gets reborn.

You’re not buying a footwear brand, John. You’re buying a pivot. You’re buying a narrative. You’re buying a management team that looked at a weak shoe business and said, you know what, let’s just become an AI company before lunch.

That, John, is vision.

And sure, maybe last quarter they were trying to move inventory. Maybe now they’re talking about hyperscaler shortages, compute scarcity, and long-term cloud opportunity like they’ve been in the data center business their entire lives. But that is not the point.

The point is the market loves reinvention. The market loves AI. And when you take a company that used to sell sneakers and tell people it’s now chasing GPU demand, suddenly nobody remembers the laces.

This is the kind of move that makes absolutely no sense, which is exactly why people will talk themselves into it all day.

So no, John, I’m not pitching you shoes.

I’m pitching you NewBird AI, a next-generation compute infrastructure platform with a dream, a ticker, and $50 million to go shopping for GPUs.

Now tell me that doesn’t sound bullish.

$TSLA

Tesla FSD is getting a bit ridiculous for me now.

I’ve been using 14.2 for the past month. Last night, I went to Walmart.

I came out of Walmart with my shopping cart, took my hands off the shopping cart for 2 seconds, looked for the button to press to turn on “autonomy,” and then legit let my shopping cart go by itself before realizing…the shopping cart doesn’t have FSD 😂

Like I actually am so used to getting in the car and not worrying about driving now that I subliminally thought the shopping cart would just autonomously find its way to the car without me having to do anything 😭

It’s getting ridiculous but also proving to me that I can never go back to driving without autonomy and once people experience this, it’s really hard to imagine life without FSD.

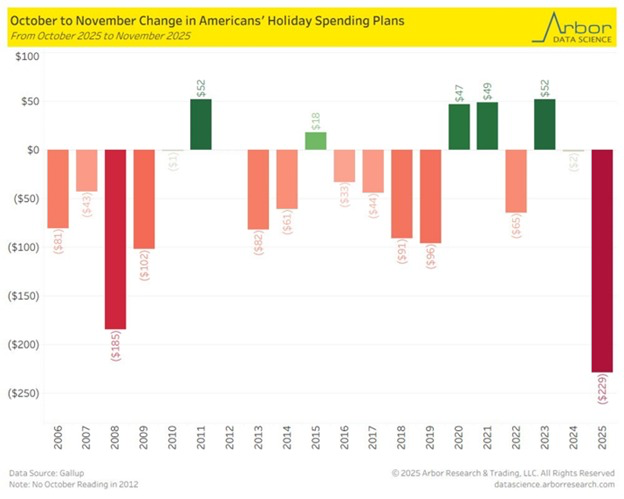

US consumer appetite for holiday spending is falling:

In November, Americans estimated that they would spend an average of $778 on holiday gifts, down -$229 from October.

This marks the largest drop in expected holiday spending in data going back to 2006, according to a Gallup survey.

This is also -$234 lower than last year’s November spending expectations of $1,012.

By comparison, during the 2008 Financial Crisis, the November decline was -$185.

Both high- and low-income Americans lowered their expectations last month.

Stagflation is weighing on US consumer spending plans.

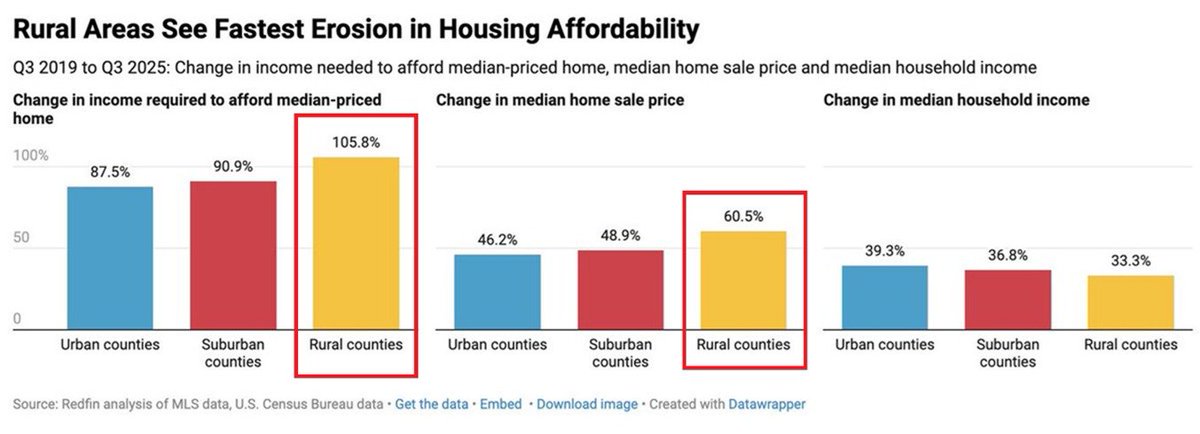

Rural home affordability has collapsed:

US homebuyers in rural areas need to earn $74,508/year to afford a typical home.

The required amount has surged +105.8% over the last 6 years.

By comparison, the income needed to afford a home has risen +90.9% in suburban counties, to $102,120, while urban counties have seen a +87.5% increase, to $118,300.

In other words, housing affordability has deteriorated the fastest in rural areas.

This has been driven by home sale prices, which have soared +60.5% in rural areas since Q3 2019, far above the increases of +48.9% and +46.2% in suburban and urban counties, respectively.

During the same period, median household income in rural counties has improved the least, rising +33.3%, compared with +36.8% and +39.3% in suburban and urban areas.

Affordability in rural America is horrible at best.

ELON MUSK ON X PHONE:

I am not working on a phone. I can tell you where I think things will go, which is that we’re not going to have a phone in the traditional sense.

There won’t be operating systems. There won’t be apps in the future... you’ll have … AI on the server side communicating to an AI on your your device … generating real-time video of anything that you could possibly want

It’s probably five or six years or something like that.

ELON MUSK ON X PHONE:

I am not working on a phone. I can tell you where I think things will go, which is that we’re not going to have a phone in the traditional sense.

There won’t be operating systems. There won’t be apps in the future... you’ll have … AI on the server side communicating to an AI on your your device … generating real-time video of anything that you could possibly want

It’s probably five or six years or something like that.

"I like to deal with people where I feel a one-page contract will do the job. If I have to have 50 pages in there to protect me against the guy I'm dealing with, I'll always wonder whether I needed 51." – Warren Buffett

The most ironic part about DeepSeek vs OpenAI:

1. OpenAI was developed by a non-profit and costs $200/month

2. DeepSeek was developed by a hedge fund and costs $0/month

3. OpenAI is actually closed-AI

4. DeepSeek is actually open-AI

Talk about a turn of events.

The gov’t has about 48 hours to fix a-soon-to-be-irreversible mistake. By allowing @SVB_Financial to fail without protecting all depositors, the world has woken up to what an uninsured deposit is — an unsecured illiquid claim on a failed bank. Absent @jpmorgan@citi or @BankofAmerica acquiring SVB before the open on Monday, a prospect I believe to be unlikely, or the gov’t guaranteeing all of SVB’s deposits, the giant sucking sound you will hear will be the withdrawal of substantially all uninsured deposits from all but the ‘systemically important banks’ (SIBs). These funds will be transferred to the SIBs, US Treasury (UST) money market funds and short-term UST. There is already pressure to transfer cash to short-term UST and UST money market accounts due to the substantially higher yields available on risk-free UST vs. bank deposits. These withdrawals will drain liquidity from community, regional and other banks and begin the destruction of these important institutions. The increased demand for short-term UST will drive short rates lower complicating the @federalreserve’s efforts to raise rates to slow the economy. Already thousands of the fastest growing, most innovative venture-backed companies in the U.S. will begin to fail to make payroll next week. Had the gov’t stepped in on Friday to guarantee SVB’s deposits (in exchange for penny warrants which would have wiped out the substantial majority of its equity value) this could have been avoided and SVB’s 40-year franchise value could have been preserved and transferred to a new owner in exchange for an equity injection. We would have been open to participating. This approach would have minimized the risk of any gov’t losses, and created the potential for substantial profits from the rescue. Instead, I think it is now unlikely any buyer will emerge to acquire the failed bank. The gov’t’s approach has guaranteed that more risk will be concentrated in the SIBs at the expense of other banks, which itself creates more systemic risk. For those who make the case that depositors be damned as it would create moral hazard to save them, consider the feasibility of a world where each depositor must do their own credit assessment of the bank they choose to bank with. I am a pretty sophisticated financial analyst and I find most banks to be a black box despite the 1,000s of pages of @SECGov filings available on each bank. SVB’s senior management made a basic mistake. They invested short-term deposits in longer-term, fixed-rate assets. Thereafter short-term rates went up and a bank run ensued. Senior management screwed up and they should lose their jobs. The @FDICgov and OCC also screwed up. It is their job to monitor our banking system for risk and SVB should have been high on their watch list with more than $200B of assets and $170B of deposits from business borrowers in effectively the same industry. The FDIC’s and OCC’s failure to do their jobs should not be allowed to cause the destruction of 1,000s of our nation’s highest potential and highest growth businesses (and the resulting losses of 10s of 1,000s of jobs for some of our most talented younger generation) while also permanently impairing our community and regional banks’ access to low-cost deposits. This administration is particularly opposed to concentrations of power. Ironically, its approach to SVB’s failure guarantees duopolistic banking risk concentration in a handful of SIBs. My back-of-the envelope review of SVB’s balance sheet suggests that even in a liquidation, depositors should eventually get back about 98% of their deposits, but eventually is too long when you have payroll to meet next week. So even without assigning any franchise value to SVB, the cost of a gov’t guarantee of SVB deposits would be minimal. On the other hand, the unintended consequences of the gov’t’s failure to guarantee SVB deposits are vast and profound and need to be considered and addressed before Monday. Otherwise, watch out below.

Excited to launch Pixel 7 and Pixel 7 Pro with our next generation Google Tensor G2 chip, which brings state-of-the-art #GoogleAI directly to the phone. And introducing our first Google Pixel Watch, with health and fitness insights from Fitbit.

https://t.co/u4YA6ZlReV