I personally think $SIVE can be the next $LITE.

In the past few months alone, we've seen:

1. Partnerships with O-Net pushing ELS into mass production

2. $JBL 1.6T LRO mass production signals with "relatively dramatic moats" for pluggables using Sivers.

3. $GFS SCALE reference level laser for hyperscalers with pluggable, NPO, CPO.

-> -> where $AMD and others went to GFS for CPO.

4. Ayar, which joined $NVDA NVLink for CPO

-> -> which removed Lumentum/Macom from their website and likely made Sivers their primary laser supplier.

-> -> AlChip likely Trainium win from Amazon price placement (Ayar's customer)

-> -> GUC rack level design in with Ayar.

-> -> Raised $500m for mass production by AMD, Alchip, Mediatek, and NVIDIA

5. ~ $AEVA starting HVM H2 2026.

6. $POET starting HVM H2 2026 with hyperscaler suppliers like Lumilens ("top 3 hyperscaler initial customer")

7. TFLN + $SIVE CW Lasers with Lightium

8. Likely direct relationships with $MRVL Celestial and CPO players like Lightelligence/Lightmatter.

9. Multiple new undisclosed relationships for pluggables following Jabil in their quarterly transcripts

With new Trendforce reports that $AMD and other hyperscalers are trying to source LTAs for CW laser sources, serving as a direct catalyst for independent CW sources.

So when hyperscaler suppliers from Jabil to O-Net are incentivized to mass produce as many as they can: That's very material for revenue for Sivers relative to current valuations, and it looks like just a waiting game.

Even in the past week:

- $SIVE raised an oversubscribed institutional round for volume ramp... This is very nuanced since Sivers is fab-lite so it's not going to in-house foundry capex to scale. Likely toward Win Semi and others (they mentioned other partners too), for laser scaling + foundry allocations.

So this is likely signaling material for revenue ramp is coming.

- Sivers also mentioned NASDAQ listing completion targeted in the next few quarters (probably H2 2026 or Q1 2027 is my est. timeframe).

This would fund M&A efforts, since it's impossible with the fundraising environments in local Swedish markets.

As for becoming the next $LITE:

M&A makes their lasers more valuable, so downstream IP acqusition -> into contract manufacturing like $FN, and others to make the full 1.6T pluggable or optical engines. Is how they get there, since laser array ASP scaling that people are modeling off of, wouldn't command a $60B+ valuations.

There's going to be a lot of bridge architectures like NPO/pluggables, etc and noise around certain architectural delays in the meantime.

But markets misunderstand laser companies like $LITE, $SIVE, $AAOI and others are used across different architectures compared to if you just look at certain passive optical components.

So markets see "CPO delay headlines" algos sell off laser companies that benefit from other architectures.

Being included in the pluggable 1.6T ramp to CPO scale out (Which Sivers is included in), helps bridge revenue waiting gaps until scale up inflection point H2 2027.

I'm personally holding long term, since I haven't seen a ~$1.4B company mapping to this many hyperscalers before.

TLDR:

- Waiting on volume ramps from different architectures to play out across their hyperscaler supplier mapping

-> 1.6T LRO/CPO scale out late H2 2026 start into high volume ramp 2027

-> H2 2027 CPO scale up volume ramp

- Waiting on NASDAQ listing likely H2 2026/Q1 2027 for M&A efforts to fully take off, unless Sivers get more creative with equity financing in the meantime.

I'm bearish on humans.

Hard to see people still having a job if humanoids come out at <$15K mass production.

No insurance, no JP Morgan HR cannon scandals.

And can do everything a person can, but better + 24/7.

Japan's Rakuten to establish joint venture with $ASTS to build out LEO satellite networks for Japan per Digitimes/Nikkei.

"The move is widely viewed as a strategic response to the growing influence of $SPCX Starlink in Japan"

If you're new to $AAOI:

It looks scary entering positions near ATH at $109 after a 175% YTD increase.

However, this looks like the photonics equivalent of $SNDK.

And it so happens the center of the optical transceiver supercycle...

At a $8.2B valuation we can look at projections:

(est. Capacity * ASP Projections)

Q2 2026: ~$312.1M

Q4 2026: ~$1.41B

Q2-2027: ~$1.53B

Q4-2027: ~$1.97B

If $AAOI ends up leapfrogging the $55B $LITE in revenue...

$8B MC looks a little absurd for revenue growth off 30-40% margins…

Re-rating potential is enormous.

Worst case scenario if they fail internal laser fab and buys off $COHR.

Is it ends up a Made in America Innolight / Eoptolink (Both $66B-$90B+ Chinese companies)?

The optionality of making the entire supply chain in America is understated.

$AAOI is one of my few high conviction longs aside from $SIVE and $LITE if they can deliver on projections.

There’s a lot of disinformation going around about $META “cutting capex” because they “overbuilt”.

This is an “if” they have excess capacity.

And it looks like the opposite right now:

Hyperscalers like $GOOGL are so compute constrained that they had to cut allocations to Meta back in March.

Since Meta was using too much for internal projects.

Meta was immediately constrained so it looks like they were forced to immediately sign massive $48B+ contracts with Neoclouds like $CRWV and $NBIS.

Meta is selling excess capacity if there’s any, especially since their large contracts are take or pay from the Neoclouds.

If anything, I’m expecting their guided capex to go up as they build out more independent capacity.

Wells Fargo: $META intent to sell excess compute is a positive signal around underlying demand and unit economics of AI.

“Despite this shift, we don’t expect a pullback in Meta’s capex or that overall compute needs are lower”

Regarding Neoclouds: WF thinks it validated the massive AI infra opportunity as well as acquisition opportunities. Despite any potential competition for Neoclouds.

I’m inclined to agree with Wells Fargo here and say markets completely misunderstood Meta’s excess compute comment.

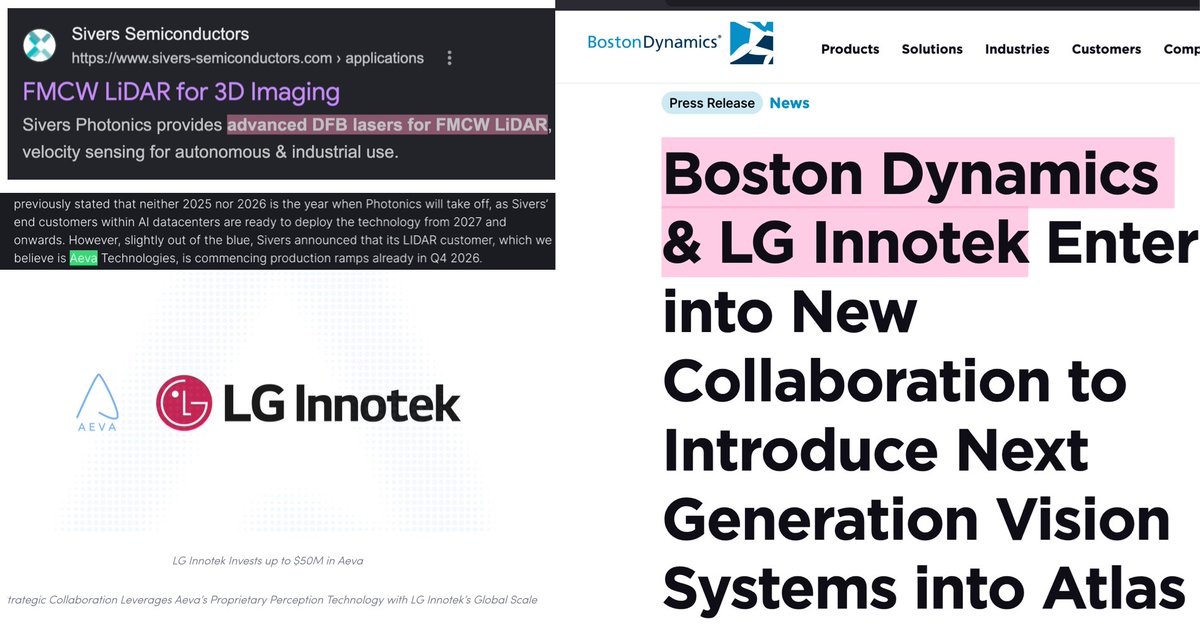

Fun fact: Lot of the same companies are often used across different supply chains.

One likely example is: $SIVE as the upstream laser supplier to Boston Dynamics via:

Sivers -> $AEVA FMCW (CW DFB lasers) -> LG Innotek -> Boston Dynamics.

I actually personally liked Aeva for 4D AI first.

Just so happened to find out Sivers was their high confidence laser supplier for 4D FMCW lidar.

So you actually get robotics exposure with photonics while the same CW lasers used for hyperscaler AI DCs.

Near term revenue ramp though it's probably $SIVE supplying laser volume ramp for $NVDA self-driving car related architectures though Aeva.

Humanoids are probably later in 2028?

You can always get more indirect exposure like MU with memory or $INTC with edge CPUs, but of course there's more direct exposure out there.

Think I've already covered a lot of names in the past like $VPG or Harmonic Drive. But hilariously enough CPO players like $SIVE are a core part of frontier physical AI development.

I think u must be new here.

Many of my ideas get intense backlash at the start, especially the more original they are.

$AXTI - endless hate to the point I got banned from the $RDDT WSB forum.

They thought it was some scam Chinese company, but Reuters, Epiwafer company earnings, and institutions validated their InP substrate position many months later.

$RPI - everyone called it some meme stock.

Literally Bloomberg, Financial Times, and others went out and called it a meme stock with no fundamentals.

Analysts went and said the idea was stupid and said it was going to crash ��as a fact”.

Earnings came out? Blew away any projection with 58% fwd revenue growth.

But they seem to have forgot all the backlash they threw out at me, while they’re citing it as a high growth ai hardware company no.

$SIVE? Everyone called it a “meme stock”. I get bunch of hate from Swedish media all the way up.

Bunch of people didn’t understand the technical nuances, and they keep throwing personal attacks for some strange reason.

But as you know it’s probably my most successful idea and it’s validated so far by institutional buying from Fidelity Research, JP Morgan as well as formally announced partnerships from $JBL to $GFS.

Same hate with:

- $AAOI at $30, when everyone called management a “scam” or “shady”

- $LITE at $300 when everyone called photonics a “bubble”

- $RKLB at $20 when everyone thought it was a low revenue launch company that was a bubble. I actually got temp banned from WSB from posting about Rocketlab since moderators didn’t like the stock.

- $HOOD at $20 when everyone recalled them freezing GME buys/sells

- $IQE at $12 when people thought it was just some random crap $100m company over in the UK with “no actual photonics partnerships”

- $SOI at $44 when European bank analysts thought it was “overvalued”and my thesis wasn’t anything new

- $NBIS at $75 when everyone in the $IREN camp said I was spreading Russian propaganda and that they had no moat

- $INTC at $115 when everyone thought they couldn’t compete with $TSM

- $MRVL at $85 when everyone thought they were losing ASIC share to Broadcom.

- $AEHR at $35 when everyone misread their earnings and thought they had no revenue

- $EWY at $115 when everyone was crying KOSPI was a bubble and LNG/helium/oil would disrupt the memory trade

Can go on and on…

I do read a lot of the comments, which is why I remember a lot of the hate (probably either jealously, impression farming, or lacking the technical depth is my guess).

But I think at this point, people can just see each thesis validated over and over again.

And the success in markets drown out the old noise.

Good thing is markets are the final arbiter of what’s right or wrong, not the angry comments or posts on X.

Just a reminder: 99% of X was bearish on memory 3 months ago...

Since then:

$MU $380 -> $1122 (+195.26%)

$SNDK $565 -> $2155 (+281.42%)

$EWY $132 -> $219 (+65.91%)

SK Hynix 849K -> 2.685M KRW (+215.5%)

Samsung 172K -> 362K KRW (+110.7%)

If you see a bunch of projections on memory names like Samsung becoming the most profitable company in the world in 2028.

Might be a good idea to think independently outside of the narratives at the time like "Oil, LNG, Helium, Iran, etc."

Probably same thing now with optical names and their projections into 2027, 2028.

I do think photonics and memory are the 2 top themes though, with optics being very early into the supercycle.