MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST MUST WATCH

Today, our Board of Directors approved a proposed rule that would establish requirements under the GENIUS Act for FDIC-supervised stablecoin issuers.

https://t.co/VAnMhwyGo5

NEW: Wall street giant Citi bank announces "later this year, Citi will be launching our infrastructure that integrates Bitcoin into tradition finance." 🚀

"Making Bitcoin Bankable"

Bridge has received OCC conditional approval to organize a federally chartered national trust bank. This will enable us to operate stablecoin products and services under direct federal oversight, including:

- Custody

- Orchestration

- Issuance

- Reserves management

Stablecoins are becoming core financial infrastructure. Institutions need regulatory clarity, operational resilience, and scalable systems to build with confidence. A national trust bank establishes that foundation.

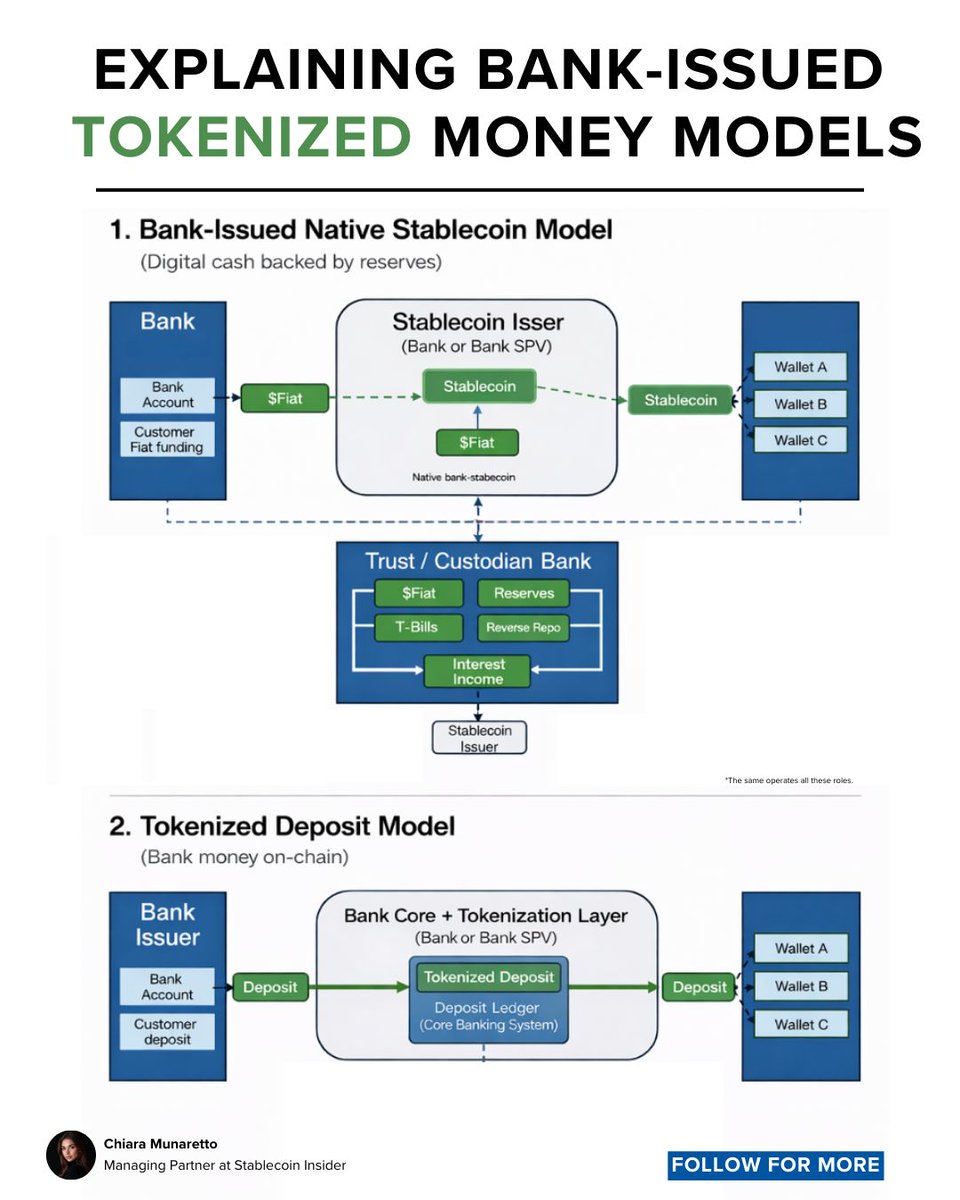

Bank stablecoin vs tokenized deposits not the same thing

They may look identical on-chain, but they live in very different worlds 👇

Bank-issued native stablecoin

- New digital cash instrument

- Backed by segregated reserves (cash, T-bills, RRP)

- Holder has a claim on the reserve pool, not the bank balance sheet

- Designed for portability, settlement, and programmability outside core deposits

Tokenized deposits

- No new money created

- Existing bank deposits, represented on-chain

- Remain on the bank’s balance sheet & core banking system

- Token are technical wrapper for speed and automation

Key point:

- Stablecoins/deposits legally, regulatorily, or monetarily.

- They only create value when moved, not when idle.

- And in both models, a bank can run the full stack end-to-end.

Same rails.

Very different instruments.

🚀 x402 v2 has come to Python!

After launching the TS & Go SDKs last month, we rewrote the x402 Python SDK from the ground up.

It’s still x402 Python v2.0.0, but all the learnings from TS & Go are baked into a fresh SDK experience.

https://t.co/VHcMTGYGsI

Today, NYSE is proud to announce the development of a platform for trading and on-chain settlement of tokenized securities.

NYSE’s new digital platform will enable tokenized trading experiences, including 24/7 operations, instant settlement, orders sized in dollar amounts, and stablecoin-based funding. Its design combines the NYSE’s cutting-edge Pillar matching engine with blockchain-based post-trade systems.

Learn more: https://t.co/gknK3viIyp

Stablecoins for AI agents and why HTTP 402 suddenly matters again.

HTTP 402 was meant to enable native internet payments. It failed because payments were slow, expensive, and human-driven.

That constraint is gone.

- Stablecoin supply: <$2B (2019) to $246B+ (2025)

- Transaction fees: fractions of a cent

- ~90% of stablecoin volume is already programmatic

AI agents can search, negotiate, and decide but traditional payments break automation. Cards, fraud systems, and human checkouts don’t scale to machines.

Stablecoins fix this:

Programmable, policy-driven, machine-native payments.

Now HTTP 402 returns as a payment challenge:

Server sets price. Agent validates policy. Stablecoin settles. Access granted automatically.

The protocol stays open.

The value accrues to payment facilitators.

Stablecoins aren’t just a new rail.

They’re the execution layer for autonomous commerce.

And for the first time, HTTP 402 has a real reason to exist.

This is not a payments strategy.

This is a hedging strategy:

It’s a hedge for an agentic commerce world.

When AI agents decide how money moves, @Visa is positioning itself above every rail: cards, A2A, stablecoins, open banking.

Not owning the spend.

Owning the rules, permissions, and trust layer behind it.

📷 Source: @CBinsights

What stands out to you when you look at this strategy map?