A Possible GST Litigation Storm Coming? 🚨

Circular No. 254/11/2025-GST dated 27th October 2025 clarifies who the “Proper Officer” is for proceedings under Section 122 and Section 74A.

But here’s where things get interesting ⬇️

🔍 Section 122 doesn’t even use the term “Proper Officer”. (Section 127 does)

So… if notices were issued directly under Section 122 without first invoking Sections 73 / 74 / 74A,

👉 Can those notices now be challenged as invalid?

👉 Can the said circular be also challenged as it defines "Proper Officer" under Section 122 instead of Section 127?

And wait… there’s more 🤯

For Section 74A, this circular is the first time the government has clarified the “Proper Officer”.

So what about all the 74A notices already issued earlier?

💭 Were those notices issued without authority?

💭 Could they now be argued as void?

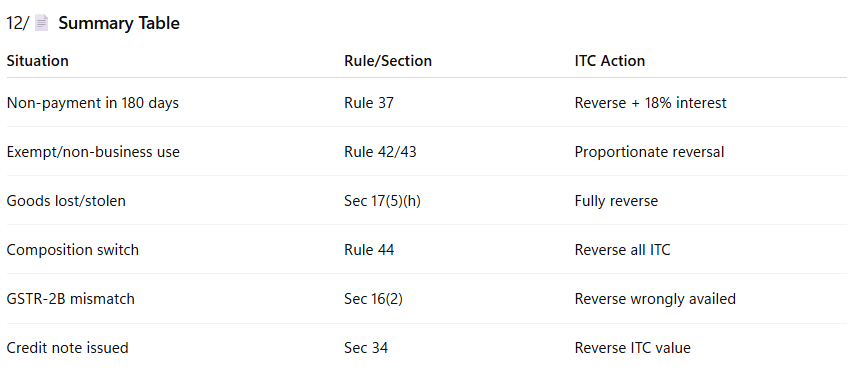

💼 GST ITC Reversal Rules – Explained Simply

Claiming Input Tax Credit (ITC) is easy 💸

But keeping it is tricky — wrong claim = reversal + interest!

Let’s decode when ITC needs to be reversed 🧵👇

1. 📘 What is ITC Reversal?

➡️ITC reversal means reducing or paying back the credit you earlier claimed —

either due to ineligibility, non-payment, or non-usage for taxable supplies.

2. ITC Reversal – Non-Business or Exempt Use (Rule 42 & 43)

➡️If inputs/services are used for both:

✅ taxable & ❌ exempt/non-business supplies —

then proportionate ITC must be reversed.

➡️Example:

If 20% of your turnover is exempt → reverse 20% ITC.

3. Non-Payment to Vendor within 180 Days (Rule 37)

➡️Didn’t pay your supplier within 180 days from invoice date?

🚫 Reverse the ITC + pay interest (18%).

✅ You can re-avail it once payment is made later.

4. Goods Lost, Stolen, or Destroyed (Sec 17(5)(h))

➡️ITC not allowed if goods are:

❌ Lost

❌ Stolen

❌ Destroyed or given as free samples/gifts

If already claimed → must reverse.

5. Change in Use of Capital Goods (Rule 43)

➡️If capital goods used for taxable supply are later used for:

• Exempt supply, or

• Personal purpose

→ Proportionate ITC reversal required based on remaining life (5 years).

6. Credit Notes / Purchase Returns

➡️If supplier issues a credit note or goods are returned,

ITC related to that value must be reversed from your books.

7. Composition Scheme Opt-In

➡️If you switch from regular GST to Composition Scheme,

all unutilized ITC on inputs, capital goods, and stock must be reversed on the date of switch.

8. Supply Becomes Exempt / GST Registration Cancelled

➡️If your outward supplies become exempt or your GST registration is cancelled →

You must reverse proportionate ITC on stock & capital goods held.

9. ITC Mismatch with GSTR-2B

➡️ITC not reflected in GSTR-2B = can’t be claimed.

➡️If wrongly availed → reverse immediately to avoid demand under Sec 73/74.

10. ⚖️ Interest & Penalty

➡️Interest @ 18% applies from the date of wrong availment till reversal.

➡️Voluntary reversal before notice helps avoid penalty under Sec 73(5).

11. 💡 Key Takeaways:

✅ Claim only eligible ITC

✅ Reconcile with GSTR-2B monthly

✅ Pay suppliers within 180 days

✅ Reverse promptly to avoid demand

🧵 Can GST Registration be Cancelled for Filing NIL Returns or Non-Commencement of Business for 6 Months?

Let’s understand the legal provision + case laws 👇

1. Legal Provision — Rule 21(a) of CGST Rules, 2017: -

➡️Registration is liable to be cancelled if the registered person does not conduct any business from the declared place of business or has not commenced business within six months from the date of registration.

⚠️ So, if you obtain GSTIN but continuously file NIL returns (no turnover, no activity) for 6 months — it may be treated as non-commencement of business and invite cancellation.

2. Combined Reading of Rule 21(a) & 21(b): -

➡️Rule 21(a): Non-commencement of business within 6 months

➡️Rule 21(b): Failure to furnish returns for 6 continuous months

👉 Filing NIL returns for 6 months can be seen as both —

🔹 Non-commencement of business, and

🔹 Failure to carry on genuine business activity.

3. Departmental Action

If either condition exists, officer may:

📩 Issue Show Cause Notice (REG-17)

🕒 Allow 7 working days to reply in REG-18

📄 Pass Cancellation Order (REG-19)

During the process, your GSTIN may be suspended — meaning no invoicing or ITC allowed.

4. Key Case Laws 🔍

(a) Suguna Cutpiece Center v. Appellate Deputy Commissioner (ST)

(Madras HC, 2022 – 2022-TIOL-508-HC-MAD-GST)

Held : - that cancellation solely for non-filing of returns or NIL activity, without proper enquiry or opportunity, is invalid.

(b) ARS Steel & Alloy International Pvt. Ltd. v. STO

(Madras HC, 2021 – 2021-VIL-524-MAD)

Held: - Authorities must record reasons and follow Rule 22 procedure before cancelling GSTIN, even if returns are NIL for long.

(c) TVL. R.K. Motors v. STO (ST)

(Madras HC, 2023 – 2023-TIOL-616-HC-MAD-GST)

Held: - Directed restoration of GSTIN cancelled for NIL filings, permitting revocation upon filing pending returns.

5. How to Avoid Cancellation

✅ File all GST returns (even NIL) on time

✅ Ensure some activity (if business is operational)

✅ Respond promptly to SCN

✅ Apply for voluntary cancellation if business not commenced

6. Revocation Option

➡️If cancelled, apply under Section 30 using Form REG-21 within 30 days (extendable).

➡️Revocation is allowed only after all pending returns are filed and dues paid.

7. 📌 Summary:

🔸 Non-commencement of business within 6 months (Rule 21a) or

🔸 Filing NIL returns continuously for 6 months (Rule 21b)

→ both can trigger GST registration cancellation.

Stay compliant, file timely, and respond to notices!

🚨 MSME Reporting in Tax Audit (Form 3CD)

Auditors must check compliance with the MSMED Act, 2006 & report delays in payment to Micro/Small enterprises.

Here are the relevant clauses 👇

1. Clause 22 – Disallowance u/s 43B(h): -

🔹 Any sum payable to MSME beyond time limit u/s 15 of MSMED Act (45 days max) is not deductible.

Auditor must report such unpaid amounts.

✅ Example: Goods ₹10L bought on 1-Apr, credit 45 days. Paid after 90 days.

→ Deduction of ₹10L disallowed in P&L.

2. Clause 26 – Payments to Specified Persons u/s 40A(2)(b): -

If payment to MSME is made to a related party covered u/s 40A(2)(b), auditor must report details separately.

3. Clause 34 – TDS Compliance: -

If payments to MSMEs require TDS (say for services/contract), auditor must report:

✔️ Whether TDS deducted

✔️ If deposited within time

4. Clause 43 – Break-up of MSME Dues

Auditor must disclose:

▶️Principal & interest due to MSMEs

▶️Separately for Micro & Small enterprises

▶️Amounts remaining unpaid beyond the specified period

🔎 Example – MSME Reporting: -

ABC Ltd. purchased goods from XYZ (MSME):

Invoice: ₹10L dated 01-Apr, credit 30 days

Paid: 30-Jul (after 120 days)

➡️ Auditor must:

✔️ Report under Clause 22 (disallowance u/s 43B(h))

✔️ Show dues in Clause 43

✔️ Verify TDS u/s 194C (if applicable) under Clause 34

✅ Key Takeaway

Auditors now have to be extra cautious with MSME disclosures.

📌 Delayed payments → Tax disallowance

📌 Non-reporting → Auditor responsibility

#TaxAudit #TaxAudits

Pani puri wala gets GST notice after receiving Rs 40 lakh in annual payments, internet reacts: 'Time to change career!'

Read More at: https://t.co/Nzu08yddjT!'

📛⚠️ Very Important Judgment on Input Tax Credit (ITC); #MUSTREAD

📢 ITC Claim Can't Be Denied Solely On The Ground That Such Claim Is Not Reflected In GSTR-3B, Where Such Claims Were Referred In GSTR -2A and GSTR-9

➡️ The Madras High Court allowed the petition in the case of SRI SHANMUGA HARDWARES ELECTRICALS, remanding the case back to the assessing officer for re-consideration of the Input Tax Credit (ITC) claims for the assessment years 2017-2018, 2018-2019, and 2019-2020, which were initially denied because they were not reflected in the GSTR-3B returns, despite being claimed in GSTR-2A and GSTR-9 returns.

➡️ The Court held that the assessing officer should not deny an ITC claim solely on the basis that it was not claimed in the GSTR-3B returns, without examining all relevant documents and allowing the registered person to substantiate their claim.

➡️ The petitioner, dealing in electrical products and hardware, contended that nil returns filed in GSTR-3B were erroneous and that they are indeed eligible for ITC, which is reflected in their GSTR-2A and duly claimed in their GSTR-9 annual returns.

➡️ The High Court emphasized the need for the assessing officer to offer a comprehensive examination of the ITC claim by examining all pertinent documents and providing the petitioner a reasonable opportunity to present their case, including a personal hearing.

➡️ The judgment mandates that upon the petitioner placing all documents supporting its ITC claims, the assessing officer must reassess the claim and issue a fresh assessment order based on a thorough evaluation of the presented evidence and relevant guidelines.

✔️ Madras HC - SRI SHANMUGA HARDWARES ELECTRICALS [Writ Petition Nos. 3804, 3808 & 3813 of 2024 and W.M.P.Nos. 4105, 4107, 4110, 4111, 4116 & 4119 of 2024]

#GST #GSTwithBimalJain #a2ztaxcorpllp #GSTUpdate #GSTcaseLaw #GSTR2A #GSTR9 #GSTITC #InputTaxCredit #Credit #GSTCredit #GSTreturn