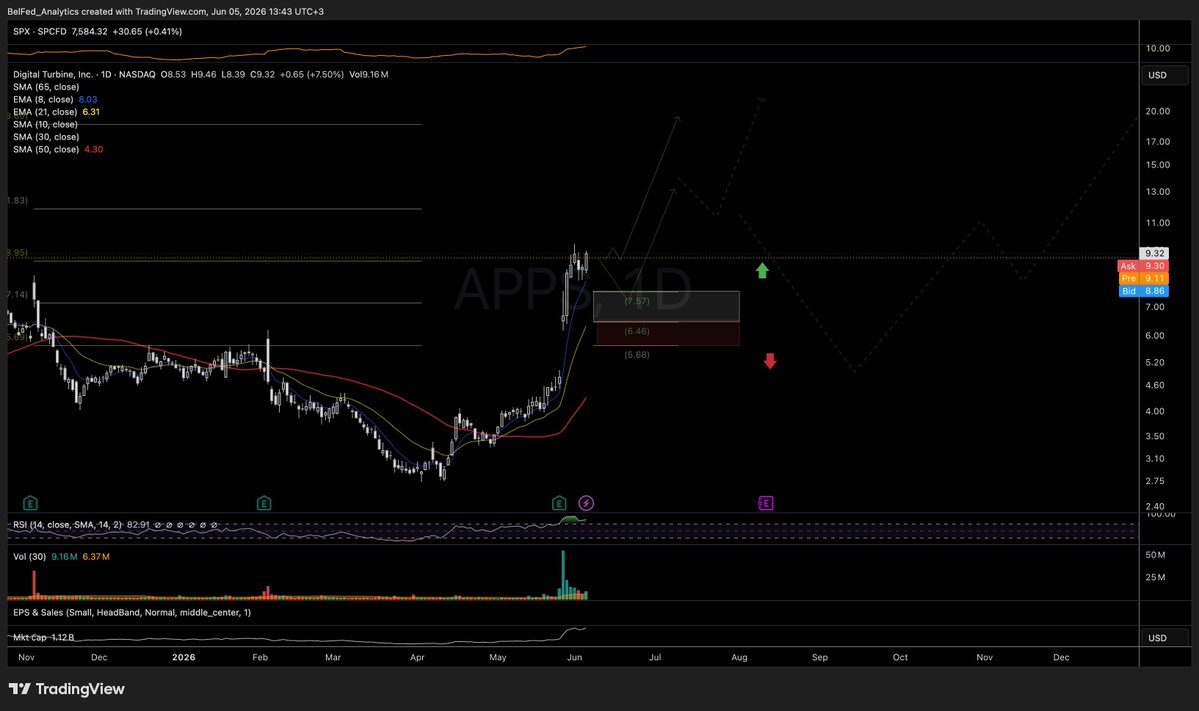

$APPS

2am thoughts. I never sleep fam

We keep going. I love this one long-term. Only a ~$1B market cap.

I shared this on 5/29. DONT MISS

The valuation, P/S ratio, and platform niche still stand out.

Repost. Bookmark. Subscribe. Follow for more ideas.

Digital Turbine ($APPS) is quietly building a unique position in mobile app distribution and monetization.

While everyone focuses on app stores and ad networks, $APPS sits directly between carriers, OEMs, developers, and users.

The company is embedded across 1B+ devices, works with 80K+ apps, and reaches over 1B users monthly.

Recent numbers were strong:

• Q4 revenue $142.5M (+20% YoY)

• App Growth Platform +57% YoY

• Adjusted EBITDA $31.4M (+53% YoY)

• Adjusted EPS $0.16 vs $0.10 last year

• FY2026 revenue $565.3M (+15% YoY)

• FY2026 adjusted EBITDA $122.5M (+69% YoY)

FY2027 guidance:

• Revenue $630M-$650M

• EBITDA $135M-$145M

What stands out is Launchpad, announced June 2.

Launchpad unifies app distribution across on-device placements, storefronts, direct-to-consumer channels, in-app opportunities, and programmatic advertising.

Think about what that means.

As privacy restrictions increase and developers look for alternatives to the traditional app-store funnel, Digital Turbine is positioning itself as a distribution layer.

The company already has carrier and OEM relationships with names like Orange, Telefónica, Verizon, and Motorola while developers including Zynga, Playtika, and King are utilizing the ecosystem.

The AI angle is getting overlooked too.

DT iQ, Ignite Graph, Google Cloud partnerships, and Databricks integrations are helping improve targeting, discovery, and install efficiency across its network.

Valuation is where it gets interesting.

$APPS trades around 2x sales with a market cap near $1.1B.

Compare that to:

$APP trading roughly 28-31x sales.

$ADBE around 4x sales.

No, I’m not saying it deserves those multiples.

But if management executes, margins continue improving, and Launchpad gains adoption, there is room for multiple expansion from current levels.

The market is finally rewarding execution again.

Stock has more than doubled YTD and is trading near 52-week highs around $10.40 after earnings.

Thinking out loud…

A company controlling app discovery and distribution across 1B+ devices at only a ~$1B valuation feels like something institutions eventually revisit if growth continues.

Higher risk? Absolutely.

But this is one of the more interesting underfollowed platform plays I’ve found lately.

$DOCU $NOW $ASAN $U $TTD $MGNI $PUBM $ZETA $ORCL $CRCL $MSFT

Do your own DD.

$APPS

APPS steigt seit dem Tief von 2026 stark an und liegt oberhalb des vorherigen Bereichs. Das kleine 1-2 setup hat sich durchgesetzt, aber der Vormarsch sieht jetzt gedehnt aus und ein Pullback der Welle 4 kann jederzeit beginnen.

Führendes Szenario: Die gekennzeichnete Struktur lässt es immer noch zu, dass es sich bei dem aktuellen Anstieg um Welle 3 handelt, mit einer normalen Welle 4-Korrektur in die orangefarbene Unterstützungszone, bevor ein späterer Welle 5-Versuch erfolgt. Solange der Kurs nicht unter diese Zone fällt, bleibt die Aufwärtsstruktur intakt und die blau markierte Region bleibt relevant, wenn sich die bullische Interpretation weiter entwickelt.

Risiko-Szenario: Ein nachhaltiger Durchbruch unter 5,35 $ würde die Sichtweise der Welle 4 unzuverlässiger machen und die Wahrscheinlichkeit erhöhen, dass es sich bei der Rallye nur um eine korrigierende Erholung handelt. Dies würde den Fokus wieder auf den strukturellen Unterstützungsbereich bei ~2,70 $ und die untere blaue Region lenken. Wichtige Supportlevels: $7,60 / $6,26 / $5,35 / ~$2,70

Wichtige Widerstandsniveaus: $18,72 / $24,15 / $36,79

Fazit: Der bullische Weg bleibt offen, aber der aktuelle Push ist ausgedehnt und muss einen Pullback der Welle 4 verkraften, ohne die Unterstützungszone zu verlieren.

$APPS

2am thoughts. I never sleep fam

We keep going. I love this one long-term. Only a ~$1B market cap.

I shared this on 5/29. DONT MISS

The valuation, P/S ratio, and platform niche still stand out.

Repost. Bookmark. Subscribe. Follow for more ideas.

Digital Turbine ($APPS) is quietly building a unique position in mobile app distribution and monetization.

While everyone focuses on app stores and ad networks, $APPS sits directly between carriers, OEMs, developers, and users.

The company is embedded across 1B+ devices, works with 80K+ apps, and reaches over 1B users monthly.

Recent numbers were strong:

• Q4 revenue $142.5M (+20% YoY)

• App Growth Platform +57% YoY

• Adjusted EBITDA $31.4M (+53% YoY)

• Adjusted EPS $0.16 vs $0.10 last year

• FY2026 revenue $565.3M (+15% YoY)

• FY2026 adjusted EBITDA $122.5M (+69% YoY)

FY2027 guidance:

• Revenue $630M-$650M

• EBITDA $135M-$145M

What stands out is Launchpad, announced June 2.

Launchpad unifies app distribution across on-device placements, storefronts, direct-to-consumer channels, in-app opportunities, and programmatic advertising.

Think about what that means.

As privacy restrictions increase and developers look for alternatives to the traditional app-store funnel, Digital Turbine is positioning itself as a distribution layer.

The company already has carrier and OEM relationships with names like Orange, Telefónica, Verizon, and Motorola while developers including Zynga, Playtika, and King are utilizing the ecosystem.

The AI angle is getting overlooked too.

DT iQ, Ignite Graph, Google Cloud partnerships, and Databricks integrations are helping improve targeting, discovery, and install efficiency across its network.

Valuation is where it gets interesting.

$APPS trades around 2x sales with a market cap near $1.1B.

Compare that to:

$APP trading roughly 28-31x sales.

$ADBE around 4x sales.

No, I’m not saying it deserves those multiples.

But if management executes, margins continue improving, and Launchpad gains adoption, there is room for multiple expansion from current levels.

The market is finally rewarding execution again.

Stock has more than doubled YTD and is trading near 52-week highs around $10.40 after earnings.

Thinking out loud…

A company controlling app discovery and distribution across 1B+ devices at only a ~$1B valuation feels like something institutions eventually revisit if growth continues.

Higher risk? Absolutely.

But this is one of the more interesting underfollowed platform plays I’ve found lately.

$DOCU $NOW $ASAN $U $TTD $MGNI $PUBM $ZETA $ORCL $CRCL $MSFT

Do your own DD.

@Crypto__Goku@TylerZapruder Bah en pratique si… tu en fait bien la promotion en donnant de la visibilité à ce phénomène. C’est ce qui engage une ligne éditoriale d’un point de vue éthique et sociale bref tu ne peux pas t’en dédouaner fait juste assumer

$APPS Can someone explain to me why Unity has a P/S ratio of nearly 7? The very same Unity $U that lost the entire IronSource business to Digital Turbine? That would imply a share price of $37 for DT. Only business performance comparison.

$APPS

This may be one of the cleaner turnaround setups in software

Following years of restructuring, operating leverage is beginning to inflect:

• Revenue beat by 7%

• EPS beat by 88%

• Revenue growth accelerated to 20% YoY

Meanwhile the chart continues to tighten:

• Up ~90% since earnings

• Coiling beneath HTF resistance

• RSI resetting after the initial move

• Showing relative strength on Friday's weakness

I'm watching for a breakout through $9.50 to initiate a swing

$APPS The upside trend structure looks strong and intact as long as price holds above the 7.60–6.50 local support zone.

If a new leg higher has not already started, any pullback into this area could offer an attractive buying opportunity, or price may instead consolidate sideways around current levels.

The ideal resistance targets for the next wave up sit at the 11.80 and 18.50 extension levels.

Je le dis comme ça pour prendre date mais on est encore loin du bottom bear market qu’on a pas encore vraiment commencé:

Le catalyseur principal de ce Bear et du bottom viendra de $MSTR Microstrategy

Le père Saylor va faire trembler la planète crypto et c’est pour bientôt…

Very possible that the dip the last two days was deliberate. $APPS apparently represented themselves quite well at the BAC conference and what was said was well received.

@Dark_Emi_ Dur…☹️

J’imagine ce que ça a du réveiller en toi

Je ne savais pas que tu avais gardé des séquelles reconnues en handicap suite à ta chute.

Même si tu dois relativiser avec le pire qui aurait pu arriver ça doit être marquant.

Bon courage à toi

$APPS One Store appstore - for which Digital Turbine holds the rights to pre-load the app store onto mobile devices in the US, Europe, and LATAM - seeks to offer more than just distribution: Commerce & Payments. They combine that Orange deal with One Store for Europe's DMA act.

@Oddhootcapital $APPS They have an Alternative Appstore which they beta test in US (that's for 1-2 years)

They gonna use Ignite to deploy 3rd party AI agents on phone (already today)

They have Ben John, ex-VP from Microsoft AI, now CTO working on further AI products.

$APPS (L)

The bull case for APPS is definitively strengthening after yesterday's earnings report:

- double beat and guidance raise that exceeded consensus estimates on top and bottom level

- 8 straight quarters of EBITDA margin expansion (Q4 margin up 5% to 22%)

- operating leverage is heating up (FY26 EBITDA up +69% YoY on +15% revenue)

- significant deleveraging progress (debt $409M → $361M) with more expected on the back of strong FCF growth

- strongest AGP growth in 3 years (+57% y/y) driven by a mix of price (+40% y/y) and volume; AGP is now growing 2x the global ad-tech market

- new Orange partnership expected is expected to accelerate commercial momentum, representing more subscribers than Verizon and AT&T combined

Despite a ~40% increase following yesterday's report, $APPS remains cheap, valued at ~8.2x on an EV/FY27 EBITDA basis.

And, while many of its ad-tech peers face a potential existential crisis as LLMs reduce open web traffic, $APPS stands to benefit in this new world as less open web time translates into more time spent in the app environment in which $APPS lives

This is just the beginning...

$APPS Earnings:

- Fiscal fourth quarter of 2026 revenue totaled $142.5 million, representing an increase of 20% year-over-year as compared to the fiscal fourth quarter of 2025.

- GAAP net loss for the fiscal fourth quarter of 2026 was $7.3 million, or ($0.06) per share. Non-GAAP adjusted net income for the fiscal fourth quarter of 2026 was $19.7 million, or $0.16 per share, as compared to non-GAAP adjusted net income of $11.3 million, or $0.10 per share, in the fiscal fourth quarter of 2025.

"Fiscal 2026 was a successful year for Digital Turbine. Emboldened by our upside financial performance and ongoing business momentum, we are pleased to provide guidance above current estimates for fiscal 2027," said Bill Stone, CEO. "I am extremely proud of the Company's overall execution, as we returned the business to double-digit revenue and adjusted EBITDA growth with notable gross margin expansion, while simultaneously strengthening the balance sheet and strategically positioning the Company for the future. One of the key factors for our markedly improved performance has been our ability to more effectively utilize our unique first-party data in order to drive better results for our rapidly expanding global network of advertisers, publishers, carriers and OEMs. Our ability to leverage valuable new AI tools and partnerships to maximize the value of our extensive data array has been, and will continue to be, a meaningful contributor to growth."

https://t.co/Naij3xyAjg

@TCQNVP2@franceinfo Le foot est un prétexte et n’a rien à voir là dedans ce sont des délinquants armés qui ont agit en bande organisée pour semer la terreur dans un État laxiste et rien d’autre