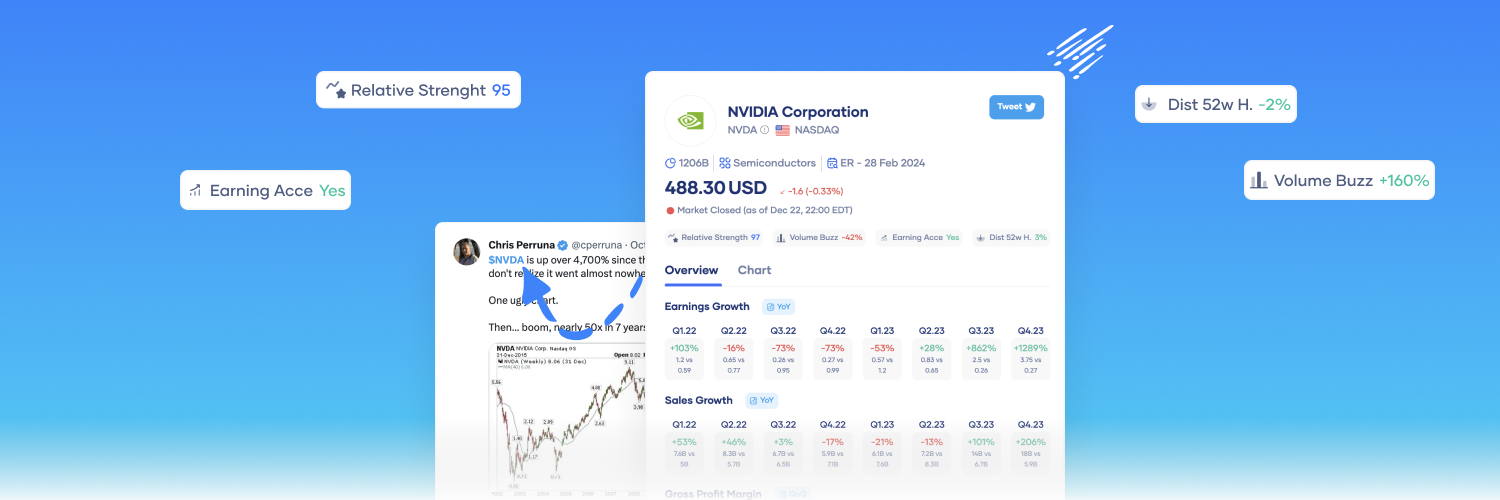

@Tweevest

It's definitely a great tool—if you're looking for the best ideas... they're right here!

And best of all, it's free!

What more could you ask for!

Thanks to @Tweetvest

$HIMS in 2023:

- $870M Revenue

-$74M FCF

-1 Brand in the US

-1.5M Subs

$HIMS in 2026:

-$2.4B Revenue

-$280-300M FCF

-Sells in US, Canada, EU, Australia...

-2.6M subs

-3 brands ($HIMS , ZAVA, Eucalyptus)

- $NVO & $LLY Partner

Price in June 2024 and June 2026: $26

Something is wrong here... 🔥📈

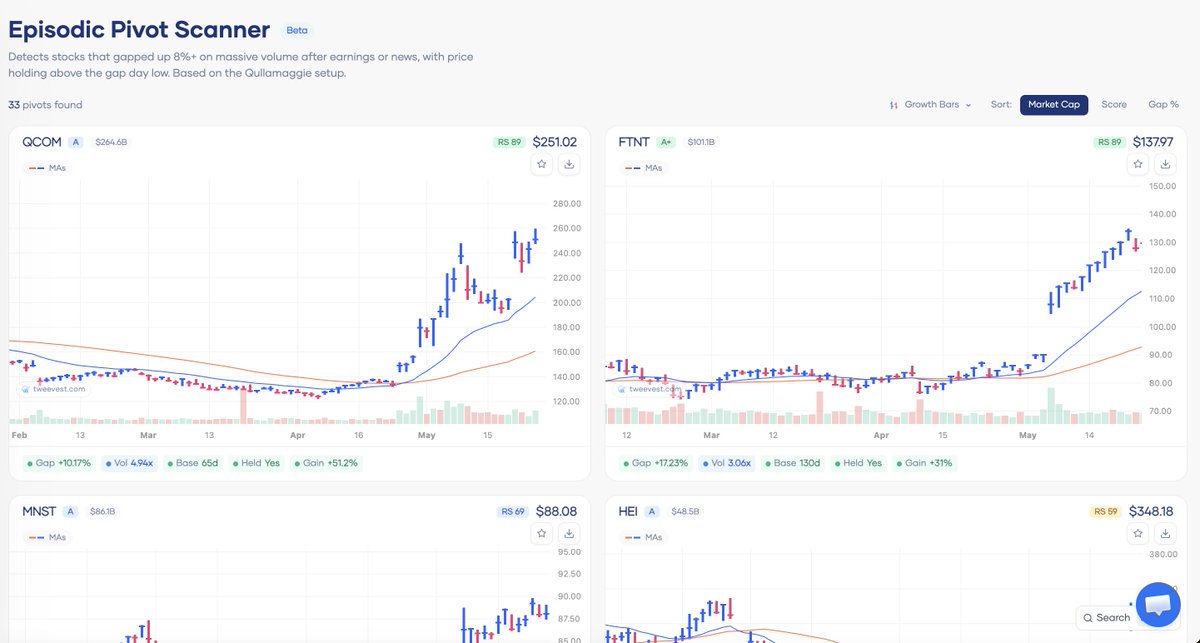

Built for traders who actually run CANSLIM.

→ RS line rankings

→ EPS acceleration filters

→ VCP / episodic pivot / bull flag detection

No paywall. Just edge. https://t.co/lMWBV8SbyE

Everyone is missing the point on $HIMS ⬇️

Borrowing $338.5M for 6 years at 0% cash cost, with dilution only kicking in above ~$50 (thanks to the capped call). Cheap capital if you believe in the story.

Polymarket now prices a SpaceX IPO at 92% probability by June 30. $1.5T+ valuation in play.

When that prints, $RKLB is the only public pure-play left in the room.

The Motley Fool ran a "Rocket Lab vs SpaceX" piece today comparing the two head to head. Tells you where the narrative is heading.

bears had a rough morning.

$HIMS just priced one of the cheapest convertibles I've seen in telehealth this cycle.

$350M. Upsized from $300M. 0.00% coupon.

Due 2032.

Capital flagged for international expansion and AI platform investment.

bears hated last quarter's print. institutions just handed them free money anyway.

who is right?

https://t.co/P2wqJ6GdfS

Everyone's still digesting $IREN's Q3 print.

Meanwhile, the company quietly announced an acquisition of Awaken this morning, a creative and media agency for brand and content strategy.

$3.4B Nvidia partnership one week. M&A the next. CEO sitting next to Dell and Nvidia at Dell Technologies World.

solid.

https://t.co/mTXhCgNnB2

$SOFI is doing the thing where the post-earnings tape is more interesting than the print itself.

Record growth. Tight guidance. Pre-market flat for a third straight session.

Whoever's accumulating down here isn't being loud about it.

When was the last time a public company grew AI Cloud revenue 841% year over year and got called "peak euphoria" by the bears the same week?

$NBIS up 400%+ in twelve months. WSJ now framing it as the CoreWeave killer.

valuation matters. execution matters more right now.

https://t.co/5t8piEoFAX

$HIMS is down 8% because investors saw the convertible note offering and immediately worried about dilution.

But I think this needs a little more context…

$HIMS announced a $300M convertible senior notes offering due 2032, with an option for another 45M.

So max size = 345M.

At roughly a $5.3B market cap, that is around 6–7% of the company’s value.

But this is not the same as them dumping 6–7% new shares into the market tomorrow.

It is debt that can convert later, and part of the proceeds are being used for capped calls, which are meant to reduce dilution risk if the stock moves higher.

The real issue is not the note itself.

The real issue is timing…

$HIMS just had a messy Q1.

Revenue was $608M, up only 4% YoY.

Subscribers grew to nearly 2.6M, up 9% YoY.

Gross margin dropped to 65% from 73% last year.

They reported a $92M net loss vs $49M net income last year.

That is why the market is sensitive right now…

The compounded GLP-1 boom faded, $HIMS pivoted toward branded GLP-1s through the $NVO partnership, and now investors are worried about profitability.

Demand is not the problem.

$HIMS guided 2026 revenue to $2.8B–$3.0B and still reiterated long-term 2030 targets of at least $6.5B in revenue and $1.3B in adjusted EBITDA.

The problem is the market does not want just revenue growth anymore…

It wants proof that the new GLP-1 model can produce strong contribution margins, retention, cross-sell, and operating leverage.

That is why the stock is down.

Not because $300M of capital destroys the company.

It is down because investors are already nervous about margins, and then $HIMS added another dilution/debt headline on top of it.

Personally, I think the move is an overreaction if you believe the 2030 platform thesis.

$HIMS is using capital to fund:

- Eucalyptus acquisition

- International expansion

- AI infrastructure

- Fulfillment infrastructure

- Better cost structure over time

- More financial flexibility

That is exactly what you would expect from a company trying to become the global consumer-facing front door for healthcare.

But now they have to execute.

The next few quarters need to show that the $NVO partnership can turn GLP-1 demand into profitable recurring growth, that international expansion can scale, and that AI/fulfillment investments actually improve margins.

The bear case is: dilution, lower GLP-1 margins and slower growth = multiple compression.

The bull case is: this is a temporary reset year, $HIMS uses the capital to expand globally, branded GLP-1 becomes a lower-risk long-term channel, and the market eventually re-prices the company back toward the 2030 story.

I still think the selloff is more emotional than fundamental…

But $HIMS has to prove it now.

Market check: 70+ US stocks are sitting >7 ATRs above their 50-day SMA.

Shoutout to @jfsrev his work on ATR extension is what got me building this filter into Tweevest in the first place.

Live now → https://t.co/iEwfTca70m