Enjoyed the Bending Spoons ITLB podcast

Valuation is interesting here as bending spoons is best described as a consumer software roll-up. Based on the F-1 they will IPO at ~72x FY’25 EBIT ($277M)

Think investors may have a tough time with the math given legacy SaaS roll-ups (CSU/Roper/etc) with higher retention trade at 15-20x EBIT (albeit with lower inorganic growth)

Am sure Bending Spoons will market on their Adj. EBITDA figure (implies ~32x FY’25) but pro-forma’ing for run rate synergies + adding back transaction expenses / amortization definitely not appropriate imo given M&A is the growth engine here

Worth a listen with Bending Spoons filing to go public today.

We talk about their origins, playbook, talent and everything in between.

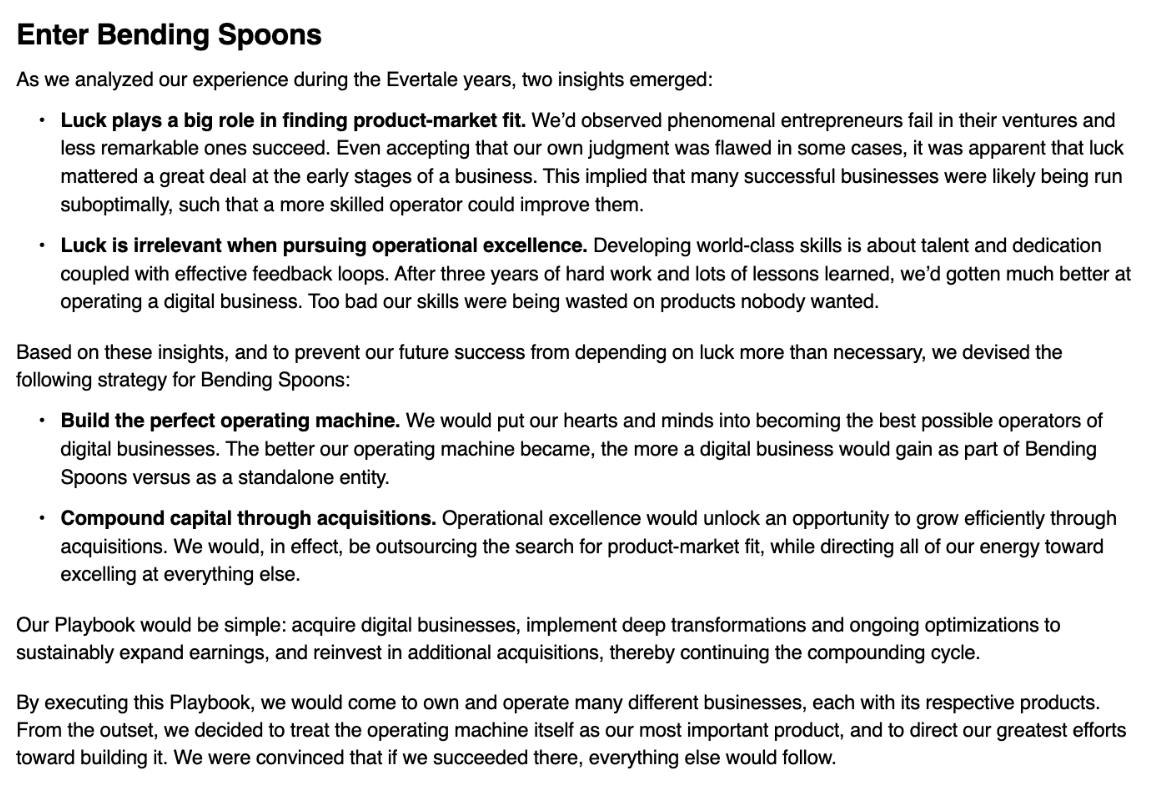

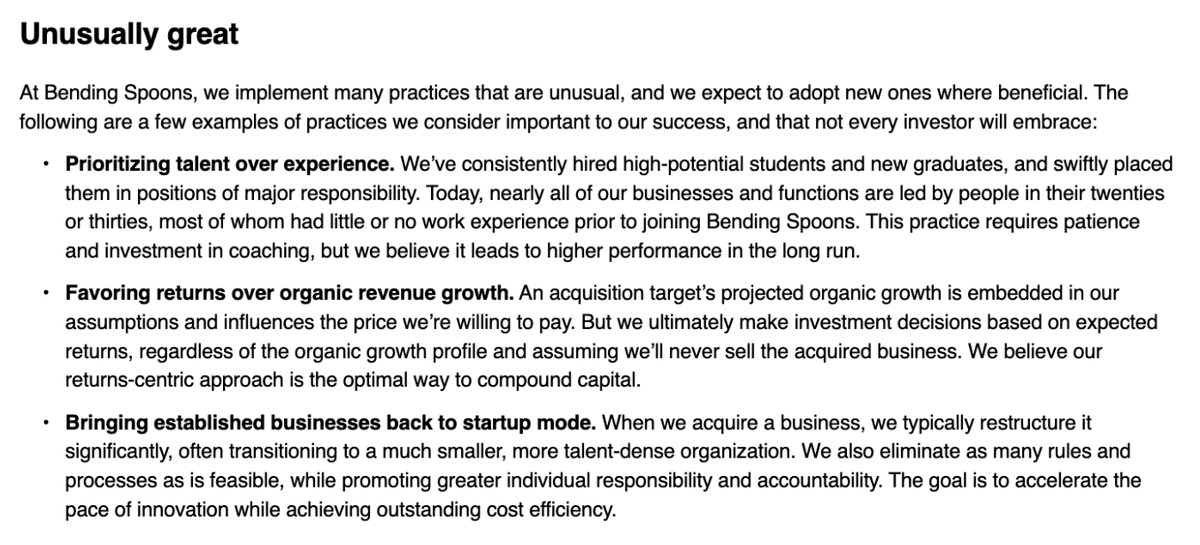

Couple things I liked from their S-1:

- Luck plays a big role in finding PMF

- Luck is irrelevant when pursuing operational excellence

- Talent > experience: "Nearly all of our businesses and functions are led by people in their twenties or thirties, most of whom had little or no work experience prior to joining Bending Spoons."

My sense is most companies only seriously adopted AI tools / began making AI products in Q1 of this year. I think ROI on the efficiency side is easy to justify and can certainly be proved out within 1 year and ROI on AI product will likely take longer and F500s will have FY’26 and FY’27 to prove out.

I think the challenge will always be the quality of talent these PE companies can attract. I’ve asked my technical friends at top tech co’s about this and they do not want to work for a PE firm. They would much rather work at a frontier lab / Cursor / Cognition / [insert other kingmade startup backed by Tier 1 VCs with extreme talent density]

When I try to explain this to partners at my PE firm, they just have a hard time understanding. Like when Cognition is handing out high 6 figs+ to people in their 20s to pursue a much more exciting mission in a much more technically dense environment, it’s hard for PE to get top talent at portcos even if dressed up as AI svcs, etc

Exceptional talk by @skgoodwin23 at Sohn on Private Credit & SaaS

Two points I would add on top of his analysis:

1. On leverage ratios: while most sponsor-owned software companies on EBITDA covenants are “only” levered ~5-6x, this is typically calculated on a “lenderized” version of EBITDA that paints an overly favorable version of earnings power. For example, one of my portfolio companies has lender EBITDA of 7x. Its covenant is 11x. Actual EBITDA (as we look at it as sponsors) is 11.5x.

2. On ARR-based loans: I would be curious to see data on performance of ARR-based vs. EBITDA loans. From where I sit, I actually think our highest performing co’s are levered on ARR and some of our lowest performing are levered on EBITDA, whereas Scott seems to imply ARR-loans are more of an issue.

Quoting Scott Goodwin, the co-founder of Diameter Capital Partners:

“We're going to talk about what the f* is going on in private credit...” (You can hear the whole audience laugh.)

In 18 minutes, Scott gives an in-depth overview of a small piece of the $40 trillion private credit market:

The $2 trillion in leveraged finance/direct lending.

As my friend said about this whole presentation: “Total stud.” And I agree.

Listened to this talk four times now

The M.A.D. Framework, specifically the concept of diffusion, is probably the most powerful articulation I’ve heard of why AI application layer startups not only have a right to exist but a strong right to win

Every year for AI Ascent, @gradypb, @Konstantine and I get to share some perspectives on AI and where things are headed.

This year's talk was about the arrival of agents and the race to deploy them across the application layer, and how founders can compete in this crazy intense market ("Get MAD!" Moats, Affordance, Diffusion).

00:00 Introduction

01:10 AI Wave Calibration

01:56 Three Differences of AI

04:28 Inflection Points to AGI

07:06 Building on Top Strategy

07:29 MAD Moats Framework

09:33 Affordance and Diffusion

12:07 Agents Are Here Now

13:46 Agent Stack and Trajectory

21:12 Future of Work and Meaning

I think the ultimate upside to software vendors is the ability to drive AI cross-sell.

Part of the reason for the Anthropic rev ramp is the fact every sw co is building AI products to sell its customers and those products are being coded with CC and calling the Anthropic API. Anthropic rev ramp probably sustains as a result and we see green shoots in sw pubco P&Ls in 3Q/4Q this year

@SaaSletter@benedictevans This is one of the most thought provoking charts in the deck imo

Potentially very bullish the application layer if low cost models can trail the leading edge by a couple months

@BATMongoose Sub-100% NRR though … seems like they’re bringing him in for sole purpose of selling the business given last 2 businesses he ran were sold. Just now sure how much strategic value buyers will ascribe here…

@HighyieldHarry Banking comp at top EBs is basically on par with MF PE for non-carry holding positions. If you can deal with the grind, its a pretty sure fire path to getting to $1m+ NW by 30

Cognition at $445M ARR seems potentially compelling as a strategic acquisition target to one of the large hyperscalers, given they are the only scaled non foundational model affiliated AI IDE left

My SWE friends think it’s superior at driving end-to-end coding workflows than CC

Cognition at $445M ARR seems potentially compelling as a strategic acquisition target to one of the large hyperscalers, given they are the only scaled non foundational model affiliated AI IDE left

My SWE friends think it’s superior at driving end-to-end coding workflows than CC

Scott Wu is the co-founder of Cognition AI, one of the fastest-growing companies in history. He’s also the greatest competitive programmer the US has ever produced. You may have seen him doing impossible card tricks and mental math.

You’ve never seen him asked about weed, Michael Jordan, cancer, and human consciousness over a punnet of strawberries. That is what Colossus editor-in-chief Jeremy Stern did on a recent visit to San Francisco.

For those less familiar with @ScottWu46: In 2nd grade, he entered a math competition for 7th graders, lost, and was so furious he still fumes about it 20 years later. The next year he entered the 9th-grade division as a 3rd-grader and got a perfect score.

Then he won first place at the US national middle-school math competition and three straight gold medals at the International Olympiad in Informatics, where he became the greatest American gold-medalist and coach in history.

Most of the people running the biggest AI companies met as teenagers, competing for their countries on international math and science teams. OpenAI’s Greg Brockman, Anthropic’s Dario Amodei, Meta’s Alexandr Wang, to name just a few.

Most agree that the von Neumann among them was Scott Wu.

In November 2023, a few weeks after his mother died of lung cancer, on the day Sam Altman was fired from OpenAI, Wu founded his own AI company: Cognition.

He was 26 and saw earlier than almost anyone that AI would converge on agents that work in the background, 24/7, like coworkers. He shipped Cognition’s AI software engineer Devin in March 2024. It worked poorly, and he took intense public criticism for it.

Now, in its first 18 months of service, Devin has generated $445 million of revenue run rate and usage has doubled every eight weeks. The US Army, Goldman Sachs, and Mercedes-Benz are all customers. Cognition is raising at a valuation around $25 billion.

@JeremySternLA sat down with Wu, the emperor of the nerds, to ask the questions we’d all ask one of the smartest people in America—building the most consequential technology of our generation—if we ever got the chance.

As well as MJ and weed, they talk about the cluster of competitive math prodigies behind so much of AI, what makes us human when AGI arrives, and why Wu believes he was put on this earth to teach AI how to code.

Read the piece below.