@zerohedge trade is an exchange of goods,and in international trade,the US dollar acts as the global "standard commodity" becauseit’sthe world’s reserve currency. The US "produces" dollars as a product for global payments,which meansUSAneed a trade deficit to ensure those dollars flow out

Sam Altman admits AI budgets are turning into a “huge issue,” with customers burning more tokens than even OpenAI’s top in-house users.

Altman said OpenAI’s top internal user spends about 100B tokens/month, while one outside customer hit 603B tokens/month.

The cost problem gets worse with AI agents because they do not just answer once, they plan, call tools, read files, retry failed steps, check their own work, and create long chains of hidden token spending. Every plan, retry, code review, context window, tool call, and verification step becomes metered cognition.

A human asks once; an agent may ask hundreds of times in a second.

Companies are no longer asking whether AI is impressive, but whether the marginal token is producing marginal value.

Jevons paradox explains part of the trap: when AI gets cheaper per token, people use far more tokens, so the total bill can still rise.

Brilliant explanation from Nvidia CEO Jensen Huang on AI's job effect:

In software, AI makes coding faster, but that does not mean fewer engineers are needed.

Before AI, we could write 1 billion lines of code; now, with AI, we can aim for 1 trillion.

The 2026 semiconductor shortage is turning into a perfect storm.

Everyone already knows the AI story: massive data center buildout has GPU and HBM capacity locked up tight. No need to repeat that.

What’s less talked about is that mature and lagging-edge nodes are tight now too.

NVIDIA’s Vera Rubin platform has entered full production and is ramping hard for H2 2026 availability. That ramp has pulled significant capacity and focus, while new investments in older nodes were minimal. The result?

Slower growth and real allocation pressure on the mature processes that make power semis, MCUs, analog, and many other essential parts.

On top of that, industrial demand is back. After the 2023 to early 2025 inventory correction and destocking, safety stocks are now largely depleted.

Factory automation is recovering. Lean inventories mean even normal rebound demand quickly turns into extended lead times and tightness.

And agentic AI has added CPUs to the shortage list. The move toward autonomous agents with heavy needs for orchestration, planning, sequential reasoning, and lighter workloads, is shifting data center architectures and driving up CPU demand on top of the GPU-heavy load.

Bottom line: This isn’t just an advanced-node AI crunch anymore. It’s an asymmetric squeeze across the board. AI dominating high-margin capacity while legacy sectors feel the spillover on mature nodes and supporting components. Higher costs and longer lead times are the new normal for 2026.

P&L management is a thankless job. In the downcycle, we are begging customers to input the orders. In the upcycle, we are begging foundry to give us enough wafers.

This week, Google Research published "TurboQuant algorithm" which creates a 6x improvement in memory utilization for AI. $MU stock tanks as a result. The speculation is that memory demand is dead!

This is a comical take! Here's why:

AI Chips and AI Algorithms in the past 5 years have improved 10,000 times! Yes, that 10-thousand, or 4 orders of magnitude.

So did we shut down all the data centers we had 5 years ago because things got 10,000x more efficient? Of course not! In fact, more money will be spent on new data center projects in the next 5 years than ALL OF HISTORY, combined!

Remember DeepSeek, the Chinese open-source algorithm that trained an LLM model for less than 1/10th the cost thought to be possible that came out last year? It showed techniques for 10x more efficiency in AI training algorithms, and quickly all the major AI companies incorporated DeepSeek's methods into their own algorithms...and yet, demand for AI chips didn't decline, it accelerated!

As the cost and efficiency of technology gets better, demand doesn't go down, it actually INCREASES!

This phenomenon is actually super common and widespread to all technologies. In fact, it's known as

Jevons Paradox, named after the economist who first proposed it in 1865! Yes, more than 160 years ago! Poor Jevons didn't even know about Micron. Jevons Paradox occurs when increased technological efficiency reduces the cost of a resource, paradoxically leading to higher overall consumption rather than savings.

So I look at $GOOGL's TurboQuant algorithm and I say AWESOME! Let's find 10x and 100x improvements in efficiency. If we do, it will be insane for Micron!

Micron says its ENTIRE capacity for 2026 is sold-out! It projects to make ~$20 Billion in PROFITS in the next quarter alone. In the next 12 months, Micron will make more profits than its ENTIRE REVENUE last year!

The sell-off of Micron due to [latest dumb reason of "peak cycle" or "TurboQuant makes 6x less demand" etc.] might be one of the dumbest things I have ever seen in the stock market. But what do I know!?

If anyone is still insisting that memory is just a cyclical industry, or that this is simply a memory super cycle, please make sure they read this article. Thank you.

Full article:

https://t.co/cKOJSXl0TT

Elon Musk: "Things will be free in the future. If you've got an AI or robotics economy that is anywhere close to a million times the size of the current Earth economy, literally any need you possibly want can be met."

This year’s @NVIDIAGTC was a powerful showcase of how fast the #AI landscape is evolving — and how central memory and storage are to unlocking what comes next.

A standout moment: @MicronCEO Sanjay Mehrotra and Jensen Huang together at the Micron booth— a powerful reflection of the shared commitment across our ecosystem to accelerate how data becomes intelligence.

As AI continues to transform every industry, collaboration between Micron and @nvidia underscores the importance of pairing breakthrough compute with advanced memory and storage solutions that empower customers to innovate with confidence.

Rumor: Tesla is going to build its own EUV lithography machines because ASML is “too slow.” to supply to the new chip plant.

ASML currently produces <100 EUV machines per year.

Apparently that’s not fast enough for Elon Musk.

The new plan:

• 1,000 EUV machines per week starting 2027

• 10,000 per week by 2028

And since HBM memory is also a bottleneck, Tesla will casually build 10 new memory fabs in the next two years producing 5× the rest of the industry combined.

Meanwhile, Micron Technology, SK Hynix, and Samsung Electronics are panicking.

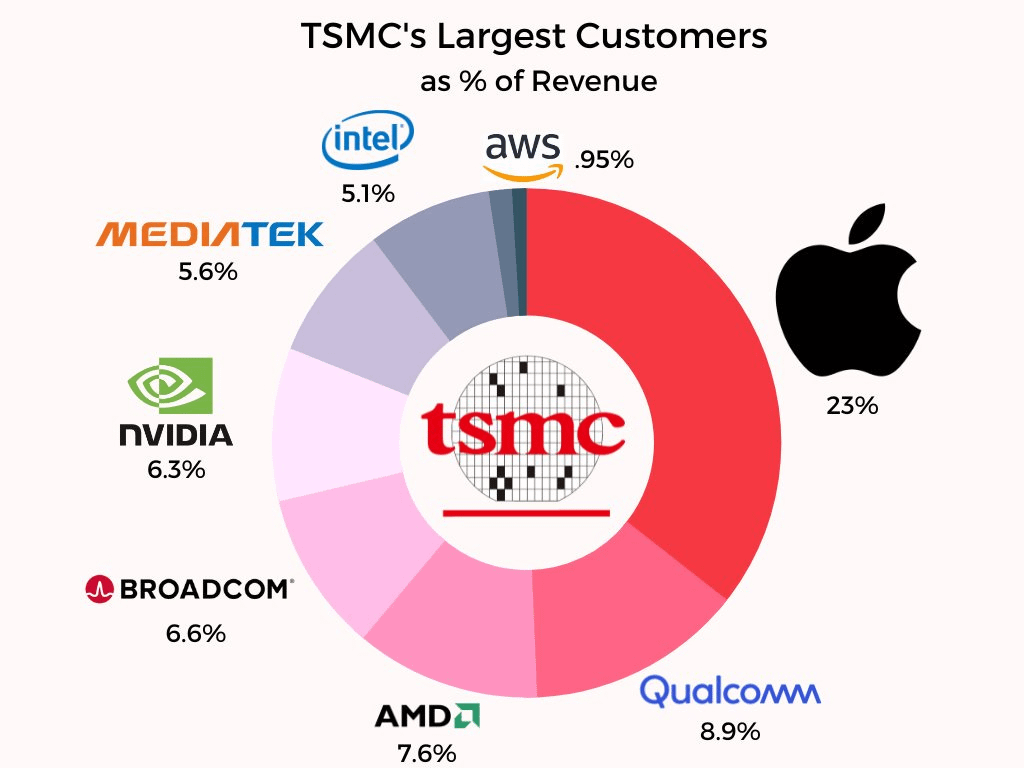

• be Morris Chang

• survive WWII in China, escape to America in 1949

• go to MIT, fail the PhD qualifying exam twice

• decide academia is a trap, join Texas Instruments

• spend 25 years climbing the ranks, building their entire semiconductor division into a global powerhouse

• get passed over for the CEO job because of corporate politics

• 1985: you are 54 years old. Most executives are buying golf clubs and preparing to retire.

• the Taiwanese government begs you to move to a tiny island and build their tech sector from scratch

• you look at the global chip industry and see a massive, glaring inefficiency

• the industry rule at the time: "Real men have fabs" (if you want to design chips, you have to spend billions to build the factory to make them)

• Chang realizes: "What if a factory just prints everyone else's designs, and promises never to compete with them?"

• 1987: founds TSMC (Taiwan Semiconductor Manufacturing Company) at age 56

• invents the "pure-play foundry" model

• traditional hardware giants like Intel and IBM laugh at him for just doing the "dirty work"

• suddenly, a guy named Jensen Huang (NVIDIA) and companies like Apple realize they can design world-class chips without spending $10 Billion on a factory

• TSMC single-handedly births the entire "fabless" technology industry

• scales the physics down to the atomic level, printing circuits smaller than a biological virus

• becomes an absolute, unbreakable monopoly on advanced human technology

• accidentally builds a "Silicon Shield" around Taiwan

• the US and China both realize that if Morris Chang's factories go offline for a single week, the entire global economy (smartphones, fighter jets, AI, car manufacturing) instantly collapses

• steps down, comes out of retirement at age 78 during the 2008 financial crisis to ruthlessly fire the CEO, doubles R&D spending while everyone else is panicking, and permanently crushes Intel

• 94 years old, smokes a pipe, plays competitive bridge, and controls the single most important bottleneck on planet Earth

"We do not compete with our customers. We are everybody's foundry."

NVIDIA's Vera Rubin to Use Only Samsung and SK Hynix HBM4

Samsung Electronics and SK Hynix's sixth-generation High Bandwidth Memory (HBM4) will be incorporated into NVIDIA's next-generation AI accelerator "Vera Rubin," slated for release in the second half of this year. Micron, the world's third-largest memory company, has been excluded from the HBM4 supply chain for Vera Rubin — a result widely interpreted as a recognition of Korean memory makers' technological superiority in key HBM4 performance metrics such as operating speed and bandwidth.

According to industry sources on March 8, Samsung Electronics and SK Hynix have been confirmed as suppliers on NVIDIA's Vera Rubin vendor list. The two companies have been provisionally selected as HBM4 suppliers for the flagship next-gen AI accelerator, whose performance hinges critically on this component. HBM4 is an AI server memory chip manufactured by stacking 8 to 16 layers of advanced DRAM built on 11–13nm process nodes atop a base die, enabling rapid delivery of large volumes of data to the GPU in AI accelerators.

Micron, which currently supplies HBM3E to NVIDIA, has been dropped from the Vera Rubin HBM4 vendor list. The company is expected to supply HBM4 for mid-tier AI accelerators optimized for inference — such as the "Rubin CPX" — rather than for Vera Rubin itself.

The selection of Samsung and SK Hynix as the sole HBM4 suppliers reflects their ability to meet NVIDIA's performance and yield requirements. Samsung has effectively passed NVIDIA's bifurcated HBM4 qualification tests targeting operating speeds of 10Gb/s and 11Gb/s. SK Hynix is in the process of optimizing its product for the 11Gb/s test. Samsung's foundry division has also won an order to produce NVIDIA's GPU "RTX 3060," which the company has decided to resume manufacturing, with production set to begin shortly on an 8nm process.

Only Samsung and SK Hynix at the Heart of NVIDIA's "Monster AI Chip" — Micron Eliminated

Since around 2022, when the AI era began, NVIDIA has been the company that determines the fate of memory semiconductor firms. Those that made it into NVIDIA's HBM supply chain became central players in the AI industry; those that didn't saw their standing diminish. Samsung was a prime example — the two-year crisis narrative that plagued Samsung Semiconductor was triggered by delays in HBM3 supply to NVIDIA and only subsided last September when Samsung passed NVIDIA's HBM3E 12-layer qualification test.

Against this backdrop, the selection of Samsung and SK Hynix — and exclusion of Micron — as Vera Rubin HBM4 suppliers is being assessed as highly significant. It opens the door to large-scale NVIDIA shipments over the next one to two years, securing their HBM dominance.

High-Spec HBM4 Orders

According to industry sources on March 8, Vera Rubin hardware will be unveiled for the first time at NVIDIA's developer conference GTC 2026, scheduled for March 16 in Silicon Valley. While no official launch date has been set, a second-half 2026 release is expected. NVIDIA is putting everything into making Vera Rubin's performance more than five times greater than its predecessor, in order to decisively outpace rivals including AMD and Broadcom. More than 80 partner companies worldwide are aligning with NVIDIA to support the launch of this "monster AI accelerator."

Since last year, NVIDIA has identified HBM4 as the critical component underpinning Vera Rubin's success, pushing memory companies to develop high-performance products. It demanded operating speeds exceeding 10Gb/s — well above the 8Gb/s JEDEC standard — for Vera Rubin's HBM4. Capacity has also been scaled up: Vera Rubin will incorporate 16 HBM4 stacks totaling 576GB, surpassing the 432GB HBM4 capacity in AMD's competing next-gen AI accelerator, the MI450.

Micron Eliminated from Vera Rubin

Global memory companies competed fiercely for Vera Rubin HBM4 supply contracts. Winning over NVIDIA — which commands over 80% share in the AI accelerator market where HBM is heavily integrated — means both technological validation and guaranteed strong earnings.

The race for Vera Rubin HBM4 has narrowed to Samsung and SK Hynix. Micron does not appear on the vendor list. "Micron isn't even being discussed as a Vera Rubin HBM4 supplier," one industry source said.

Between the two, Samsung has recently pulled ahead. Samsung has effectively passed NVIDIA's bifurcated qualification tests for both 10Gb/s and 11Gb/s variants of HBM4, and began shipping finished products to NVIDIA last month, albeit in limited volumes. SK Hynix is continuing product optimization with NVIDIA to pass the 11Gb/s test. Given that the process from HBM4 DRAM wafer input to final packaging takes over six months, both companies are expected to begin full-scale HBM4 production as early as this month.

Micron is not entirely out of the HBM4 picture, however — it is likely to supply HBM4 for mid-tier products in the Rubin series rather than for Vera Rubin itself.

Commodity DRAM Pricing Is a Wild Card

Volume allocations and pricing for Vera Rubin HBM4 have yet to be finalized. Some industry observers suggest that while SK Hynix will retain more than half of NVIDIA's total HBM shipments — including HBM3E — this year, Samsung may emerge as the largest supplier when it comes to Vera Rubin HBM4 specifically. Samsung recently expressed strong confidence, stating that its HBM revenue this year will be triple that of last year.

A key variable is commodity DRAM pricing, which has been roughly doubling quarter-over-quarter. The per-Gb price of server DRAM modules such as SOCAMM2 has reportedly risen to approximately $1.30 — approaching the level of HBM3E, the flagship HBM product. From Samsung's perspective, producing commodity DRAM — which does not require the additional expensive stacking processes that HBM4 demands — may be more profitable.

Jensen Huang's meeting with SK Hynix engineers in Silicon Valley to encourage HBM4 development is also being interpreted as a move to check Samsung's growing negotiating leverage. "Samsung holds HBM4, commodity DRAM, and other products, giving it a diverse set of negotiating cards it can play with NVIDIA," one industry observer noted.

$MU

Not a good news 👀🤔

Neuroscientist study reveals that Gen Z has become the 1st generation to be less intelligent than its predecessor, the Millennials.

For the first time in 100 years, young people are scoring lower than their parents on IQ tests and core skills like memory, reading, and focus. This is happening mainly in the US and Europe.

The main cause appears to be excessive screen time and digital device use, particularly in schools and social settings.

While some suggest Gen Z is just developing different skills, research shows actual declines in fundamental problem-solving abilities.

"Around 2010, laptops, tablets, and educational software became widespread in classrooms. These tools were marketed as solutions for personalized learning and efficiency. Instead, evidence increasingly suggests they may undermine deep cognitive processing. Screen-based learning fragments attention, encourages rapid task-switching, and reduces the need for memory consolidation.

Studies show that students who spend several hours per day using computers for learning often score substantially lower on standardized tests than peers with limited screen exposure. Outside school, smartphones and social media compound the problem. "

What a Cognitive Decline Could Mean

"If these trends persist, the consequences could extend far beyond test scores. Lower average cognitive ability may affect innovation, economic productivity, scientific problem-solving, and democratic decision-making. Complex global challenges from climate change to public health require sustained reasoning and deep understanding."

---

rathbiotaclan. com/is-gen-z-the-first-generation-less-intelligent-than-their-parents/

Huge contrarion view from Groq Founder, Jonathan Ross.

Insted of job losses, we will see labor shortages in the AI era.

AI won’t steal jobs, it’ll make everything cheaper. And when life costs less, people work less, retire earlier, and opt out of the grind.

---

"I believe that AI is going to cause massive labor shortages. I don’t think we’re going to have enough people to fill all the jobs that are going to be created. There are three things that are going to happen because of AI.

The first is massive deflationary pressure. This cup of coffee is going to cost less. Your housing is going to cost less. Everything is going to cost less, which means people are going to need less money.

So, how is it going to cost less to have a cup of coffee because of AI? You’re going to have robots farming coffee more efficiently. You’re going to have better supply chain management. It’s going to improve across the entire supply chain. You’re also going to be able to genetically engineer coffee so that you get more of it per watt of sunlight. This applies across the entire spectrum.

So, you’re going to have massive deflationary pressure. That’s number one. What that means is people will need to work less.

That leads to number two, which is that people are going to opt out of the economy more. They’re going to work fewer hours, fewer days a week, and fewer years overall. They’re going to retire earlier."

---

From "20VC with Harry Stebbings" YT Channel

This is coming a lot quicker than people think.

In a landmark move for humanoid robotics, Boston Dynamics’ Atlas robot has graduated from viral demos to real-world industrial work at a Hyundai factory in Savannah, Georgia.

The 5’9”, 56 degrees of freedom, and 200-pound machine is now performing tasks on an active auto assembly line.

A dramatic evolution in its speed, agility, and practical application. Also with Gemini Robotics from Google DeepMind, Atlas can understand its surroundings and adapt in real time. It works alongside humans, coordinates with Spot and Stretch, and connects straight into factory control systems.

It runs for 4 hours, swaps batteries without help, and works across a wide temperature range.

Hyundai plans to ramp production hard, targeting 30,000 units a year by 2028. This feels like the early stages of something much bigger.

Micron’s $MU "Crucial" Divorce: Why Suffering From Success Makes This Peak a Floor

By Hataf Capital

Investors often suffer from a psychological block when a stock hits an all-time high: the "nosebleed" fear. It is a natural instinct to assume that after a triple-digit rally, the easy money has been made and the risk-reward has tilted toward the gravity-bound. But in the case of Micron Technology $MU, looking at the price chart in isolation is a trap. If you look under the hood of the current "AI super cycle," you’ll find that Micron isn't just riding a wave; it is fundamentally re-engineering its business to shed the low-margin baggage of the past and become a pure-play infrastructure giant.

I last covered Micron in October, arguing that the demand destruction of previous years was a ghost of the past. Since then, the stock has surged to nearly $290, fueled by an FQ1 ‘26 performance that didn’t just beat expectations it shattered them. With record revenue of $13.6 billion and a staggering EPS of $4.78, Micron is proving that it is the ultimate beneficiary of an industry-wide supply crunch. When you look at the 2026 guidance projecting revenue of $18.7 billion and EPS of $8.42 for the next quarter alone you realize we aren't looking at a peak; we are looking at a structural re-rating of what this company is worth.

The Strategic Purge: Why Killing "Crucial" is a Masterstroke

The most telling signal of Micron’s confidence isn't found in a spreadsheet, but in its recent decision to shut down the "Crucial" consumer brand by February 2026. For nearly 30 years, Crucial was the face of Micron for everyday PC builders and gamers. To the casual observer, exiting a market you’ve led for three decades looks like a retreat. In reality, it is a ruthless, high-conviction pivot toward where the real money is: the AI data center.

Consumer DRAM and SSDs are notoriously cyclical, low-margin, and price-sensitive. By liquidating this segment, Micron is freeing up its most valuable asset manufacturing capacity to serve hyperscalers like Google $GOOG, Amazon $AMZN, and Microsoft $MSFT. These giants are currently in an "open-ended order" phase, essentially telling Micron they will take every bit of HBM3E and HBM4 the company can produce, regardless of the price. When your customers stop asking "How much?" and start asking "How many can you ship?", you don't waste silicon on $80 consumer RAM sticks. You pivot to the 66% gross margin world of the Cloud Memory Business Unit.

The Stargate Effect and the Physics of Scarcity

To understand why Micron has such immense pricing power right now, you have to look at the sheer scale of the infrastructure being built. OpenAI’s "Stargate" project, a $500 billion initiative, is rumored to require so much memory that it could consume nearly 40% of the entire world’s DRAM production. This creates a rising tide that lifts all boats, but Micron’s boat is leaner and faster.

The industry is currently facing a supply-driven shortage that makes the 2022 glut look like a distant memory. Contract prices for DDR5 have jumped nearly 300% in just three months. This isn't just "good timing"; it’s a physical constraint of the technology. High-bandwidth memory (HBM) is significantly harder to manufacture than standard DRAM, requiring more wafer starts for fewer finished chips. As Micron and its peers (Samsung and SK Hynix) divert more production to HBM to satisfy the hunger of Nvidia’s Blackwell and Rubin architectures, the supply for everything else shrinks. This "HBM tax" on the rest of the market ensures that pricing power remains firmly in Micron’s hands through at least 2027.

Breaking the "Cyclical" Label: The Math of a Super Cycle

The bear case for Micron has always been its cyclicality the idea that what goes up must come down. But the current trajectory suggests the "trough" of the next cycle will likely be higher than the "peak" of the last one. Micron is guiding for an annualized H1 ‘26 EPS of over $26.00. At the current stock price of roughly $276, that puts the forward P/E at an absurdly low 10.5x.

Compare that to its peers. Nvidia $NVDA trades at 40x, and even laggards in the space are commanding higher multiples. The market is still pricing Micron like a commodity memory maker when its financial profile is starting to look more like a high-growth software-infrastructure play. With free cash flow hitting a record $3.9 billion in a single quarter even after aggressive capex spending of $4.5 billion the company is effectively self-funding its expansion. This is no longer a company begging for a recovery; it is a cash-flow machine that is "suffering" only from the fact that it cannot build factories fast enough to meet demand.

Final Thoughts: The Valuation Gap is the Opportunity

We are witnessing a fundamental shift in the global economy where memory is no longer a peripheral component but the "heart" of the AI revolution. Micron’s market share in the global DRAM space has climbed to over 25%, and its technological lead in HBM4 power efficiency positions it as the preferred partner for next-gen AI accelerators.

While the triple-digit gains might make some investors hesitate, the underlying earnings power of the company has grown even faster than the stock price. If Micron were to trade at a modest 18x P/E still a discount to the broader semiconductor sector we would be looking at a stock price well north of $600 based on FY28 estimates. The reality is that Micron is still "cheap" because the market hasn't fully digested the death of the old cycle and the birth of the new secular super-trend. I am reiterating a strong Buy; this is one of those rare moments where the "all-time high" is actually a bargain.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]

Micron’s Q1 Earnings: Why the "Christmas Rally" Is Just the Beginning of a Structural Re-Rating

By Hataf Capital

Micron Technology $MU has already delivered a masterclass in shareholder returns this year, leaving many of its semiconductor peers in the dust. With the stock sitting on a massive year-to-date rally, the skepticism is natural: is the tank empty? The short answer is no. In fact, the market is arguably still in the early innings of pricing Micron correctly. We are witnessing a fundamental identity shift from a cyclical commodity player to a critical pillar of AI infrastructure.

If you are looking at Micron through the lens of historical memory cycles, you are likely missing the forest for the trees. The upcoming Q1 2026 earnings print isn't just another quarterly update; it is the catalyst that could confirm Micron’s transition into a structurally higher-margin business. The odds of a Christmas rally extending well into 2026 are substantial, and the data suggests the "easy money" hasn't actually been made yet.

The Death of the "Boom/Bust" Commodity Cycle?

To understand the bullish case, we have to dissect the revenue mix, because that is where the story has changed. In the fourth quarter, data center revenues accounted for 56% of Micron’s consolidated volume, delivering gross margins of approximately 52%. For context, Micron’s historical gross profit norm hovers between 30% and 40%. This is not a fluctuation; it is a step-change.

When over half your volume is coming from the highest-value workloads in the global economy AI and high-performance computing the old playbook of "sell the boom, buy the bust" becomes obsolete. We are seeing a prolonged period of margin superiority that suggests the volatility of the past is being smoothed out by insatiable data center demand. This shift to a higher value stack means the current margin boost is likely "sticky," justifying a valuation premium the market has been hesitant to award.

The Physics of Shortage: How HBM Changes Everything

The real magic in this thesis lies in the mechanics of High Bandwidth Memory (HBM). Micron’s HBM revenue has surged to an annualized run rate of roughly $8 billion, driven by HBM3E ramps. But the secondary effect of this ramp is what investors should be watching.

Producing HBM is incredibly resource-intensive. It soaks up a disproportionate number of wafer starts and devours advanced packaging capacity. Every wafer allocated to HBM is a wafer not producing conventional DRAM. This creates a supply vacuum in the legacy market. As HBM scales, the supply of standard DRAM tightens physically, forcing buyers of non-HBM memory to compete for shrinking availability.

This dynamic hands Micron tremendous pricing power across its entire portfolio. We are seeing "buyer capitulation" a scenario where customers stop optimizing for the lowest price and start panic-buying to secure supply. This behavior sustains higher Average Selling Prices (ASPs) far longer than typical market models predict. When you combine this with the rising memory requirements for AI-enhanced PCs, smartphones, and autonomous driving systems, you have a perfect storm of supply constraints meeting secular demand growth.

Why The Q1 Print Will Likely Beat Consensus

Heading into the Q1 report, the setup is asymmetric. Management has guided for approximately $12.5 billion in revenue with gross margins north of 51% and EPS around $3.75. The market consensus is currently pinned at the upper end of this guidance. Usually, high expectations are a setup for disappointment, but the revisions over the last month have been surprisingly muted.

Given the accelerating pricing environment and the mix shift toward data center products, Micron has multiple levers to pull. Even if unit volumes remain flat, the ASP uplift from that tighter supply-demand balance can drive a beat. If they exceed the top-end EPS guidance by a mere few cents driven perhaps by better-than-expected yield or pricing power it validates the "higher-for-longer" thesis. The bar is high, but the fundamental momentum suggests Micron can clear it.

Valuation: The Case for a Multiple Re-Rating

Here is where the math gets compelling. If we accept that this margin expansion is structural rather than cyclical, Micron is trading at a discount that borders on irrational. The stock currently trades at an implied FY2027 P/E ratio of under 11x. For a company that is essentially the fuel tank for the AI engine, that is bargain-basement pricing.

It is unreasonable to expect Micron to trade at the same multiples as Broadcom $AVGO or $AMD, given the inherent cyclicality that remains in memory. However, the gap is currently too wide. With AVGO and AMD trading at forward P/Es of roughly 26x and 32x respectively, a 15x multiple for Micron is a conservative, defensible target.

Applying a 15x multiple to FY2027 earnings estimates yields a price target of roughly $331 per share. That represents an upside of over 34% from current levels. This isn't speculative exuberance; it's a reversion to a fair value that accounts for the company's improved earnings quality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]

July 22, 2025

Micron Launches Space-Qualified Portfolio to Power Mission-Critical Data for Aerospace Innovation

https://t.co/VF3OA25VPR

https://t.co/eOfch7lYi7

$MU + SpaceX ?

![hataf_capital's tweet photo. Micron’s Q1 Earnings: Why the "Christmas Rally" Is Just the Beginning of a Structural Re-Rating

By Hataf Capital

Micron Technology $MU has already delivered a masterclass in shareholder returns this year, leaving many of its semiconductor peers in the dust. With the stock sitting on a massive year-to-date rally, the skepticism is natural: is the tank empty? The short answer is no. In fact, the market is arguably still in the early innings of pricing Micron correctly. We are witnessing a fundamental identity shift from a cyclical commodity player to a critical pillar of AI infrastructure.

If you are looking at Micron through the lens of historical memory cycles, you are likely missing the forest for the trees. The upcoming Q1 2026 earnings print isn't just another quarterly update; it is the catalyst that could confirm Micron’s transition into a structurally higher-margin business. The odds of a Christmas rally extending well into 2026 are substantial, and the data suggests the "easy money" hasn't actually been made yet.

The Death of the "Boom/Bust" Commodity Cycle?

To understand the bullish case, we have to dissect the revenue mix, because that is where the story has changed. In the fourth quarter, data center revenues accounted for 56% of Micron’s consolidated volume, delivering gross margins of approximately 52%. For context, Micron’s historical gross profit norm hovers between 30% and 40%. This is not a fluctuation; it is a step-change.

When over half your volume is coming from the highest-value workloads in the global economy AI and high-performance computing the old playbook of "sell the boom, buy the bust" becomes obsolete. We are seeing a prolonged period of margin superiority that suggests the volatility of the past is being smoothed out by insatiable data center demand. This shift to a higher value stack means the current margin boost is likely "sticky," justifying a valuation premium the market has been hesitant to award.

The Physics of Shortage: How HBM Changes Everything

The real magic in this thesis lies in the mechanics of High Bandwidth Memory (HBM). Micron’s HBM revenue has surged to an annualized run rate of roughly $8 billion, driven by HBM3E ramps. But the secondary effect of this ramp is what investors should be watching.

Producing HBM is incredibly resource-intensive. It soaks up a disproportionate number of wafer starts and devours advanced packaging capacity. Every wafer allocated to HBM is a wafer not producing conventional DRAM. This creates a supply vacuum in the legacy market. As HBM scales, the supply of standard DRAM tightens physically, forcing buyers of non-HBM memory to compete for shrinking availability.

This dynamic hands Micron tremendous pricing power across its entire portfolio. We are seeing "buyer capitulation" a scenario where customers stop optimizing for the lowest price and start panic-buying to secure supply. This behavior sustains higher Average Selling Prices (ASPs) far longer than typical market models predict. When you combine this with the rising memory requirements for AI-enhanced PCs, smartphones, and autonomous driving systems, you have a perfect storm of supply constraints meeting secular demand growth.

Why The Q1 Print Will Likely Beat Consensus

Heading into the Q1 report, the setup is asymmetric. Management has guided for approximately $12.5 billion in revenue with gross margins north of 51% and EPS around $3.75. The market consensus is currently pinned at the upper end of this guidance. Usually, high expectations are a setup for disappointment, but the revisions over the last month have been surprisingly muted.

Given the accelerating pricing environment and the mix shift toward data center products, Micron has multiple levers to pull. Even if unit volumes remain flat, the ASP uplift from that tighter supply-demand balance can drive a beat. If they exceed the top-end EPS guidance by a mere few cents driven perhaps by better-than-expected yield or pricing power it validates the "higher-for-longer" thesis. The bar is high, but the fundamental momentum suggests Micron can clear it.

Valuation: The Case for a Multiple Re-Rating

Here is where the math gets compelling. If we accept that this margin expansion is structural rather than cyclical, Micron is trading at a discount that borders on irrational. The stock currently trades at an implied FY2027 P/E ratio of under 11x. For a company that is essentially the fuel tank for the AI engine, that is bargain-basement pricing.

It is unreasonable to expect Micron to trade at the same multiples as Broadcom $AVGO or $AMD, given the inherent cyclicality that remains in memory. However, the gap is currently too wide. With AVGO and AMD trading at forward P/Es of roughly 26x and 32x respectively, a 15x multiple for Micron is a conservative, defensible target.

Applying a 15x multiple to FY2027 earnings estimates yields a price target of roughly $331 per share. That represents an upside of over 34% from current levels. This isn't speculative exuberance; it's a reversion to a fair value that accounts for the company's improved earnings quality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G8S43wFa4AAoldc.png)

![hataf_capital's tweet photo. Micron’s Q1 Earnings: Why the "Christmas Rally" Is Just the Beginning of a Structural Re-Rating

By Hataf Capital

Micron Technology $MU has already delivered a masterclass in shareholder returns this year, leaving many of its semiconductor peers in the dust. With the stock sitting on a massive year-to-date rally, the skepticism is natural: is the tank empty? The short answer is no. In fact, the market is arguably still in the early innings of pricing Micron correctly. We are witnessing a fundamental identity shift from a cyclical commodity player to a critical pillar of AI infrastructure.

If you are looking at Micron through the lens of historical memory cycles, you are likely missing the forest for the trees. The upcoming Q1 2026 earnings print isn't just another quarterly update; it is the catalyst that could confirm Micron’s transition into a structurally higher-margin business. The odds of a Christmas rally extending well into 2026 are substantial, and the data suggests the "easy money" hasn't actually been made yet.

The Death of the "Boom/Bust" Commodity Cycle?

To understand the bullish case, we have to dissect the revenue mix, because that is where the story has changed. In the fourth quarter, data center revenues accounted for 56% of Micron’s consolidated volume, delivering gross margins of approximately 52%. For context, Micron’s historical gross profit norm hovers between 30% and 40%. This is not a fluctuation; it is a step-change.

When over half your volume is coming from the highest-value workloads in the global economy AI and high-performance computing the old playbook of "sell the boom, buy the bust" becomes obsolete. We are seeing a prolonged period of margin superiority that suggests the volatility of the past is being smoothed out by insatiable data center demand. This shift to a higher value stack means the current margin boost is likely "sticky," justifying a valuation premium the market has been hesitant to award.

The Physics of Shortage: How HBM Changes Everything

The real magic in this thesis lies in the mechanics of High Bandwidth Memory (HBM). Micron’s HBM revenue has surged to an annualized run rate of roughly $8 billion, driven by HBM3E ramps. But the secondary effect of this ramp is what investors should be watching.

Producing HBM is incredibly resource-intensive. It soaks up a disproportionate number of wafer starts and devours advanced packaging capacity. Every wafer allocated to HBM is a wafer not producing conventional DRAM. This creates a supply vacuum in the legacy market. As HBM scales, the supply of standard DRAM tightens physically, forcing buyers of non-HBM memory to compete for shrinking availability.

This dynamic hands Micron tremendous pricing power across its entire portfolio. We are seeing "buyer capitulation" a scenario where customers stop optimizing for the lowest price and start panic-buying to secure supply. This behavior sustains higher Average Selling Prices (ASPs) far longer than typical market models predict. When you combine this with the rising memory requirements for AI-enhanced PCs, smartphones, and autonomous driving systems, you have a perfect storm of supply constraints meeting secular demand growth.

Why The Q1 Print Will Likely Beat Consensus

Heading into the Q1 report, the setup is asymmetric. Management has guided for approximately $12.5 billion in revenue with gross margins north of 51% and EPS around $3.75. The market consensus is currently pinned at the upper end of this guidance. Usually, high expectations are a setup for disappointment, but the revisions over the last month have been surprisingly muted.

Given the accelerating pricing environment and the mix shift toward data center products, Micron has multiple levers to pull. Even if unit volumes remain flat, the ASP uplift from that tighter supply-demand balance can drive a beat. If they exceed the top-end EPS guidance by a mere few cents driven perhaps by better-than-expected yield or pricing power it validates the "higher-for-longer" thesis. The bar is high, but the fundamental momentum suggests Micron can clear it.

Valuation: The Case for a Multiple Re-Rating

Here is where the math gets compelling. If we accept that this margin expansion is structural rather than cyclical, Micron is trading at a discount that borders on irrational. The stock currently trades at an implied FY2027 P/E ratio of under 11x. For a company that is essentially the fuel tank for the AI engine, that is bargain-basement pricing.

It is unreasonable to expect Micron to trade at the same multiples as Broadcom $AVGO or $AMD, given the inherent cyclicality that remains in memory. However, the gap is currently too wide. With AVGO and AMD trading at forward P/Es of roughly 26x and 32x respectively, a 15x multiple for Micron is a conservative, defensible target.

Applying a 15x multiple to FY2027 earnings estimates yields a price target of roughly $331 per share. That represents an upside of over 34% from current levels. This isn't speculative exuberance; it's a reversion to a fair value that accounts for the company's improved earnings quality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G8S4u6lbYAAV6zm.jpg)

![hataf_capital's tweet photo. Micron’s Q1 Earnings: Why the "Christmas Rally" Is Just the Beginning of a Structural Re-Rating

By Hataf Capital

Micron Technology $MU has already delivered a masterclass in shareholder returns this year, leaving many of its semiconductor peers in the dust. With the stock sitting on a massive year-to-date rally, the skepticism is natural: is the tank empty? The short answer is no. In fact, the market is arguably still in the early innings of pricing Micron correctly. We are witnessing a fundamental identity shift from a cyclical commodity player to a critical pillar of AI infrastructure.

If you are looking at Micron through the lens of historical memory cycles, you are likely missing the forest for the trees. The upcoming Q1 2026 earnings print isn't just another quarterly update; it is the catalyst that could confirm Micron’s transition into a structurally higher-margin business. The odds of a Christmas rally extending well into 2026 are substantial, and the data suggests the "easy money" hasn't actually been made yet.

The Death of the "Boom/Bust" Commodity Cycle?

To understand the bullish case, we have to dissect the revenue mix, because that is where the story has changed. In the fourth quarter, data center revenues accounted for 56% of Micron’s consolidated volume, delivering gross margins of approximately 52%. For context, Micron’s historical gross profit norm hovers between 30% and 40%. This is not a fluctuation; it is a step-change.

When over half your volume is coming from the highest-value workloads in the global economy AI and high-performance computing the old playbook of "sell the boom, buy the bust" becomes obsolete. We are seeing a prolonged period of margin superiority that suggests the volatility of the past is being smoothed out by insatiable data center demand. This shift to a higher value stack means the current margin boost is likely "sticky," justifying a valuation premium the market has been hesitant to award.

The Physics of Shortage: How HBM Changes Everything

The real magic in this thesis lies in the mechanics of High Bandwidth Memory (HBM). Micron’s HBM revenue has surged to an annualized run rate of roughly $8 billion, driven by HBM3E ramps. But the secondary effect of this ramp is what investors should be watching.

Producing HBM is incredibly resource-intensive. It soaks up a disproportionate number of wafer starts and devours advanced packaging capacity. Every wafer allocated to HBM is a wafer not producing conventional DRAM. This creates a supply vacuum in the legacy market. As HBM scales, the supply of standard DRAM tightens physically, forcing buyers of non-HBM memory to compete for shrinking availability.

This dynamic hands Micron tremendous pricing power across its entire portfolio. We are seeing "buyer capitulation" a scenario where customers stop optimizing for the lowest price and start panic-buying to secure supply. This behavior sustains higher Average Selling Prices (ASPs) far longer than typical market models predict. When you combine this with the rising memory requirements for AI-enhanced PCs, smartphones, and autonomous driving systems, you have a perfect storm of supply constraints meeting secular demand growth.

Why The Q1 Print Will Likely Beat Consensus

Heading into the Q1 report, the setup is asymmetric. Management has guided for approximately $12.5 billion in revenue with gross margins north of 51% and EPS around $3.75. The market consensus is currently pinned at the upper end of this guidance. Usually, high expectations are a setup for disappointment, but the revisions over the last month have been surprisingly muted.

Given the accelerating pricing environment and the mix shift toward data center products, Micron has multiple levers to pull. Even if unit volumes remain flat, the ASP uplift from that tighter supply-demand balance can drive a beat. If they exceed the top-end EPS guidance by a mere few cents driven perhaps by better-than-expected yield or pricing power it validates the "higher-for-longer" thesis. The bar is high, but the fundamental momentum suggests Micron can clear it.

Valuation: The Case for a Multiple Re-Rating

Here is where the math gets compelling. If we accept that this margin expansion is structural rather than cyclical, Micron is trading at a discount that borders on irrational. The stock currently trades at an implied FY2027 P/E ratio of under 11x. For a company that is essentially the fuel tank for the AI engine, that is bargain-basement pricing.

It is unreasonable to expect Micron to trade at the same multiples as Broadcom $AVGO or $AMD, given the inherent cyclicality that remains in memory. However, the gap is currently too wide. With AVGO and AMD trading at forward P/Es of roughly 26x and 32x respectively, a 15x multiple for Micron is a conservative, defensible target.

Applying a 15x multiple to FY2027 earnings estimates yields a price target of roughly $331 per share. That represents an upside of over 34% from current levels. This isn't speculative exuberance; it's a reversion to a fair value that accounts for the company's improved earnings quality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G8S4oapbgAA82Lj.jpg)

![hamids's tweet photo. This week, Google Research published "TurboQuant algorithm" which creates a 6x improvement in memory utilization for AI. $MU stock tanks as a result. The speculation is that memory demand is dead!

This is a comical take! Here's why:

AI Chips and AI Algorithms in the past 5 years have improved 10,000 times! Yes, that 10-thousand, or 4 orders of magnitude.

So did we shut down all the data centers we had 5 years ago because things got 10,000x more efficient? Of course not! In fact, more money will be spent on new data center projects in the next 5 years than ALL OF HISTORY, combined!

Remember DeepSeek, the Chinese open-source algorithm that trained an LLM model for less than 1/10th the cost thought to be possible that came out last year? It showed techniques for 10x more efficiency in AI training algorithms, and quickly all the major AI companies incorporated DeepSeek's methods into their own algorithms...and yet, demand for AI chips didn't decline, it accelerated!

As the cost and efficiency of technology gets better, demand doesn't go down, it actually INCREASES!

This phenomenon is actually super common and widespread to all technologies. In fact, it's known as

Jevons Paradox, named after the economist who first proposed it in 1865! Yes, more than 160 years ago! Poor Jevons didn't even know about Micron. Jevons Paradox occurs when increased technological efficiency reduces the cost of a resource, paradoxically leading to higher overall consumption rather than savings.

So I look at $GOOGL's TurboQuant algorithm and I say AWESOME! Let's find 10x and 100x improvements in efficiency. If we do, it will be insane for Micron!

Micron says its ENTIRE capacity for 2026 is sold-out! It projects to make ~$20 Billion in PROFITS in the next quarter alone. In the next 12 months, Micron will make more profits than its ENTIRE REVENUE last year!

The sell-off of Micron due to [latest dumb reason of "peak cycle" or "TurboQuant makes 6x less demand" etc.] might be one of the dumbest things I have ever seen in the stock market. But what do I know!?](https://pbs.twimg.com/media/HEgxRjraMAAp7L9.jpg)

![hataf_capital's tweet photo. Micron’s $MU "Crucial" Divorce: Why Suffering From Success Makes This Peak a Floor

By Hataf Capital

Investors often suffer from a psychological block when a stock hits an all-time high: the "nosebleed" fear. It is a natural instinct to assume that after a triple-digit rally, the easy money has been made and the risk-reward has tilted toward the gravity-bound. But in the case of Micron Technology $MU, looking at the price chart in isolation is a trap. If you look under the hood of the current "AI super cycle," you’ll find that Micron isn't just riding a wave; it is fundamentally re-engineering its business to shed the low-margin baggage of the past and become a pure-play infrastructure giant.

I last covered Micron in October, arguing that the demand destruction of previous years was a ghost of the past. Since then, the stock has surged to nearly $290, fueled by an FQ1 ‘26 performance that didn’t just beat expectations it shattered them. With record revenue of $13.6 billion and a staggering EPS of $4.78, Micron is proving that it is the ultimate beneficiary of an industry-wide supply crunch. When you look at the 2026 guidance projecting revenue of $18.7 billion and EPS of $8.42 for the next quarter alone you realize we aren't looking at a peak; we are looking at a structural re-rating of what this company is worth.

The Strategic Purge: Why Killing "Crucial" is a Masterstroke

The most telling signal of Micron’s confidence isn't found in a spreadsheet, but in its recent decision to shut down the "Crucial" consumer brand by February 2026. For nearly 30 years, Crucial was the face of Micron for everyday PC builders and gamers. To the casual observer, exiting a market you’ve led for three decades looks like a retreat. In reality, it is a ruthless, high-conviction pivot toward where the real money is: the AI data center.

Consumer DRAM and SSDs are notoriously cyclical, low-margin, and price-sensitive. By liquidating this segment, Micron is freeing up its most valuable asset manufacturing capacity to serve hyperscalers like Google $GOOG, Amazon $AMZN, and Microsoft $MSFT. These giants are currently in an "open-ended order" phase, essentially telling Micron they will take every bit of HBM3E and HBM4 the company can produce, regardless of the price. When your customers stop asking "How much?" and start asking "How many can you ship?", you don't waste silicon on $80 consumer RAM sticks. You pivot to the 66% gross margin world of the Cloud Memory Business Unit.

The Stargate Effect and the Physics of Scarcity

To understand why Micron has such immense pricing power right now, you have to look at the sheer scale of the infrastructure being built. OpenAI’s "Stargate" project, a $500 billion initiative, is rumored to require so much memory that it could consume nearly 40% of the entire world’s DRAM production. This creates a rising tide that lifts all boats, but Micron’s boat is leaner and faster.

The industry is currently facing a supply-driven shortage that makes the 2022 glut look like a distant memory. Contract prices for DDR5 have jumped nearly 300% in just three months. This isn't just "good timing"; it’s a physical constraint of the technology. High-bandwidth memory (HBM) is significantly harder to manufacture than standard DRAM, requiring more wafer starts for fewer finished chips. As Micron and its peers (Samsung and SK Hynix) divert more production to HBM to satisfy the hunger of Nvidia’s Blackwell and Rubin architectures, the supply for everything else shrinks. This "HBM tax" on the rest of the market ensures that pricing power remains firmly in Micron’s hands through at least 2027.

Breaking the "Cyclical" Label: The Math of a Super Cycle

The bear case for Micron has always been its cyclicality the idea that what goes up must come down. But the current trajectory suggests the "trough" of the next cycle will likely be higher than the "peak" of the last one. Micron is guiding for an annualized H1 ‘26 EPS of over $26.00. At the current stock price of roughly $276, that puts the forward P/E at an absurdly low 10.5x.

Compare that to its peers. Nvidia $NVDA trades at 40x, and even laggards in the space are commanding higher multiples. The market is still pricing Micron like a commodity memory maker when its financial profile is starting to look more like a high-growth software-infrastructure play. With free cash flow hitting a record $3.9 billion in a single quarter even after aggressive capex spending of $4.5 billion the company is effectively self-funding its expansion. This is no longer a company begging for a recovery; it is a cash-flow machine that is "suffering" only from the fact that it cannot build factories fast enough to meet demand.

Final Thoughts: The Valuation Gap is the Opportunity

We are witnessing a fundamental shift in the global economy where memory is no longer a peripheral component but the "heart" of the AI revolution. Micron’s market share in the global DRAM space has climbed to over 25%, and its technological lead in HBM4 power efficiency positions it as the preferred partner for next-gen AI accelerators.

While the triple-digit gains might make some investors hesitate, the underlying earnings power of the company has grown even faster than the stock price. If Micron were to trade at a modest 18x P/E still a discount to the broader semiconductor sector we would be looking at a stock price well north of $600 based on FY28 estimates. The reality is that Micron is still "cheap" because the market hasn't fully digested the death of the old cycle and the birth of the new secular super-trend. I am reiterating a strong Buy; this is one of those rare moments where the "all-time high" is actually a bargain.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G9a77VebEAAOhKo.jpg)

![hataf_capital's tweet photo. Micron’s Q1 Earnings: Why the "Christmas Rally" Is Just the Beginning of a Structural Re-Rating

By Hataf Capital

Micron Technology $MU has already delivered a masterclass in shareholder returns this year, leaving many of its semiconductor peers in the dust. With the stock sitting on a massive year-to-date rally, the skepticism is natural: is the tank empty? The short answer is no. In fact, the market is arguably still in the early innings of pricing Micron correctly. We are witnessing a fundamental identity shift from a cyclical commodity player to a critical pillar of AI infrastructure.

If you are looking at Micron through the lens of historical memory cycles, you are likely missing the forest for the trees. The upcoming Q1 2026 earnings print isn't just another quarterly update; it is the catalyst that could confirm Micron’s transition into a structurally higher-margin business. The odds of a Christmas rally extending well into 2026 are substantial, and the data suggests the "easy money" hasn't actually been made yet.

The Death of the "Boom/Bust" Commodity Cycle?

To understand the bullish case, we have to dissect the revenue mix, because that is where the story has changed. In the fourth quarter, data center revenues accounted for 56% of Micron’s consolidated volume, delivering gross margins of approximately 52%. For context, Micron’s historical gross profit norm hovers between 30% and 40%. This is not a fluctuation; it is a step-change.

When over half your volume is coming from the highest-value workloads in the global economy AI and high-performance computing the old playbook of "sell the boom, buy the bust" becomes obsolete. We are seeing a prolonged period of margin superiority that suggests the volatility of the past is being smoothed out by insatiable data center demand. This shift to a higher value stack means the current margin boost is likely "sticky," justifying a valuation premium the market has been hesitant to award.

The Physics of Shortage: How HBM Changes Everything

The real magic in this thesis lies in the mechanics of High Bandwidth Memory (HBM). Micron’s HBM revenue has surged to an annualized run rate of roughly $8 billion, driven by HBM3E ramps. But the secondary effect of this ramp is what investors should be watching.

Producing HBM is incredibly resource-intensive. It soaks up a disproportionate number of wafer starts and devours advanced packaging capacity. Every wafer allocated to HBM is a wafer not producing conventional DRAM. This creates a supply vacuum in the legacy market. As HBM scales, the supply of standard DRAM tightens physically, forcing buyers of non-HBM memory to compete for shrinking availability.

This dynamic hands Micron tremendous pricing power across its entire portfolio. We are seeing "buyer capitulation" a scenario where customers stop optimizing for the lowest price and start panic-buying to secure supply. This behavior sustains higher Average Selling Prices (ASPs) far longer than typical market models predict. When you combine this with the rising memory requirements for AI-enhanced PCs, smartphones, and autonomous driving systems, you have a perfect storm of supply constraints meeting secular demand growth.

Why The Q1 Print Will Likely Beat Consensus

Heading into the Q1 report, the setup is asymmetric. Management has guided for approximately $12.5 billion in revenue with gross margins north of 51% and EPS around $3.75. The market consensus is currently pinned at the upper end of this guidance. Usually, high expectations are a setup for disappointment, but the revisions over the last month have been surprisingly muted.

Given the accelerating pricing environment and the mix shift toward data center products, Micron has multiple levers to pull. Even if unit volumes remain flat, the ASP uplift from that tighter supply-demand balance can drive a beat. If they exceed the top-end EPS guidance by a mere few cents driven perhaps by better-than-expected yield or pricing power it validates the "higher-for-longer" thesis. The bar is high, but the fundamental momentum suggests Micron can clear it.

Valuation: The Case for a Multiple Re-Rating

Here is where the math gets compelling. If we accept that this margin expansion is structural rather than cyclical, Micron is trading at a discount that borders on irrational. The stock currently trades at an implied FY2027 P/E ratio of under 11x. For a company that is essentially the fuel tank for the AI engine, that is bargain-basement pricing.

It is unreasonable to expect Micron to trade at the same multiples as Broadcom $AVGO or $AMD, given the inherent cyclicality that remains in memory. However, the gap is currently too wide. With AVGO and AMD trading at forward P/Es of roughly 26x and 32x respectively, a 15x multiple for Micron is a conservative, defensible target.

Applying a 15x multiple to FY2027 earnings estimates yields a price target of roughly $331 per share. That represents an upside of over 34% from current levels. This isn't speculative exuberance; it's a reversion to a fair value that accounts for the company's improved earnings quality.

[Guys! Please Make Sure To Like And Repost If You Like Our Content]](https://pbs.twimg.com/media/G8S49oTb0AE319c.jpg)