Today is 3 June, but the beneficiary has still not received the returned funds. We are repeatedly being sent the same SWIFT copy without any clear update, while emails and calls remain unanswered.

A fund manager’s job is to beat or at least match the benchmark while staying within the fund’s mandate.

A financial adviser’s job is to help clients set goals, allocate assets sensibly, manage risk, optimise taxes, pick suitable products, and manage their behaviour.

That’s the essence.

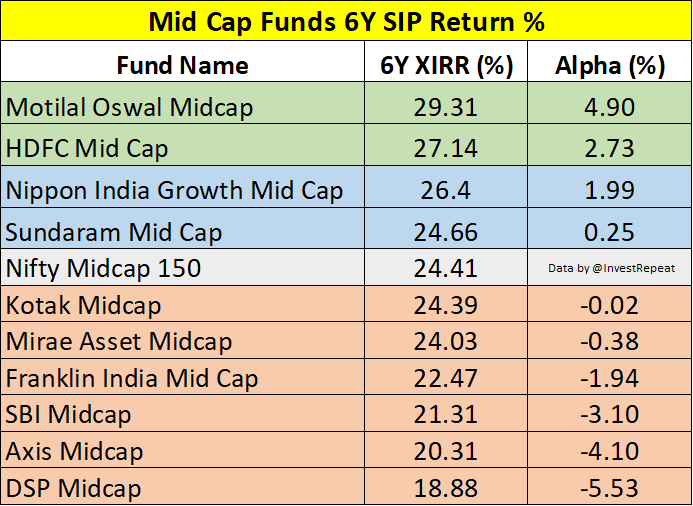

Among the top 10 AUM Mid Cap Mutual Funds

⚡️ 70% funds failed to generate even 1% alpha over Nifty Midcap 150.

⚡️ 80% funds failed to generate 2% alpha over the index.

Thread: The Evolution of Simplicity 🧵

Why Nifty 500 Index fund, instead of mix of sliced and diced, Nifty 50, Next 50, Mid Cap 150, Small Cap 250, etc.?

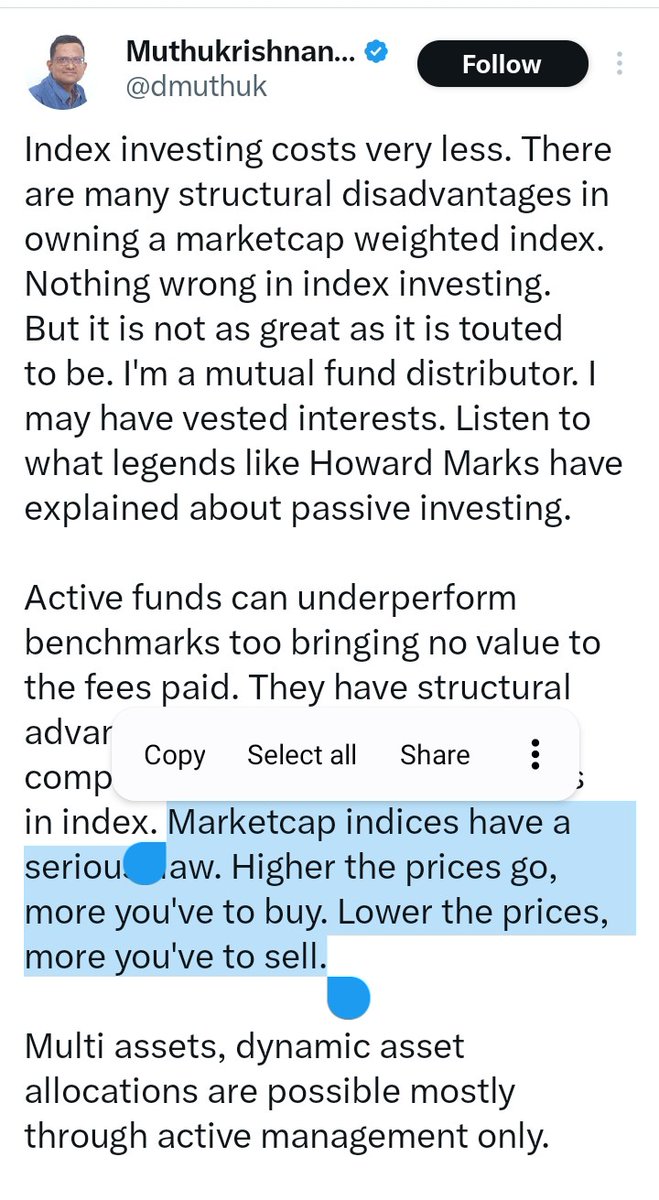

"Marketcap indices have a serious flaw. Higher the prices go, more you've to buy. Lower the prices, more you've to sell." Says Muthuji.

NO.

A market-cap weighted index fund does not sell a stock just because its price falls, nor does it buy more just because a stock’s price rises.

The weights change automatically with price movement.

Rebalancing only happens when the index committee changes the constituents or their free-float data changes.

I have said this before and I will reiterate:

Muthuji is the most overrated personal finance expert in India.

He doesn’t have deep insights into anything, all his knowledge is superficial.

The basic premise of index investing explained:

All investors in the secondary market, taken together, hold 100% of the free-float market capitalization of all listed companies.

This means their collective portfolio is market-cap weighted.

Each stock’s weight in the combined portfolio of all investors is exactly proportional to its free-float market cap relative to the total.

If you isolate any segment of the market (Nifty 50, Next 50, Nifty 500 etc.), the same logic holds:

the aggregate portfolio of all investors in that segment has the same weights as the market-cap weighted index of that segment.

Therefore, the return of a market-cap weighted index is simply the weighted-average return of all investors in that market segment.

Before expenses and taxes, half the money in any segment must underperform that weighted average.

But once you include the costs and taxes of active management, the balance tilts:

more than half of all money must underperform the market-cap index after costs and taxes.

As skilled investors and professional fund managers come to dominate the market, their collective portfolios start to look more and more like the market-cap portfolio.

They become the market.

So even before costs, half of professionally managed assets must underperform the index.

After costs, more than half inevitably underperform.

As markets become more efficient, alpha shrinks and tends to cluster around the cost of active management, further increasing the proportion of assets that lag the index.

This is the basic premise of index investing.

The arithmetic guarantees that a few fund managers will outperform, some through skill, many through luck; but there is no reliable way to identify them in advance, especially for the exact period an investor stays invested.

Why? Because fund managers are human beings. Human behaviour is inconsistent. And when behaviour is inconsistent, future performance becomes unpredictable.

By definition “actively managed fund” means you leave it on the fund manager to invest your money.

So technically if they invest in Lenskart or any IPO shouldn’t offend you. That’s exactly what investors signed up for.

But then calling for SEBI action on them isn’t wise.

People who don’t like fund managers to invest in IPO at all - then broad market index funds are already there.

You have the full power & freedom to decide the product. Choose wisely & as per your comfort.

Multi asset funds (MAFs) solve 2 problems - asset allocation (AA) & tax. Multi-asset + passive cuts expenses & tax. Some say you must tailor AA to customer profile - my reply in below thread.

Have a view/question? Join our mutual funds group on WhatsApp https://t.co/sOIJNGj90g

Congratulations @naveenthacker sir on being named a #Goalkeepers2025 Champion by @gatesfoundation in NYC.

Sir has dedicated his life to polio eradication, immunization, vaccine advocacy & child health — a true inspiration globally! 🙏

As of August 2025, you are having around 620 Index Funds (including equity, debt, commodity and others). AMCs already created clutter. But don’t make your portfolio cluttered.

For them, its PAAPI PETH KA SAWAAL.

Just because fund tagged with Index doesn't mean worth to invest.

IMD દ્વારા જારી કરેલ સ્ટેટ ફોરકાસ્ટ અનુસાર આવતી કાલે તા.૦૭/૦૯/૨૦૨૫, રવિવારના રોજ કચ્છ જિલ્લામાં રેડ એલર્ટ (અતિભારે વરસાદની શક્યતા) હોઈ, સાવચેતી દાખવવા કચ્છ જિલ્લા વહીવટીતંત્ર દ્વારા જાહેર જનતાને અનુરોધ કરવામાં આવે છે.

@CMOGuj@revenuegujarat@SEOC_Gujarat

Fintechs offering direct mutual funds are just a customer acquisition tool.

The real business? Making you trade stocks, F&O, and cross-sell products.

You’re not the customer. You’re the opportunity.

If it’s free, you’re the product.

These fintech apps pretend to “empower investors” with direct mutual funds.

But the same apps push you into stocks and F&O.

First they preach “wealth creation”, then turn you into a thrill-seeking trader.

House always wins — and it’s not you.

After 20+ years of being in the markets, one thing has become crystal clear to me: most investors should just invest in low-cost equity, debt, and gold index funds and do something useful with their lives. 😬 Trying to pick the "best fund" or "best asset class" is largely a waste of time and energy.

What most investors don't realize is that they'd get far better returns by focusing on maximizing their earning potential rather than obsessing over picking the "best stocks and funds." The odds are stacked against them anyway.

That's exactly why we launched the @ZerodhaAMC Multi Asset Fund. This single fund gives investors exposure to large-cap and mid-cap equities, government bonds, and gold all in one place. Investors don't have to worry about rebalancing, tax complications, or managing multiple investments.

There was a famous study from Fidelity that found that their best-performing accounts belonged to people who were either dead or had forgotten they had accounts. The study was made up, but the point still stands.

Category 1: Index investing does not work in India. May be for large caps.

Category 2: Most funds cannot beat the index. Look at the data for large caps or even for midcaps (given below)

Handa Uncle: Stop chasing alpha. Chase peace of mind. Buy the index.