Tech sector TTM P/E just hit 47.3x. That's the 100th percentile of the past decade!

What's wild isn't the absolute number. It's that we got here in seven weeks. From ~32 in early April to ~47 now.

A 47% multiple expansion with zero change in earnings.

The Iran panic isn't just over. It's been completely unwound, and then some.

100th percentile doesn't mean the top is in. But it does mean the margin for error is paper thin from here.

Anything that disappoints lands on multiples that have nowhere left to expand.

More at: https://t.co/3AReXT2QU9

Renewables hit 33.8% of global electricity in 2025. Coal sat at 33.0%. First time clean power has outsized coal since 1919. Solar alone covered 75% of new demand. Fossil generation fell for only the fifth time this century. Will DC push this further or will nuclear enter the pic at scale?

More at https://t.co/uIhcy0w735

Solar in 2025 grew 19x faster than experts at the International Energy Agency predicted in 2015.

Solar is now the fastest growing electricity source in human history.

China's chip exports hit $30B in April. Double YoY. Value growth was 4x volume in March, so most of that is memory shortage and AI server pricing, not new fab output.

More at https://t.co/VcO7wTNm1b

China's chip exports are surging:

China's chip exports jumped +100% YoY in April, to a record ~$31 billion.

This figure has TRIPLED over the last 2 years.

At the same time, overseas sales of laptops, tablets, and their components jumped +47% YoY.

Goldman Sachs and Nomura estimate that semiconductors, computers, and other AI-related products accounted for ~50% of China's export growth last month.

In total, Chinese exports rose +14% YoY in April, to $359 billion, the highest monthly reading on record.

Put differently, Chinese companies were generating ~$500 million in export revenue every hour on average last month.

China's economy is evolving with AI.

Americans don't think about AI much. It ranks 29th of 39 issues they care about. When they do think about it, they don't like it. Higher power bills, friends getting laid off, slop all over their feeds. That's how indifference turns into a real backlash, right as the capex cycle is hitting full speed.

More at https://t.co/iBMWNCwDOg

Everyone blames mag 7 for the "narrow market." Not really, the number of large caps have been 500 for decades. The missing companies are micro caps, from 4500 down to < 2k. Small-cap IPOs are shrinking and private capital ate the rest.

https://t.co/fto4bJPKsS

The "sell in May" pitch leaves out the part where May–Oct still returns 3.4% on average and is positive 72.4% of the time. same win rate as Nov–Apr. You're sitting out a coin flip that lands heads 7 out of 10 times.

"Sell in May and Go Away"

Has this been a good rule of thumb for investors to follow?

Not at all.

May-October returns are still positive on average (+7% annualized) with stocks higher 72% of the time.

Mortgage delinquencies sitting at 1% but credit card delinquencies at 13%. Same economy. If you locked a 3% mortgage in 2021 nothing is wrong. If you rent and carry a balance you're basically in 2009!

The blue line is getting the attention on this chart but the key takeaway is that all of credit cards, auto loans, and student loan delinquencies are at or near their highest levels ever. Only home loans are doing ok, but their market is on multi year life support demand wise.

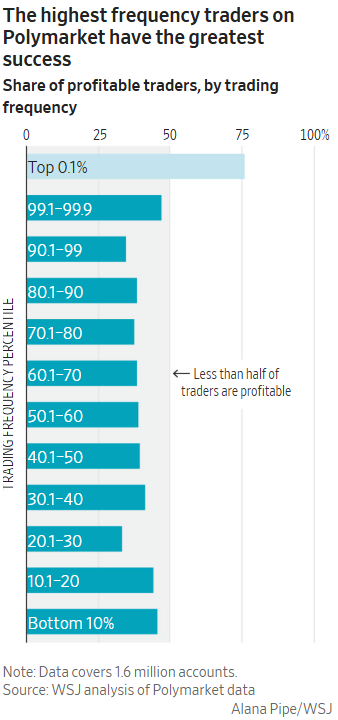

Polymarket has 1.6 million users. About 2000 of them walked off with 67% of the profits. Everyone else? 70% lost. Bottom 10% dropped 4k each.

The winners aren't sharp retail. It's Susquehanna, Jump, etc. Same shops running algos against retail flow on Wall Street, except now they're pointing them at people guessing whether some senator resigns. Calling this the next poker is generous. In poker the fish at least know they're the fish ;)

More at: https://t.co/E4Gm5LLmDs

Insane stat: of the 0.1% of accounts on Polymarket that trade the most, more than three-quarters are profitable. Everyone else? Loses money on average.

Every earnings call this quarter, AI comes up in literally every answer. Then Gallup goes and asks Americans what they're actually worried about, and AI lands 29th out of 39. Behind cost of living, inflation, even gas prices.

The people freaked out about AI? Mostly young, college-educated, well-off. Everyone else has bigger things to worry about.

So the thing slowing the AI buildout isn't going to be voters. It's power, money, and engineers.

More at: https://t.co/W34uxs1mfg

We might be heading towards a populist backlash towards AI, but we're not there yet. Outside the tech bubble, Americans really don't care about AI yet.

AI is Americans' 29th most important issue, according to the fantastic survey @davidshor ran that everyone is rightly looking at.

It's not surprising that Americans will answer sentiment questions about AI negatively, as they've been negative towards tech for a while. But it's a big leap from negative sentiment to meaningful political action.

Americans have been negative on social media for 10 years, and there has been no meaningful political action. And that's despite all the other hallmarks of backlash people are saying about AI---violent extremists (people forget there was a shooting at YouTube HQ), protests, etc.

My prediction: we will get real populist backlash to AI when the unemployment moves by, say, 2 percentage points and people see it as caused by AI.

That might happen quite soon. So it's good that people are already thinking about this issue and where it might lead (esp @jasminewsun whose recent writing on this has been incredible).

When the populist backlash does occur, people will be searching around for policies, and if we're lucky and smart, we'll have a library of potential good ideas ready to deploy. Because otherwise, we'll get horrible ideas like data center moratoria instead.

I'll be writing more about this for my piece on the poltical economy of AGI next week!

This capex cycle is so top-heavy it's barely a cycle. Used to be everyone joined in. Small caps, mid caps, large, mega, all spending together. Not this time. Mega caps are up 20%+ on capex YoY. Mid caps did nothing. Small caps are cutting. Five companies will commit $600b to AI this year alone. $2.1T over the next three. Borrowing got too expensive for everyone else to play.

https://t.co/RqsLmIra2j

More at: https://t.co/XV6YRjINQ3

Nobody could afford a lawyer or a real consultant before. That's the part of the AI conversation I keep not hearing. If the cost falls 75%, the market doesn't shrink. Instead it will finally open up to everyone who got priced out.

Source: https://t.co/CMLut6JLBv

More at: https://t.co/eDjcTZeEux

Funny how the "retail is dead" takes peaked in March, right before retail dumped $40B into stocks in April. They didn't capitulate. They just waited for the 16% bounce and piled back in.

More at: https://t.co/dDMPSTVi9r

Risk appetite among individual investors is skyrocketing:

Daily net call option purchases by retail investors are up to ~9 million contracts, the highest since November 2025.

This tracks the difference between call options purchased and call options sold, showing how aggressively retail is betting on stocks moving higher.

Net daily call option purchases have risen +7 million contracts, or +350%, since the late-March low.

This marks the largest monthly increase in net daily call option purchases in at least 2 years.

By comparison, the average between January 2024 and September 2025 was ~6 million contracts, or -33% below current levels.

Retail investors are now extremely bullish.

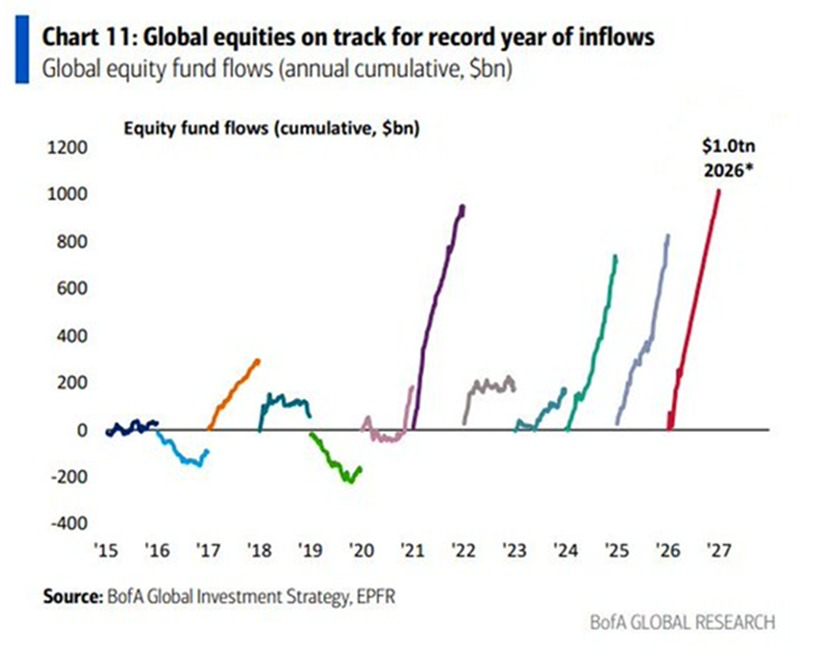

Record equity inflows in 2026 but have no idea where rates settle, where inflation actually goes, or how any of these wars end. And neither does anyone else, even if many sound certain.

Strong flows are great — until the day they stop being a tailwind and become the thing that snaps.

More at https://t.co/W6PJjeCDxh

BREAKING: Global equity funds are on track to attract +$1 trillion in annual inflows in 2026 for the first time in history.

This will surpass the previous record of +$970 billion set in 2021.

This comes as investors have already poured +$310 billion into world equity funds year-to-date.

By comparison, global equity funds attracted +$850 billion in the full year 2025.

Meanwhile, global corporate investment-grade bond funds are on pace to attract a record +$434 billion this year.

Asset owners will be the only winners in this market.

When CPI is above 3%, no one wins.

S&P gives up ~380bps. Credit gives up 300+.

Inflation expectations: 4.8%.

Every bull narrative right now: hedge funds adding tech, consumers still spending, is really one trade: a CPI print that finally cools.

https://t.co/qTFBDtsA3p

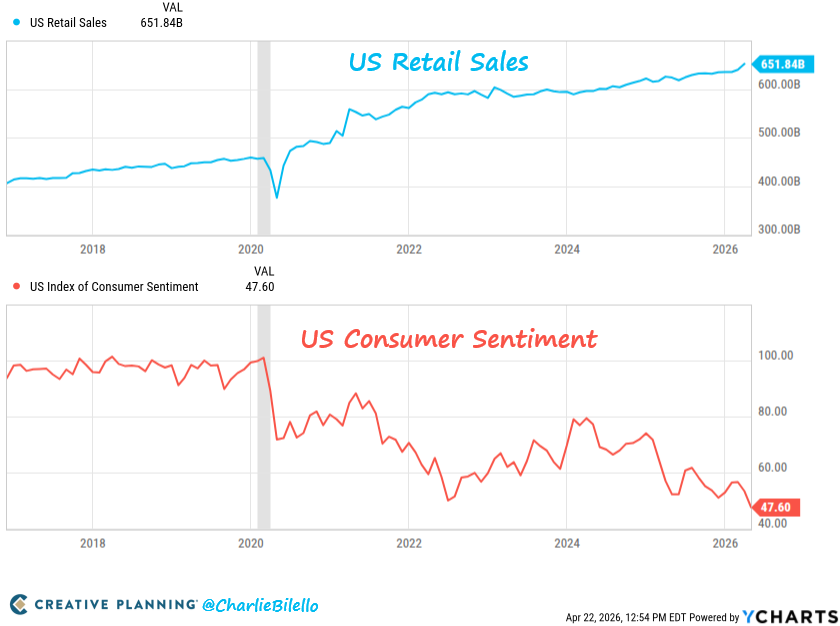

Worst consumer sentiment in 74 years but highest retail sales ever.

Asset-rich households keep spending. Everyone else is telling pollsters how bad it feels...

More at https://t.co/mS0jYe0H60

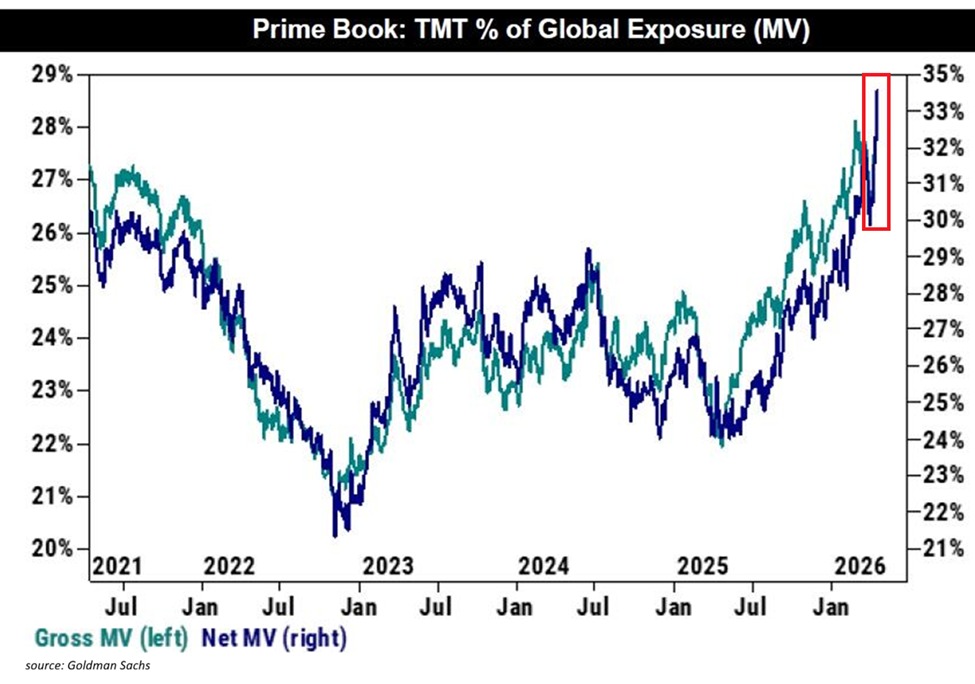

V-shape of the year isn't in the tape. It's in HF TMT books.

Worst drawdown since 22 to 5yr-high net exposure in weeks.

The velocity of the flow is quite impressive!

More at https://t.co/LHXwzkHJEB

Hedge funds are aggressively buying tech stocks:

Hedge funds purchased global technology stocks more than any other sector last week.

Information Technology names were purchased for the first time in 5 weeks, led by semiconductors, electronic equipment, and software.

At the same time, purchases of Communication Services were the largest in 5 months.

This was primarily driven by new long positions rather than short covering, signaling genuine institutional demand rather than forced repositioning.

As a result, hedge fund gross and net exposure to global tech rose to 28.3% and 34.0%, both the highest in 5 years.

Hedge funds are piling back into tech.

930 bn in 6 years. 0.5% of GDP a year. Entirely privately funded. The biggest private capex programme in US history since the 1800s railroads. This time nobody's asking taxpayers to underwrite the future.

More at https://t.co/Q87sgt4sG4

47.6. UMich consumer sentiment just printed its lowest reading ever, worse than 08, worse than 1980.

Honestly the number isn't what got me. It was reading the UMich director herself say "every age, income, and political party posted setbacks, as did every component of the index."

You rarely see everyone agree on anything these days. Let alone agree on pessimism. Caveat is that most of the survey ran before the Iran ceasefire.

Source: https://t.co/Wm9iE4minq

Read more: https://t.co/GNZsnN6elD

Funny thing about "tech is expensive" is that the Nasdaq's forward P/E is at 22.4x, below the 10yr avg. The narrative hasn't caught up to the tape. Every time that gap existed in the last five years it closed the same way.

https://t.co/uX6tvsfdzl

More at https://t.co/3FJQxFa8WE