In those days of semi conductors massive jumps in stock prices 📈, I feel a bit odd adding and growing my Krones AG $KRN.DE position 🇩🇪

But honestly connecting less over X and other platforms helps really stay focused and not start questioning everything.

Whether you made or not great gains there, just be cautious either way, knowing when to jump in or out 🙏👍🤞

Sometimes standard stock screeners hide the best investing opportunities $KRN.DE 🚨📊

If you look at most finance databases, Krones AG 🇩🇪 shows a weak 7-8% ROIC. Many quality investors might see that number and skip the stock. But the data is entirely wrong and here is why:

🔹 The cash drag: Krones holds €548M in net cash. Leaving this idle cash in the calculation artificially lowers their reported returns.

🔹 Customer advances: Customers pay upfront before their bottling lines are built. This structurally lowers the amount of capital Krones has to risk.

The Real Number: When you remove the excess cash, Krones' True ROIC is actually 17.5% to 19% with

🔸NOPAT-based economics

and

🔸excess cash removed

🚀

Krones is not a low-return, cyclical machinery company. It is a very good packaging automation compounder selling at a traditional manufacturing price (5x EV/EBITDA).

$krn $krn.de

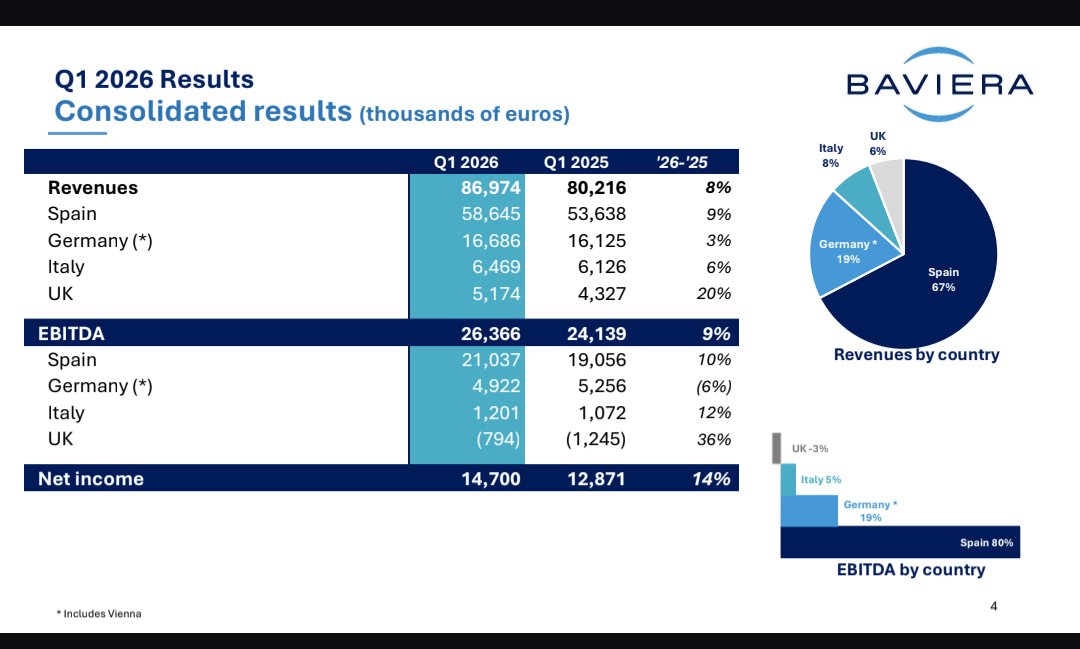

Clínica Baviera $CBAV Q1 2026 are out and they are crazy good🏥📊

🔸Top Line: revenues grew 8% to €86.97M.

🔸Bottom Line: net income jumped 14% to €14.7M.

🔸Sitting on a massive net cash position of €57.4M, up from €42.4M at year-end.

🔸UK 🇬🇧 turnaround: revenues surged 20%. The EBITDA loss is narrowing fast as the business scales.

🔸Spain 🇪🇸: added 4 new clinics. They are clearly reinvesting their high returns into new local hubs to grab market share.

🔸Italy 🇮🇹 : improving profitability, with margins hitting nearly 19%.

🔸Germany 🇩🇪 : market is facing some economic headwinds, but the business is holding up with 3% growth.

So many good questions.

1/ The exceptional tax — France introduced it as a "temporary" fiscal measure for 2024-2025. Officially two years. But "temporary" French taxes have a habit of becoming permanent, or getting replaced by a structurally similar levy. The risk isn't this specific tax; it's that Vinci's concession profits are a perennial target whenever Paris needs revenue.

2/ Airport M&A — Vinci Airports is one of the best capital allocators in infrastructure I would say. The model is attractive: buy undervalued regulated assets, apply operating leverage, harvest long-duration cash flows. They still have dry powder and the concession pipeline globally hasn't dried up (LatAm, Southeast Asia, Southern Europe). Balance sheet is solid enough to keep deploying. My view here is that the real constraint is deal availability at sensible or reasonable prices, not their capacity to execute.

3/ Construction vs Energy — this is the most critical question. It is true that Vinci Construction is the drag: cyclical, low margin, labor-intensive. On the other hand, Vinci Energies built mostly thanks to the Cobra deal (electrical, digital, HVAC) is the gem — high recurring revenue, fragmented acquisitions compounding quietly, direct tailwind from electrification and data center buildout. My intuition is that they've resisted divesting construction partly because it feeds the concessions pipeline (in-house contractor advantage). But at some point the sum-of-parts argument for a Vinci Energies spin-off becomes hard to ignore or in other words very compelling.

Any thoughts from your side ?!

Vinci $DG.PA just released its 2025 results, and it is a masterclass in why "Infrastructure Monopolies" are the ultimate generational assets.

Even with a massive new tax in France, the company is printing more cash than ever. Here is the high-value breakdown for your portfolio:

1️⃣ The "Cash Flow" King 👑

Vinci generated a record FCF of €7.0 Billion in 2025.

I really love this as it allows Vinci to buy more assets without taking on dangerous debt.

2️⃣ The "Hidden" Growth 📈

Net profit was €4.9 Billion. It looks flat, but it is a "fake" slowdown.

France added an exceptional tax that cost Vinci €449 million.

Without this tax, profit grew by 10%. * The underlying business is actually accelerating

3️⃣ The Global Monopoly 🌍

Vinci is no longer just a "French builder."

59% of revenue now comes from outside France.

Airports: Traffic is booming (+5%), and they are locking in long-term deals in London Gatwick and Mexico.

Energy (Cobra IS): This is their secret weapon for the energy transition, with a massive €35B order book.

4️⃣ Shareholder Reward 💰

They proposed a dividend of €5.00 per share (up from €4.75). This is a consistent, growing "rent" check for anyone holding the stock.

Eiffage $FGR.PA, Ferrovial $FER, ACS $ACS , Hochtief $HOT

The new "Luce" electric model is getting a lot of bad feedback. Design matters for Ferrari $RACE because their whole business is based on desirability.

If the car is "ugly" or lacks the Ferrari soul, the pricing power might disappear...I am highly skeptical 🤨

@FinanceClean Je suis d'accord mais du coup pour le futur votre valorisation intègre un possible ajustement de la valeur terminale lié au risque AI ou pas du tout.

Je n'arrive pas à aller sur du software trop peur et incapable de prédire comment évoluera le marché 😄☺️

@Nicoloz__ C'est le spin-off de l'ancien Cargotec, concurrent de Konecranes sur le matériel roulant dans les ports. Belle pépite avec une grande partie de ses revenues venant des services

Mais j'en prends note 🙏

Sometimes standard stock screeners hide the best investing opportunities $KRN.DE 🚨📊

If you look at most finance databases, Krones AG 🇩🇪 shows a weak 7-8% ROIC. Many quality investors might see that number and skip the stock. But the data is entirely wrong and here is why:

🔹 The cash drag: Krones holds €548M in net cash. Leaving this idle cash in the calculation artificially lowers their reported returns.

🔹 Customer advances: Customers pay upfront before their bottling lines are built. This structurally lowers the amount of capital Krones has to risk.

The Real Number: When you remove the excess cash, Krones' True ROIC is actually 17.5% to 19% with

🔸NOPAT-based economics

and

🔸excess cash removed

🚀

Krones is not a low-return, cyclical machinery company. It is a very good packaging automation compounder selling at a traditional manufacturing price (5x EV/EBITDA).

$krn $krn.de

I’ve added Krones AG $KRN.DE to my portfolio. 🇩🇪🍻📦

It is not an "exceptional" company (like a tech giant), but it is a "Very Good" company at a "Great Price." It sits at the perfect intersection of Quality and Value.

Here is why this is a high-reward play:

🛡️ The key facts

🔸Family Owned: The Kronseder family owns 51.85% of the company 🤝

🔸Cash King: They are sitting on a massive €523 Million net cash pile (as of Q1 2026). They have zero debt stress and plenty of fuel for acquisitions. 💰

🏗️ Why is it "Quality"?

Krones is a global leader in bottling lines (Coke, Pepsi, Heineken).

The Moat: Once a factory installs a Krones line, they are locked in for 20+ years of Service and Spare Parts. This "aftermarket" revenue is high-margin and very stable.

Q1 2026 Performance: Orders grew +5.3% to €1.5 Billion, and EBITDA margins improved to 10.8%. The business is getting more efficient. 💪

📊 The Value Math (Reverse DCF)

At 5x EV/EBITDA, the market is treating Krones like it's a failing business. My math shows otherwise:

Market View: The current price (~€117) implies the company will shrink by -5% every year for the next decade. 📉

Reality: Krones is growing at 3-5% organically.

Upside: Using relatively conservative numbers, a "Fair Value" is closer to €145+. That is an upside of approx 30% just to reach a normal valuation. 📈⚖️

✅The Bottom Line: You are buying a family-backed, cash-rich, global leader at a "recession" price while the business is actually growing $KRN. ☕📦

I’ve added Krones AG $KRN.DE to my portfolio. 🇩🇪🍻📦

It is not an "exceptional" company (like a tech giant), but it is a "Very Good" company at a "Great Price." It sits at the perfect intersection of Quality and Value.

Here is why this is a high-reward play:

🛡️ The key facts

🔸Family Owned: The Kronseder family owns 51.85% of the company 🤝

🔸Cash King: They are sitting on a massive €523 Million net cash pile (as of Q1 2026). They have zero debt stress and plenty of fuel for acquisitions. 💰

🏗️ Why is it "Quality"?

Krones is a global leader in bottling lines (Coke, Pepsi, Heineken).

The Moat: Once a factory installs a Krones line, they are locked in for 20+ years of Service and Spare Parts. This "aftermarket" revenue is high-margin and very stable.

Q1 2026 Performance: Orders grew +5.3% to €1.5 Billion, and EBITDA margins improved to 10.8%. The business is getting more efficient. 💪

📊 The Value Math (Reverse DCF)

At 5x EV/EBITDA, the market is treating Krones like it's a failing business. My math shows otherwise:

Market View: The current price (~€117) implies the company will shrink by -5% every year for the next decade. 📉

Reality: Krones is growing at 3-5% organically.

Upside: Using relatively conservative numbers, a "Fair Value" is closer to €145+. That is an upside of approx 30% just to reach a normal valuation. 📈⚖️

✅The Bottom Line: You are buying a family-backed, cash-rich, global leader at a "recession" price while the business is actually growing $KRN. ☕📦

🐦 Atlas Copco $ATCO 🛠️🇸🇪

Atlas Copco shares are down 5% today. The market is panicking over "reported" numbers, but what I read makes me like this earnings release

1️⃣ The Cash Flow 📉

Operating cash flow is down 34%. Why? It’s just "Working Capital" timing (inventories and receivables). Atlas Copco has a 90%+ cash conversion track record over decades. One quarter is noise and I expect this to normalize.

2️⃣ The currency issue🌍💸

Reported Orders: -3% 🔴

Organic Orders (Real): +5% ✅

The entire "decline" is just a strong Swedish Krona (SEK) making foreign sales look smaller. The business is actually growing.

3️⃣ The "AI Engine" is exploding thanks to vacuum segment🚀

The Vacuum Technique segment is the real star:

✅ Organic Orders: +32%

✅ Margins: Up to 20.5%

AI and semiconductor demand are flowing directly into Atlas Copco’s pockets.

Overall I think there is a lot to like about $ATCO.B including the final concrete delivery on AI promesse - the FCF, ROIC issues seem really temporary ☕📦

Air Liquide ✅

Le titre pourrait respirer un peu.

En tant que "long term" je retiens ces deux belles slides qui montrent à quel point le management est tourné vers l'avenir : une marge qui devrait progresser de 5.6% en 6 ans 😍🙏